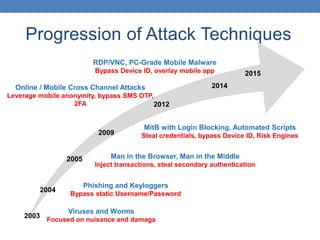

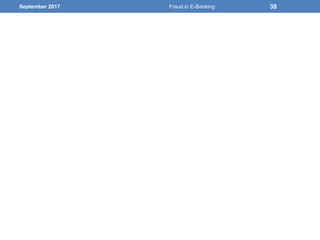

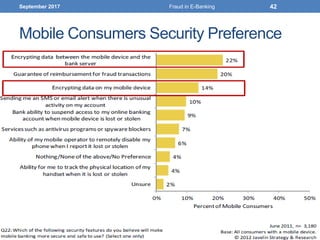

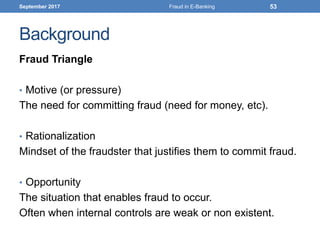

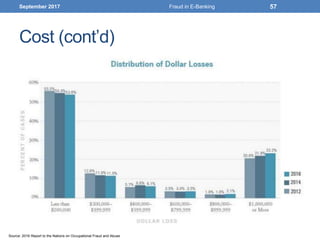

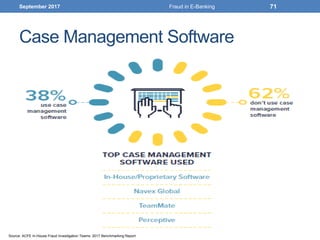

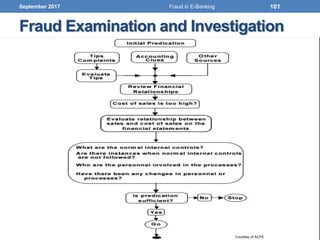

![September 2017

Source: IBM [1] UNODC Comprehensive Study on Cybercrime, 2013

23Fraud in E-Banking](https://image.slidesharecdn.com/dealingwithfraudinelectronicbankingsphereforparticipantv1-170916183855/85/Dealing-with-Fraud-in-E-Banking-Sphere-23-320.jpg)

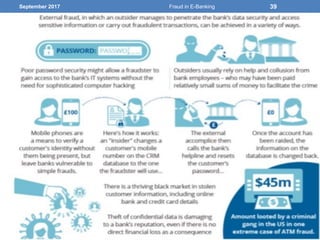

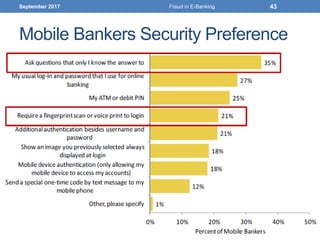

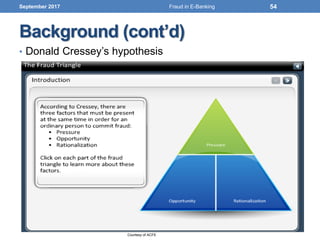

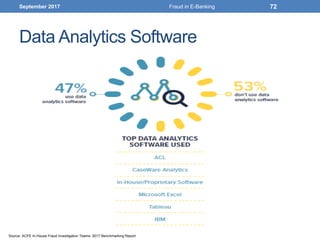

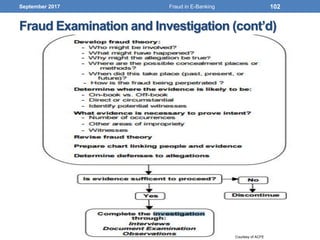

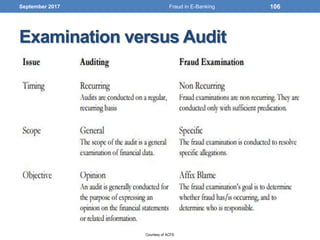

![September 2017

Source: IBM

[2] FBI: Crime in the United States 2013

[3] United California Bank Robbery

[4] Center for Strategic and International Studies

24Fraud in E-Banking](https://image.slidesharecdn.com/dealingwithfraudinelectronicbankingsphereforparticipantv1-170916183855/85/Dealing-with-Fraud-in-E-Banking-Sphere-24-320.jpg)

