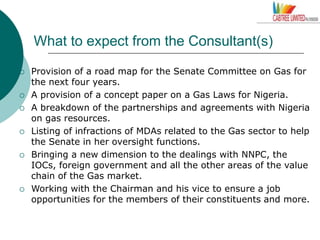

Sowunmi Olabode III from Cabtree Limited presented to the Senate Committee on Gas in April 2016. Some key points from the presentation include:

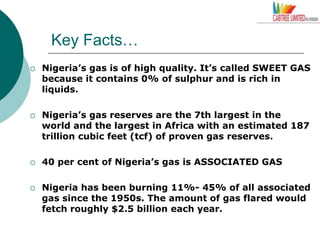

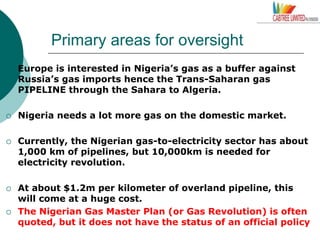

- Nigeria has significant natural gas reserves, being the 7th largest in the world and largest in Africa, however 40% is associated gas which is often flared.

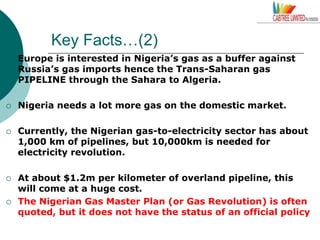

- There is interest from Europe in Nigerian gas to reduce reliance on Russian imports, however Nigeria also needs more gas for domestic use.

- Expanding gas infrastructure like pipelines will be costly, as the country currently only has 1,000 km of gas-to-electricity pipelines but requires 10,000 km for increased domestic use and exports.