Download to read offline

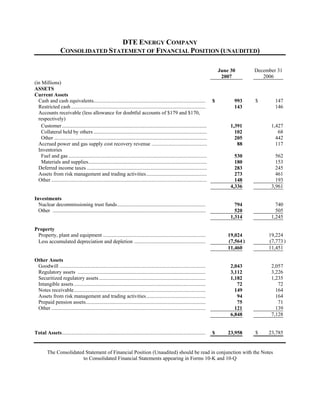

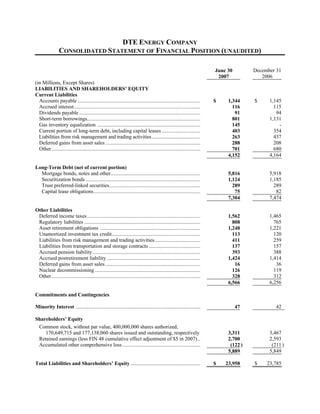

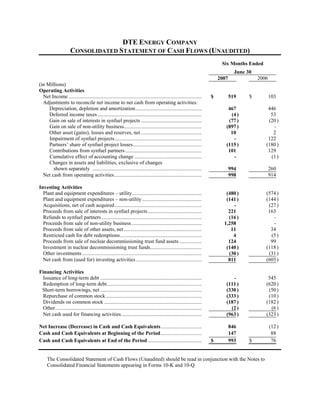

This document provides supplemental financial information for DTE Energy Company for the second quarter of 2007. It includes consolidated statements of financial position, cash flows, and operations for DTE Energy and its subsidiaries Detroit Edison and Michigan Consolidated Gas. Some key details are: - Total assets for DTE Energy as of June 30, 2007 were $23.958 billion, with current assets of $4.336 billion and property, plant and equipment of $11.451 billion. - Total debt for DTE Energy as of June 30, 2007 was $6.981 billion, or 53% of its total capitalization of $13.159 billion. - For the second quarter of 2007, Detroit E