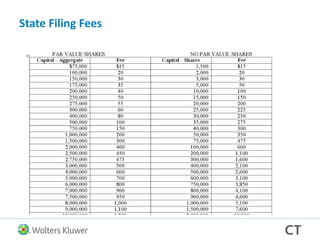

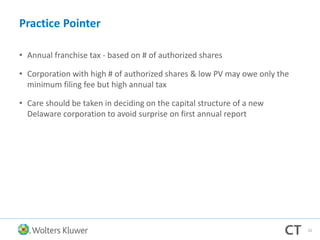

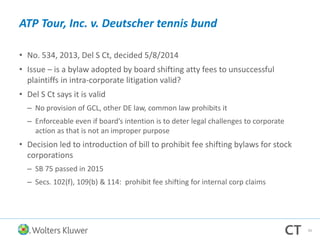

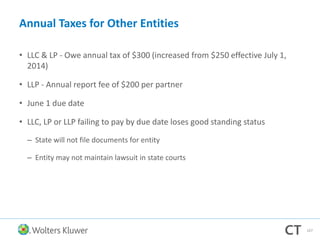

The document provides an overview of Delaware's business entity laws as of 2016, detailing reasons for Delaware's status as a leading formation state and outlining key legislations like the Delaware General Corporation Law and the Limited Liability Company Act. It covers the benefits of Delaware's legal framework, such as flexibility, efficiency, and a robust court system, along with procedural aspects like annual franchise taxes, document filing requirements, and common errors in corporate filings. Additionally, it highlights significant legal cases that influenced corporate governance and outlines the roles of directors and officers in corporate structures.