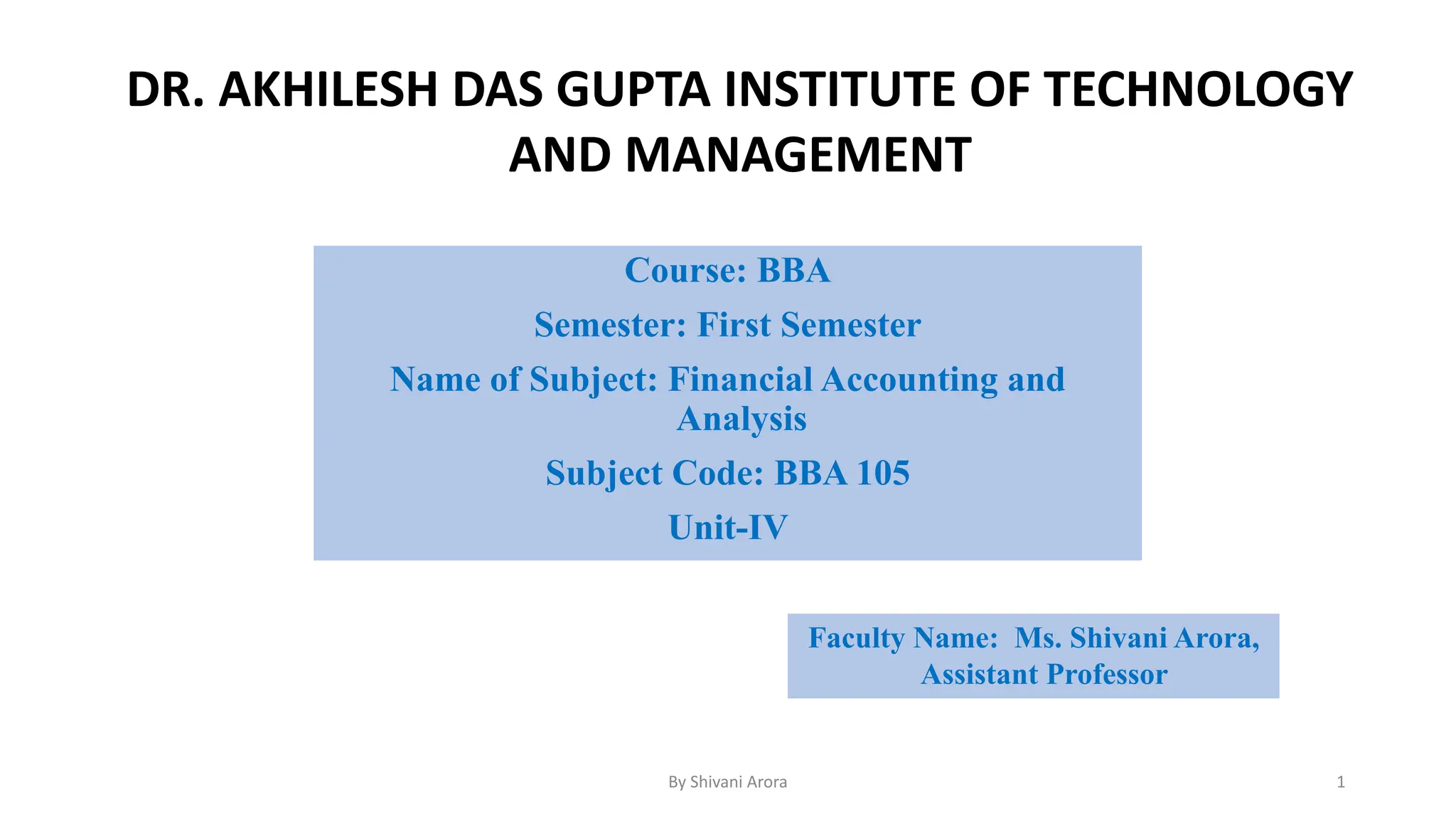

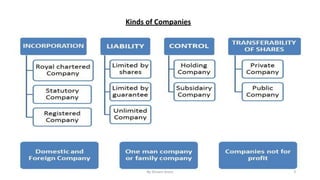

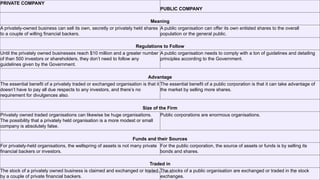

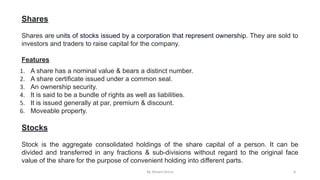

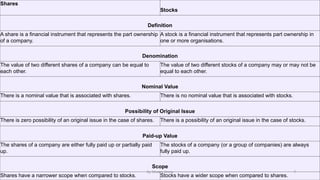

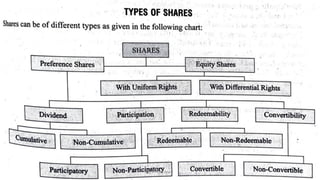

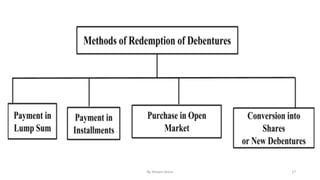

The document elaborates on the concept of joint stock companies, defining their characteristics and contrasting them with partnership firms. It discusses types of companies, including private and public companies, their share capital, shares, and debentures, along with related financial mechanisms like rights shares and bonus shares. Moreover, it outlines the regulations governing each type and the implications of shares' issuance, transfers, and forfeitures.

![DTB presentation[1].pptxrjfkkfkfkkfkfkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/dtbpresentation1-240424142240-fc4a479e-thumbnail.jpg?width=640&height=640&fit=bounds)