Download to read offline

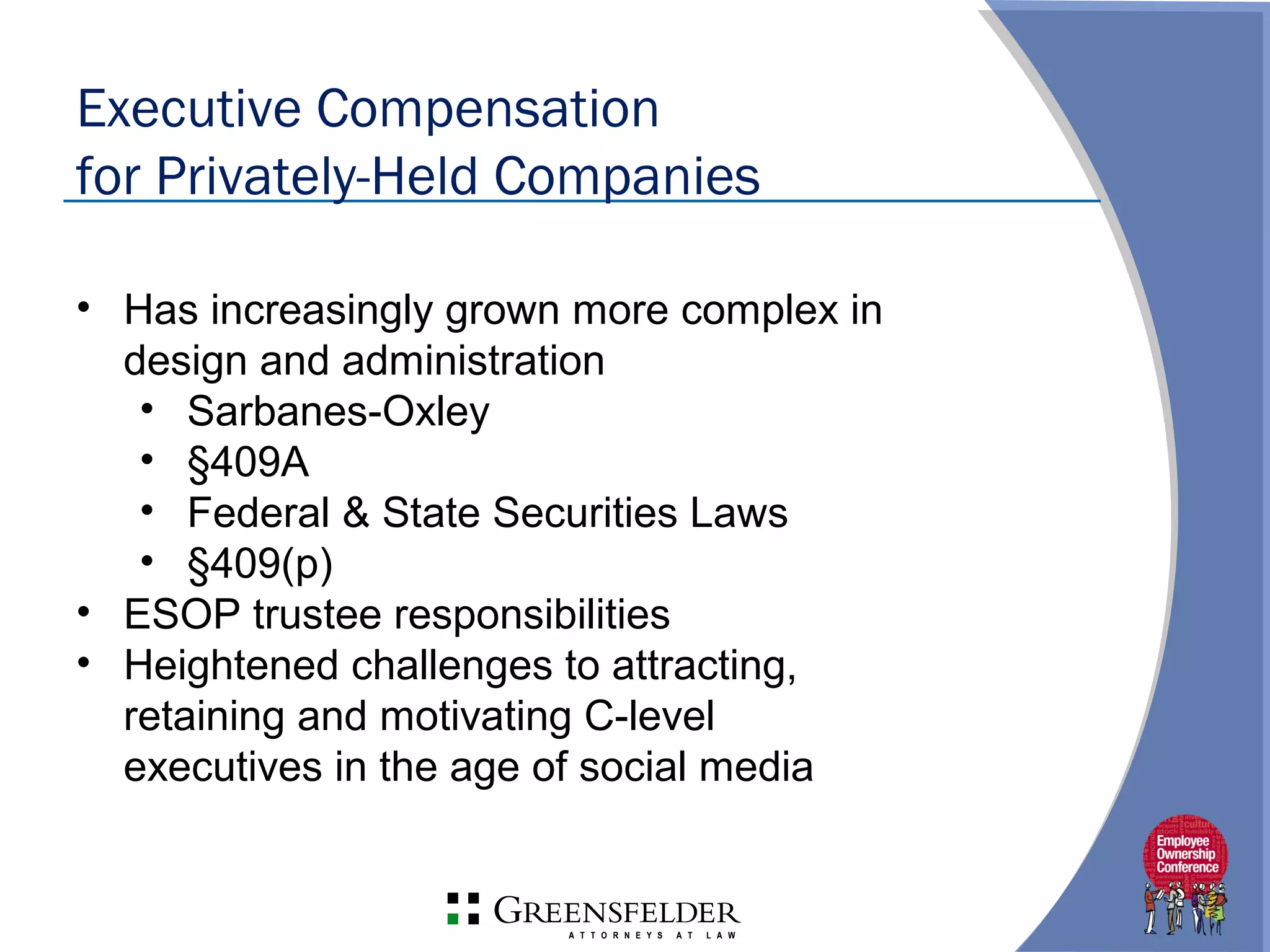

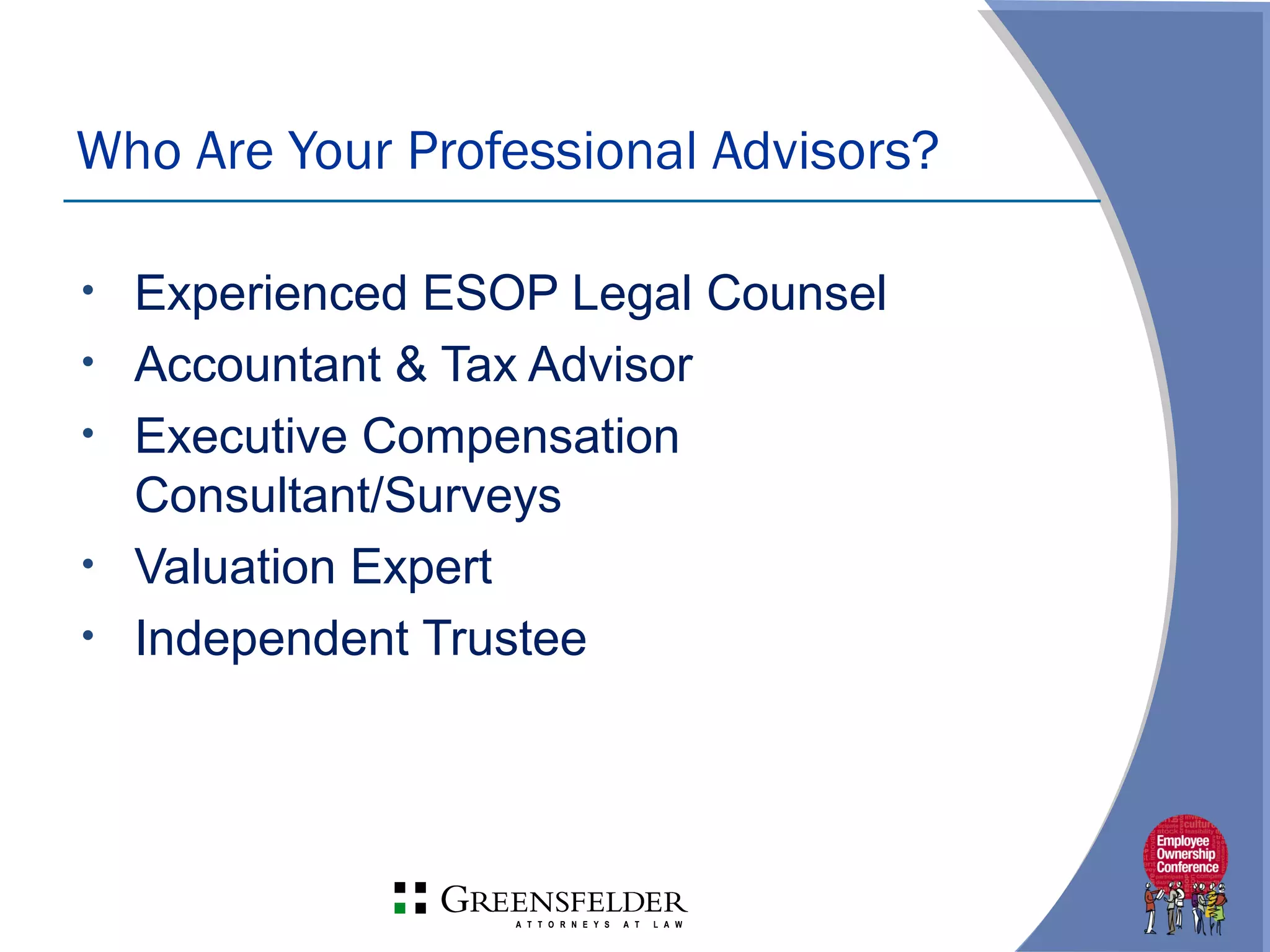

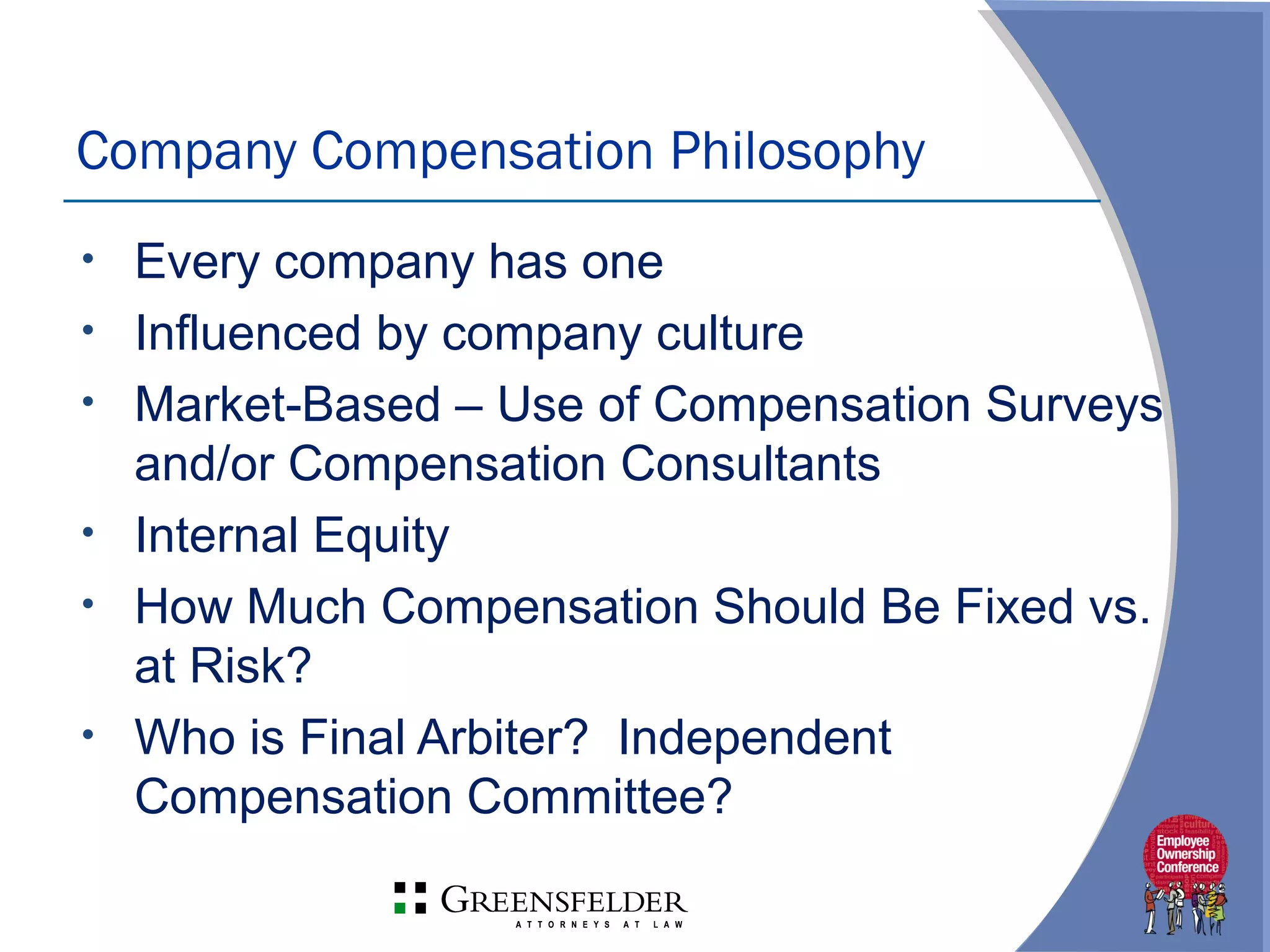

