Download to read offline

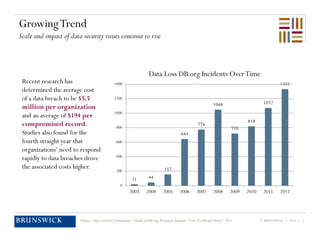

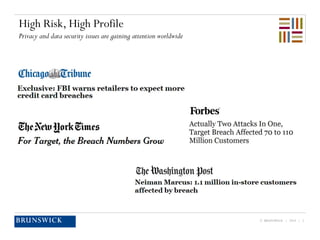

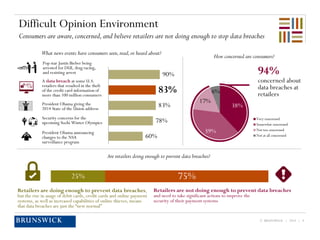

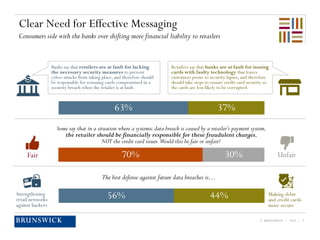

Data breaches are increasingly impactful, with an average cost of $5.5 million per incident, leading to a heated debate between retailers and banks over accountability. Consumers express significant concern about retailers' handling of data security, with a notable portion blaming them alongside criminals. A call for improved security measures has emerged, highlighting the need for effective communication and a shift in financial responsibility towards retailers in cases of breaches.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)