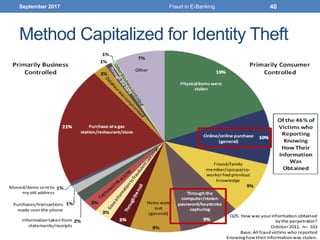

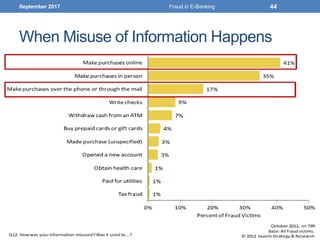

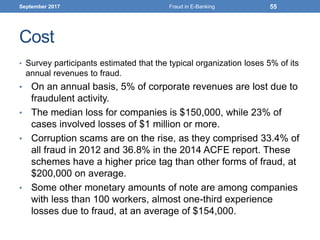

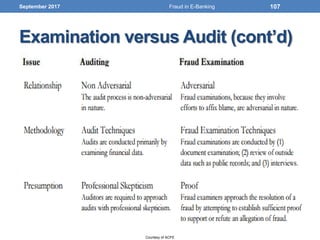

![September 2017

Source: IBM [6] ESG: http://bit.ly/1xzTmUW

25Fraud in E-Banking](https://image.slidesharecdn.com/dealingwithfraudinelectronicbankingsphereforparticipantv1-170916183855/85/Dealing-with-Fraud-in-E-Banking-Sphere-25-320.jpg)

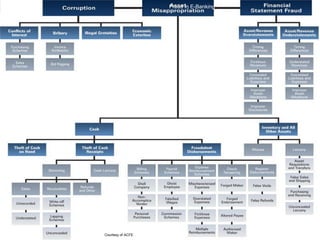

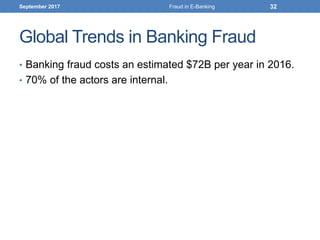

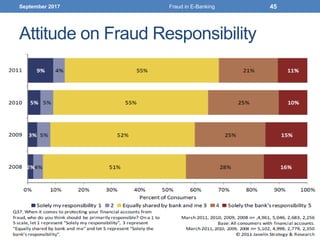

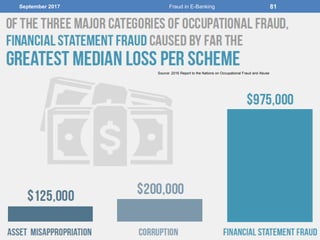

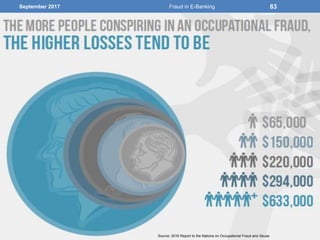

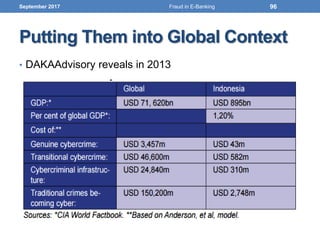

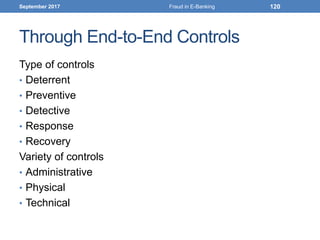

The document discusses the prevalence and impact of fraud within the electronic banking sector, outlining various definitions, types, and trends related to fraud. It highlights the significant costs of fraud, estimated at $72 billion annually, with a notable portion attributed to internal actors. Key areas of focus include the types of fraud occurring, methods of detection and investigation, and the importance of robust anti-fraud measures for organizations.