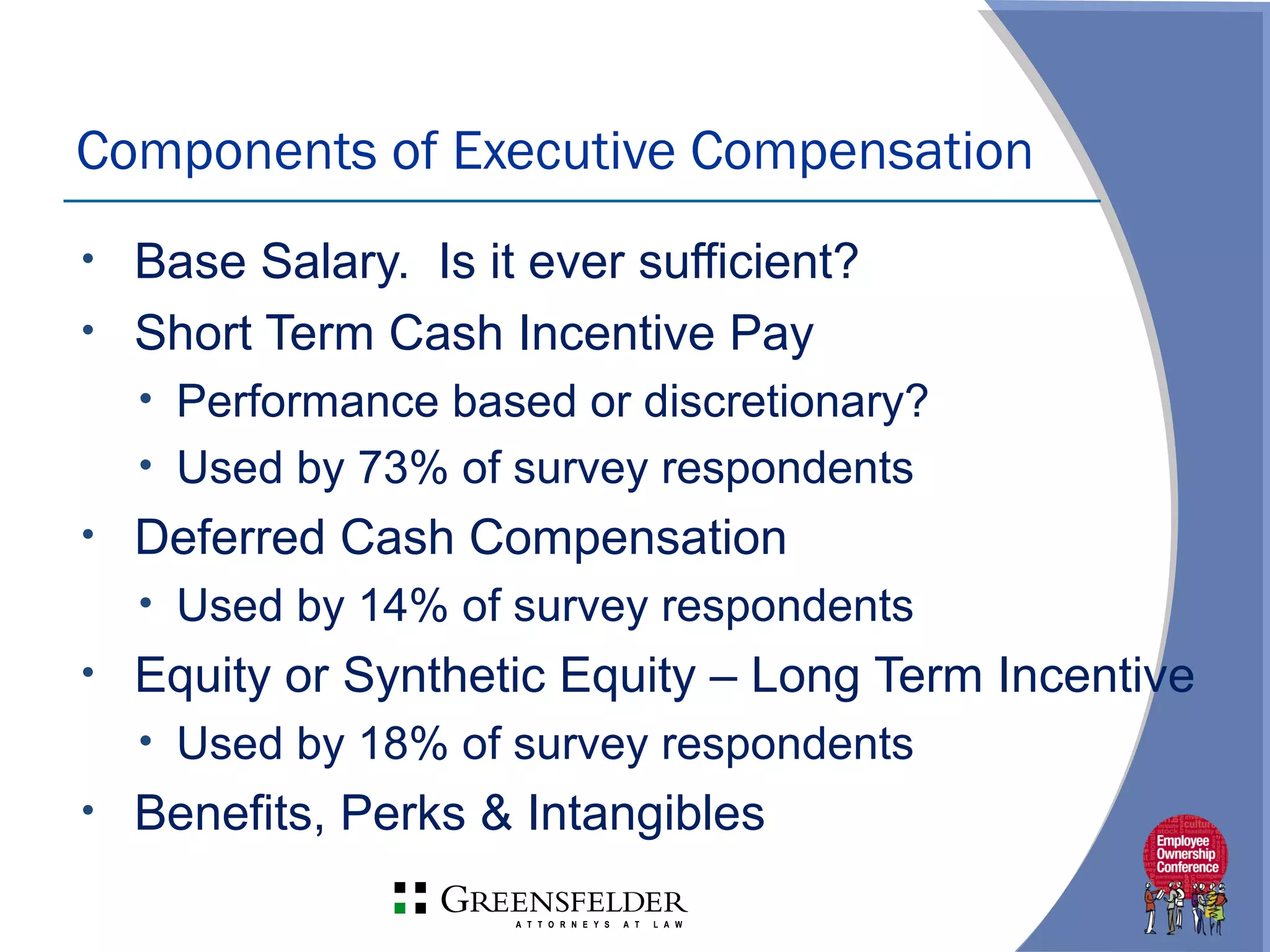

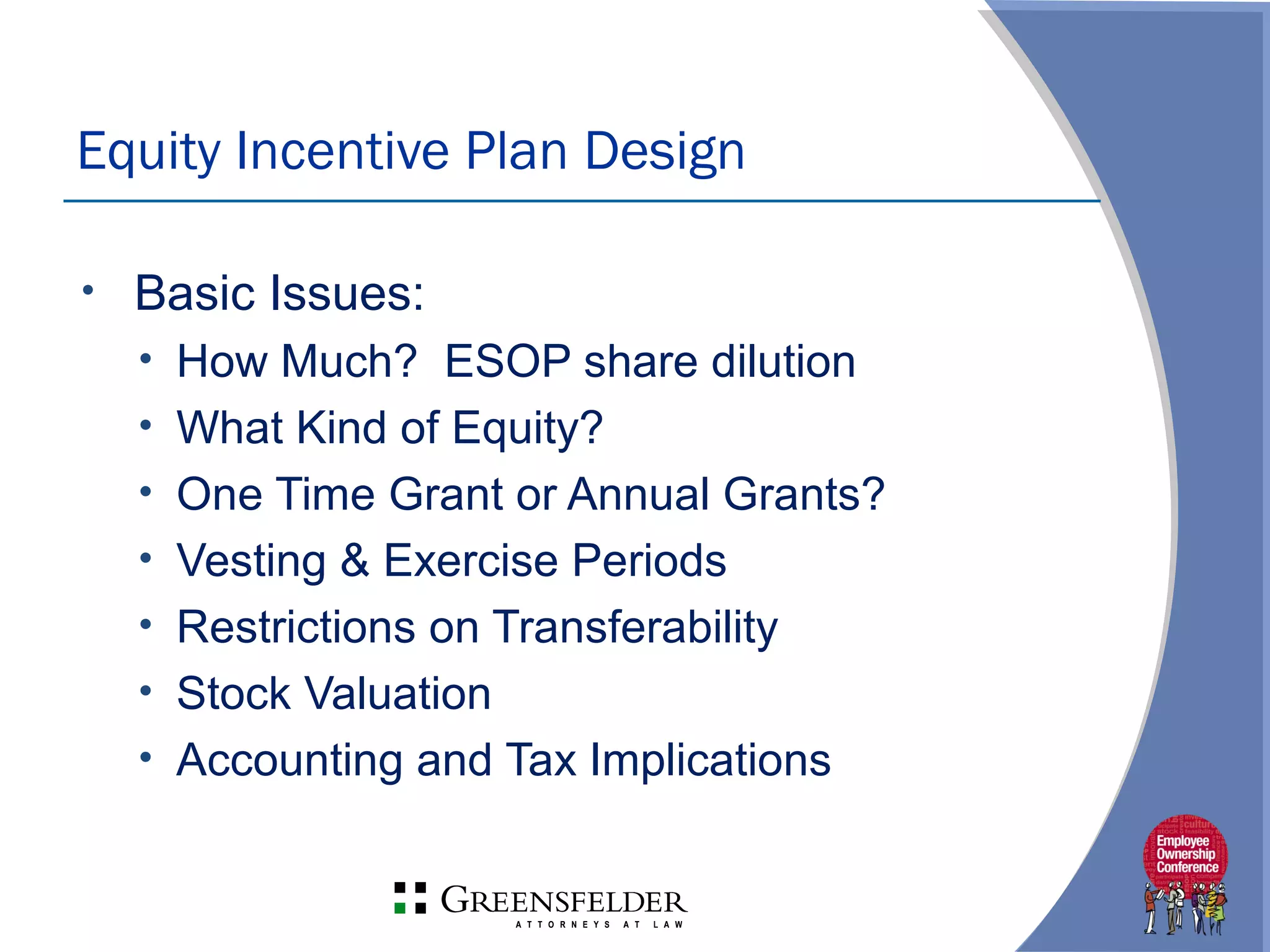

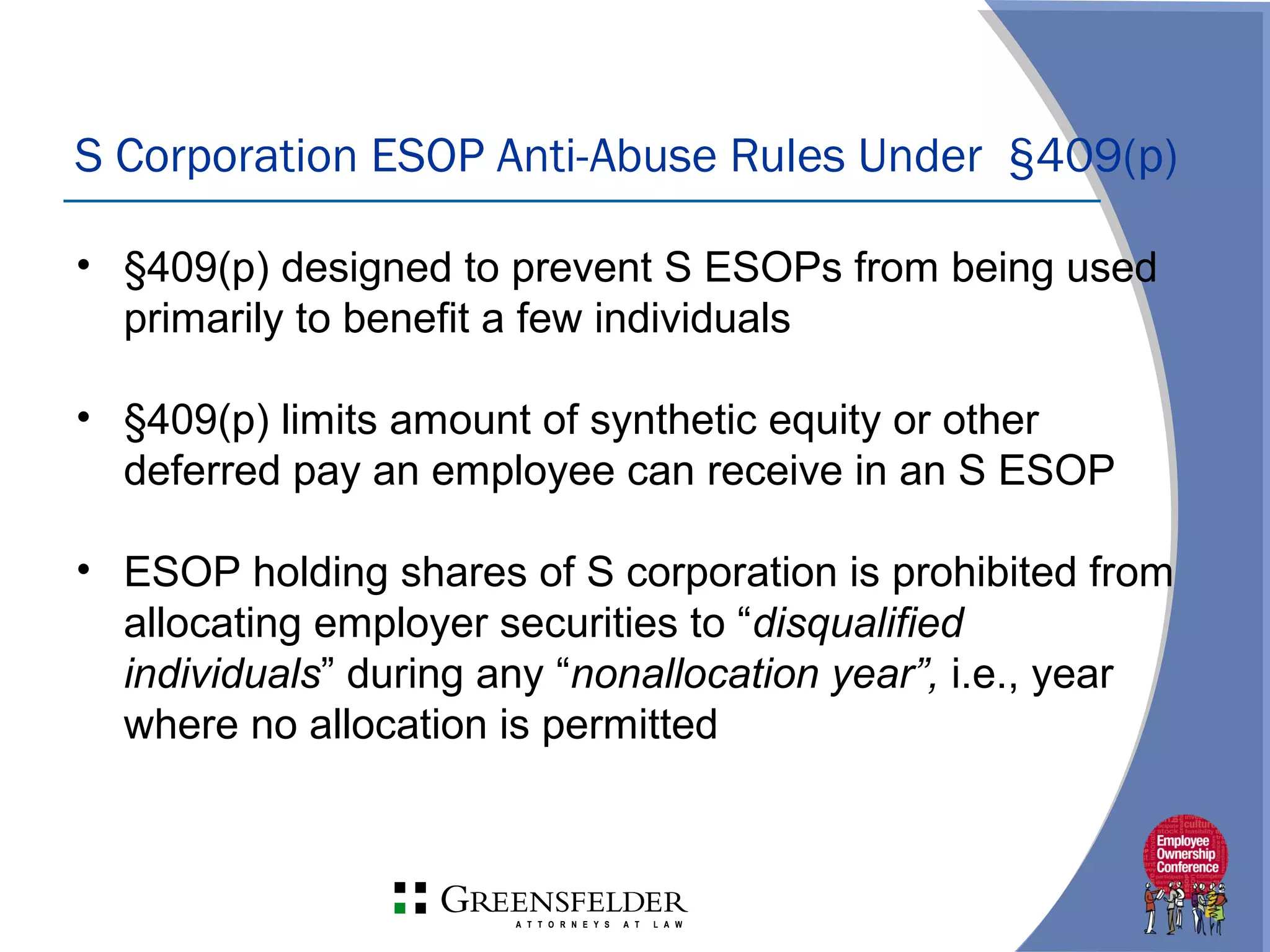

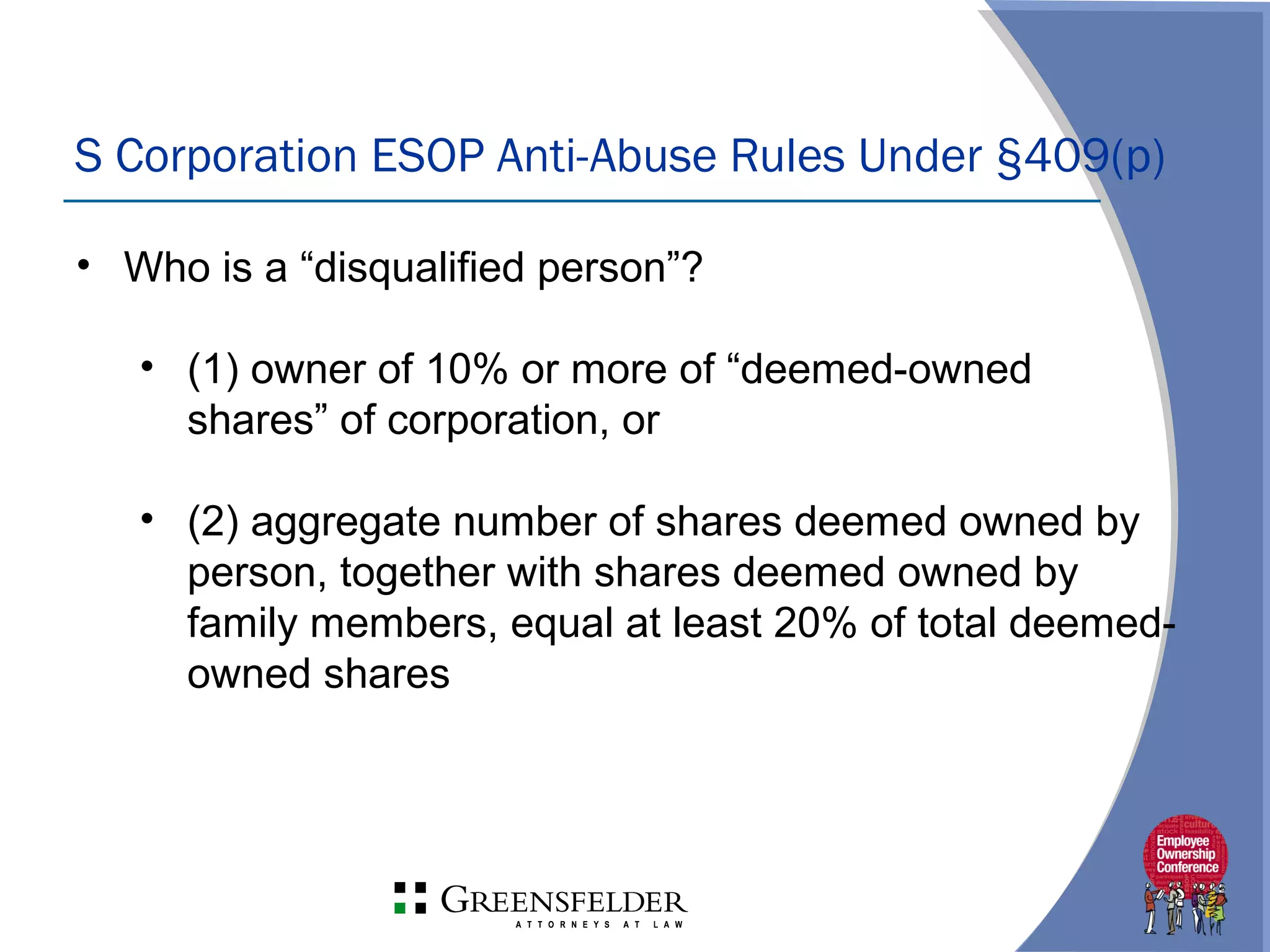

