Download to read offline

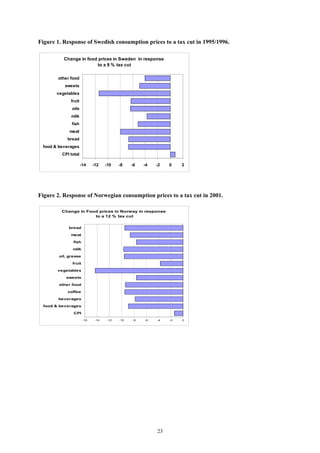

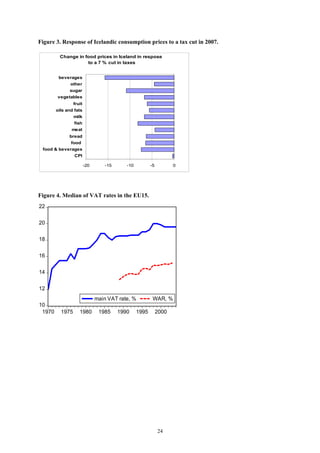

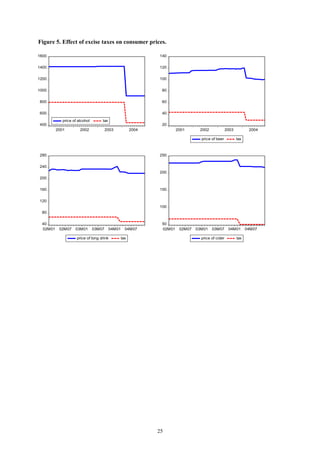

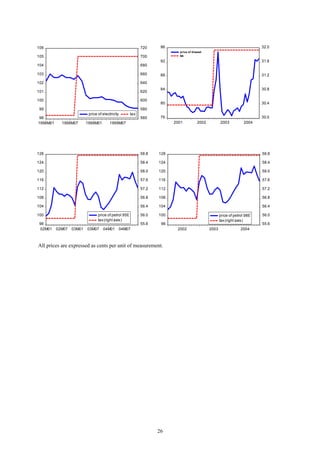

This study investigates how consumption taxes, particularly value-added tax (VAT), impact consumer prices in EU countries from 1970-2004. The findings indicate that approximately two-thirds of a tax increase is passed on to consumer prices, with minimal evidence of a similar effect on producer prices. The research is timely due to Finland's high food VAT rate and considerations for potential tax cuts.