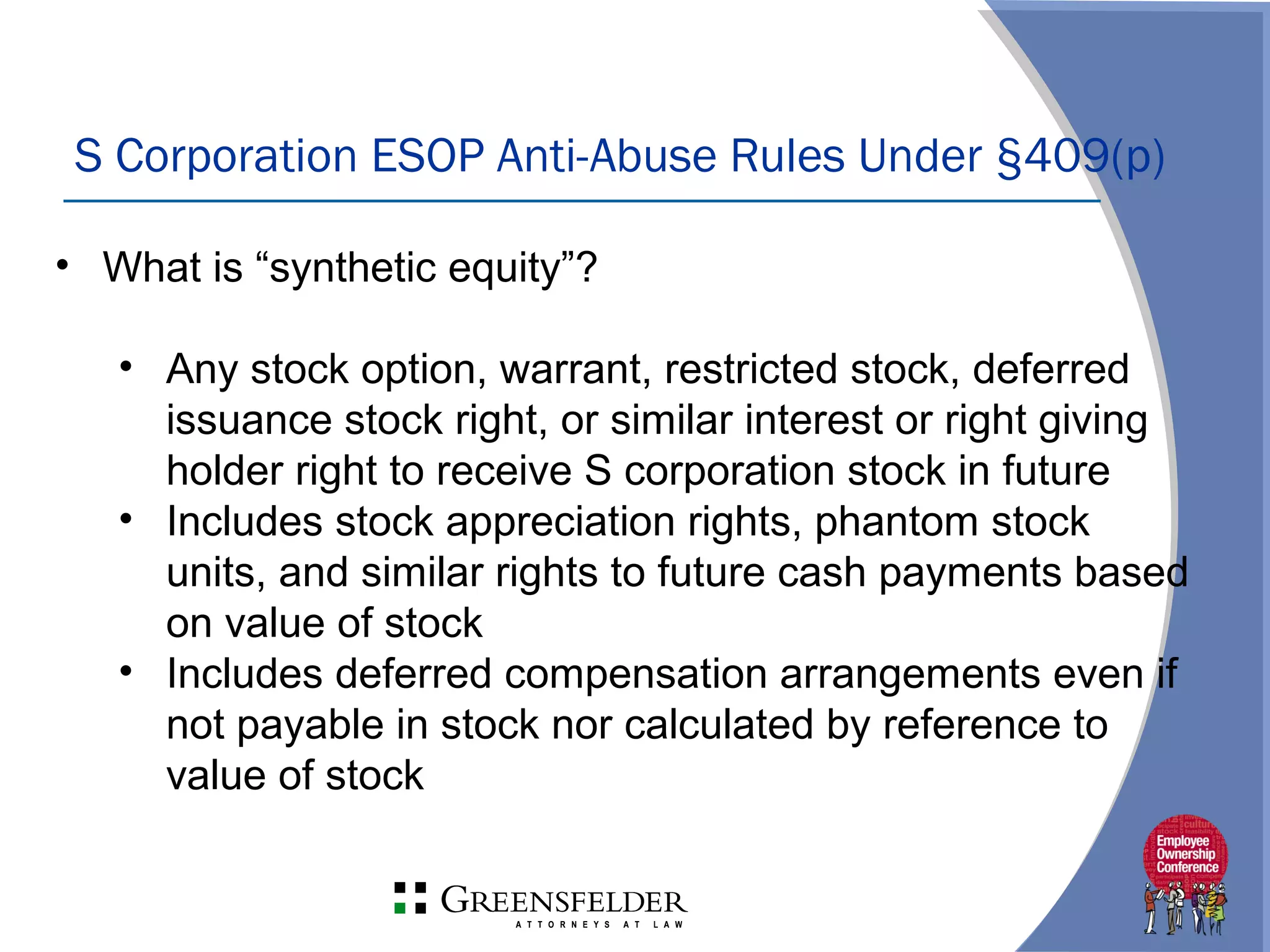

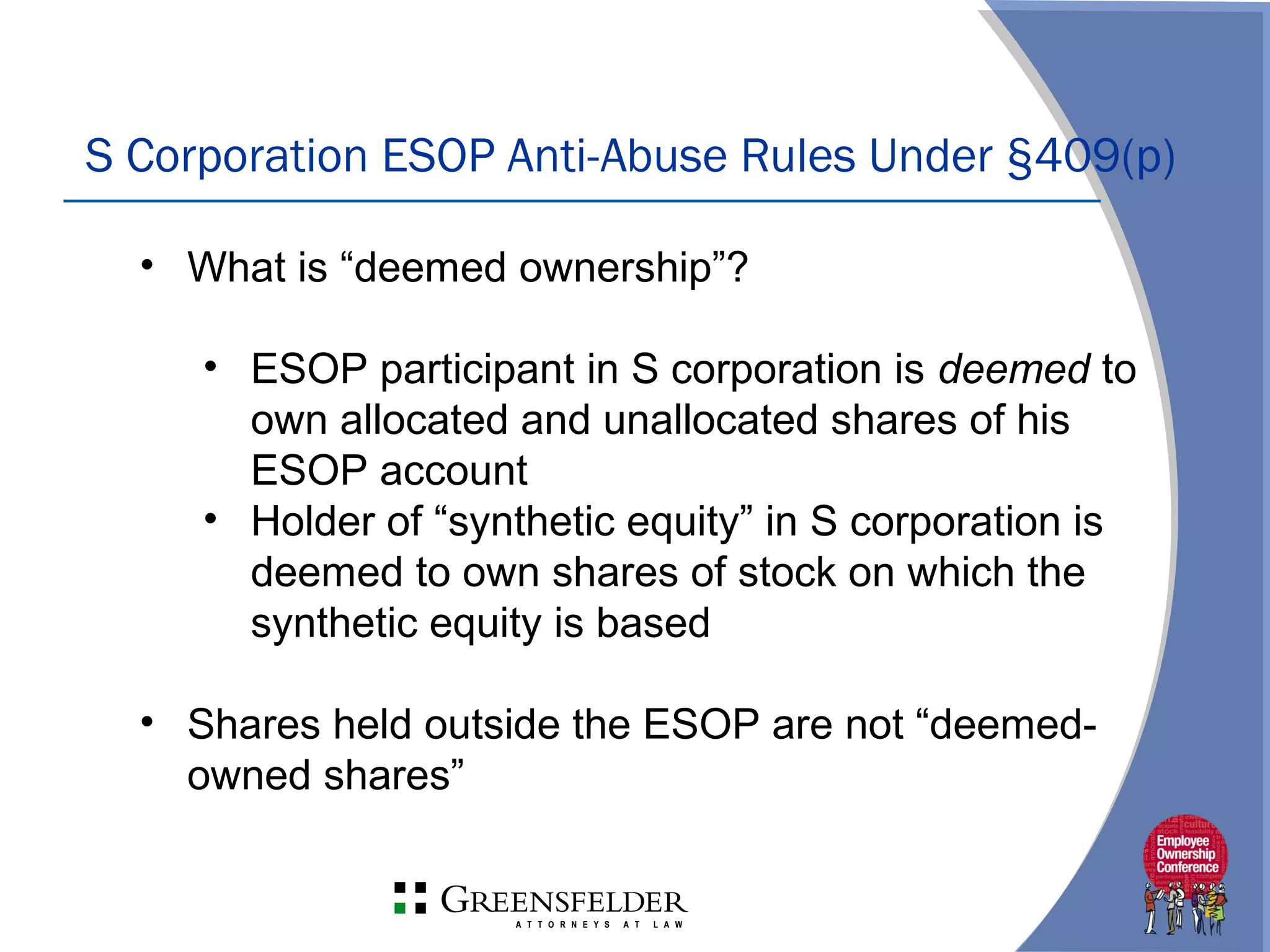

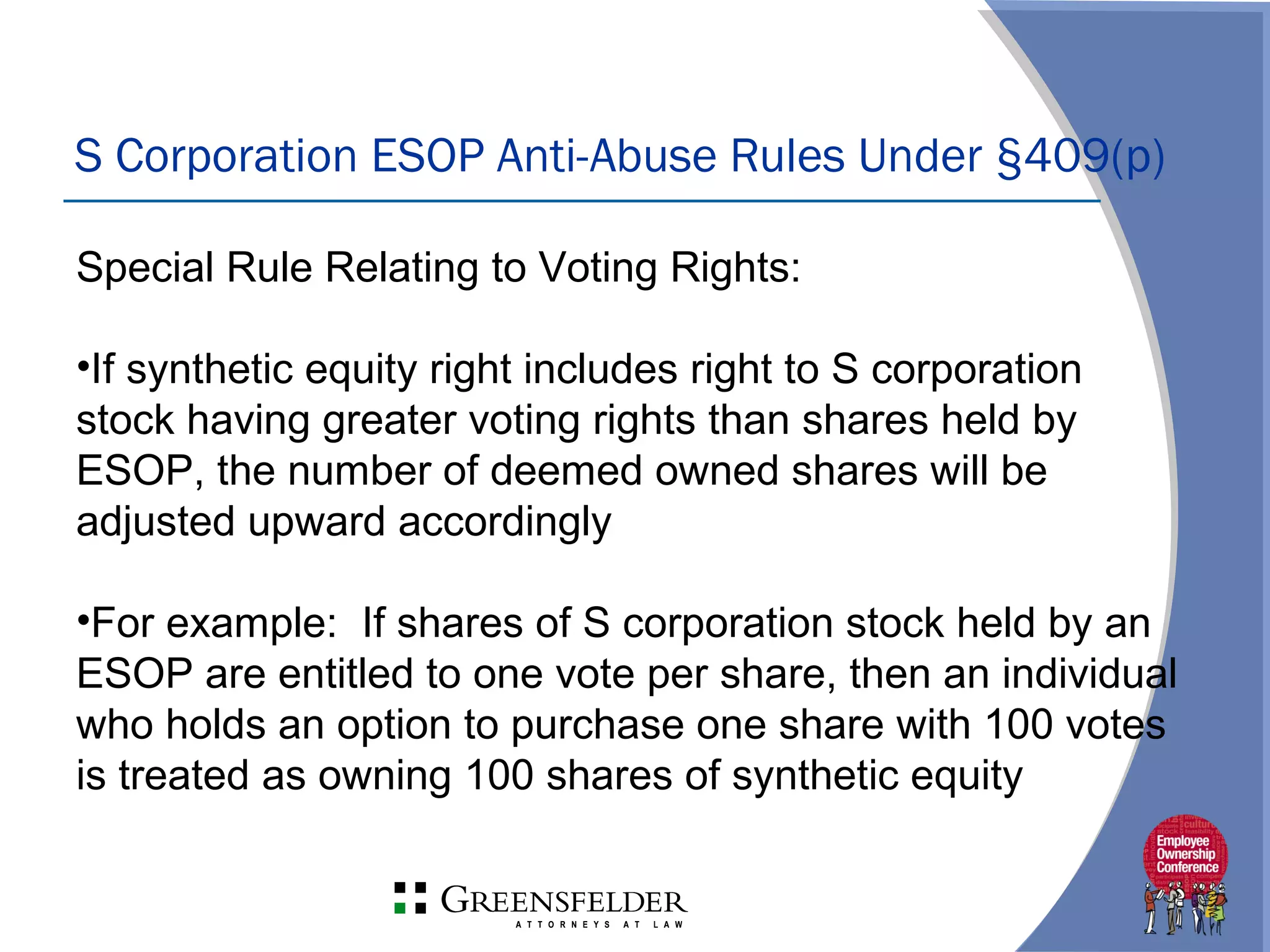

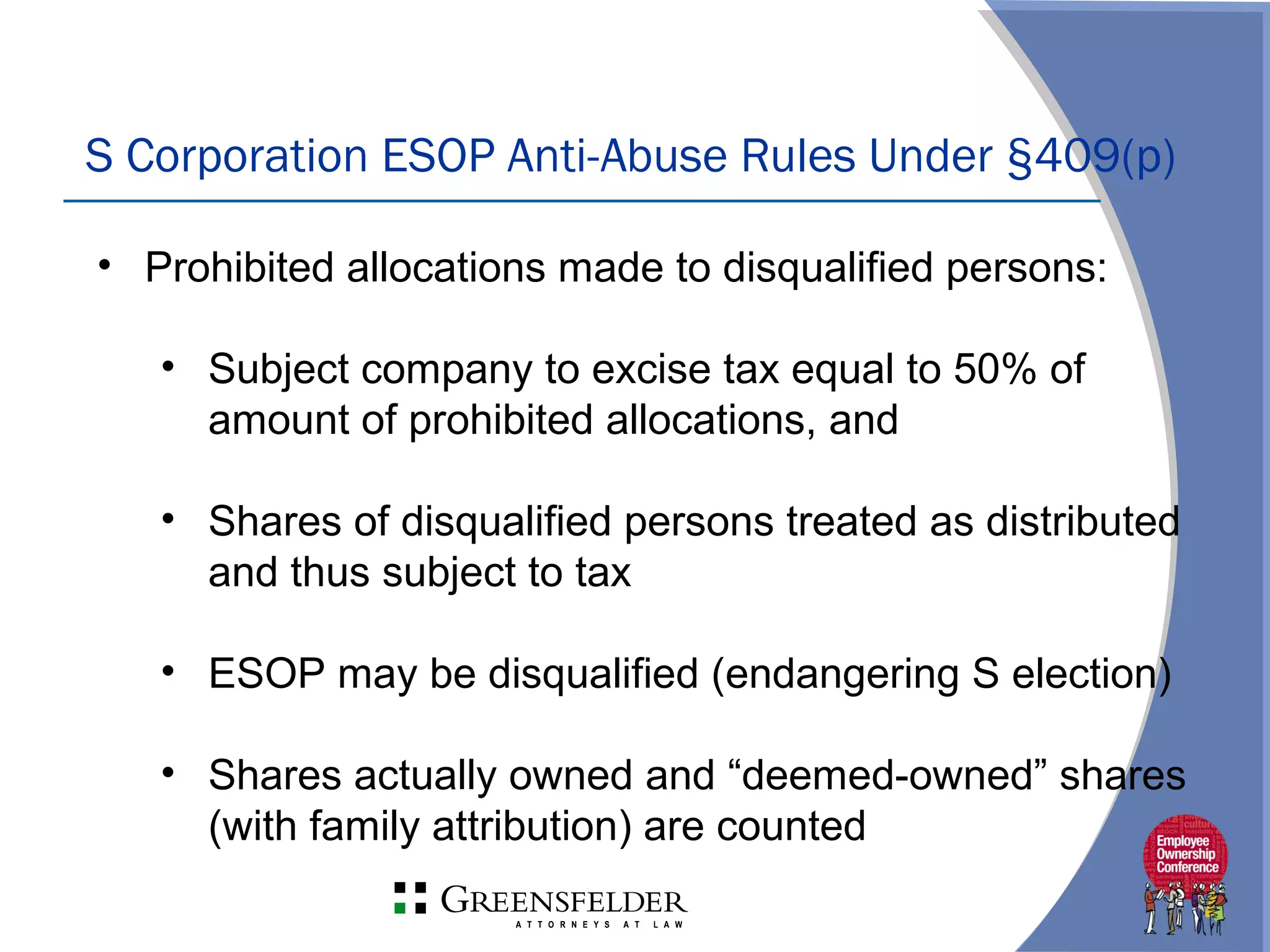

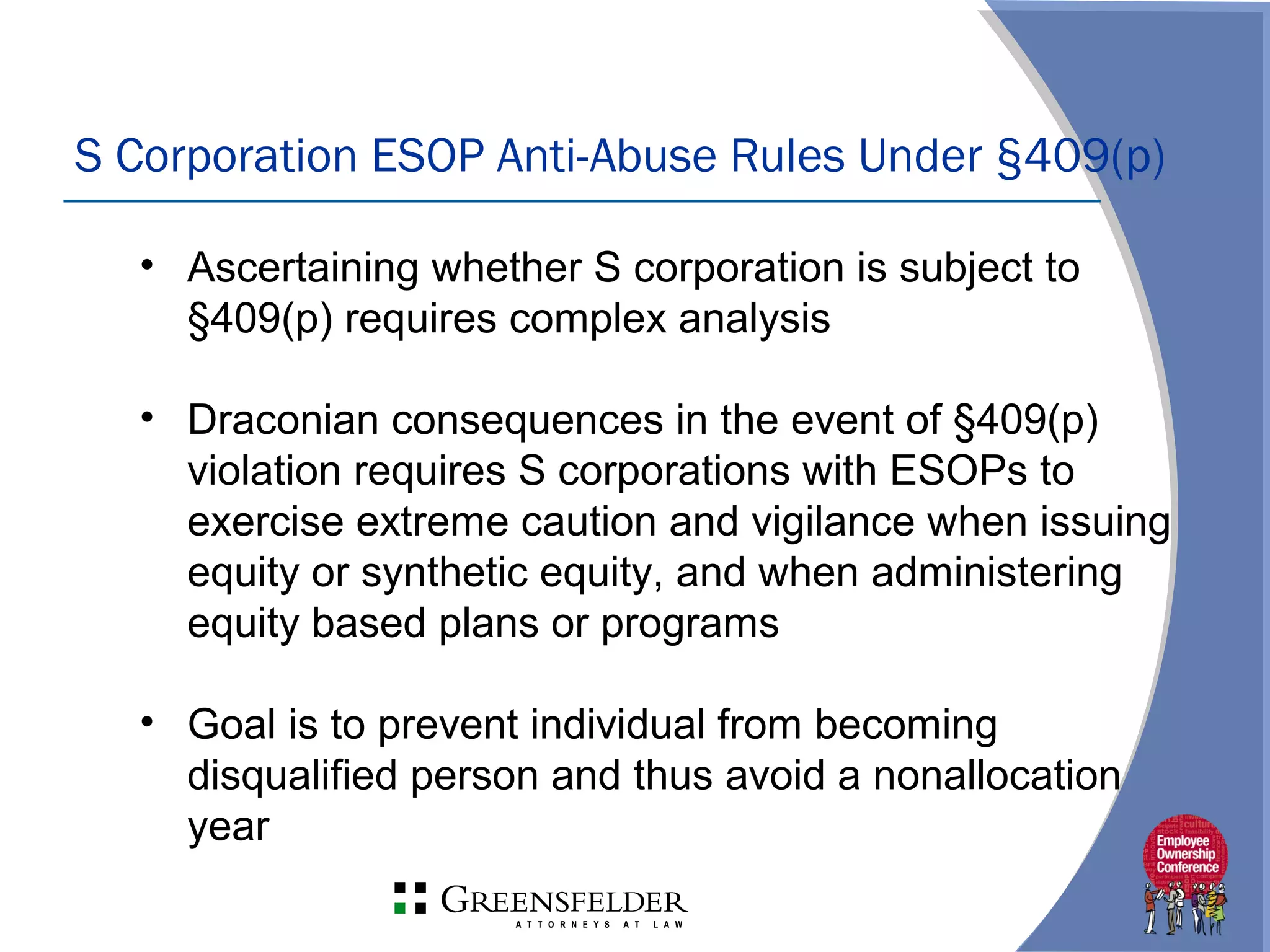

Daniel Janich presented on forms of executive compensation for privately-held companies. Executive compensation has grown more complex due to regulations like Sarbanes-Oxley, Section 409A, and securities laws. Privately-held companies need experienced advisors and a compensation philosophy when determining compensation. Components of compensation include salary, bonuses, deferred compensation, equity incentives, and benefits. Equity plans for S corporations require special consideration of Section 409(p)'s rules regarding disqualified individuals and nonallocation years.

![[DIY] Employee Stock Options the right way](https://cdn.slidesharecdn.com/ss_thumbnails/diymakingesopsmatter-190314055510-thumbnail.jpg?width=640&height=640&fit=bounds)