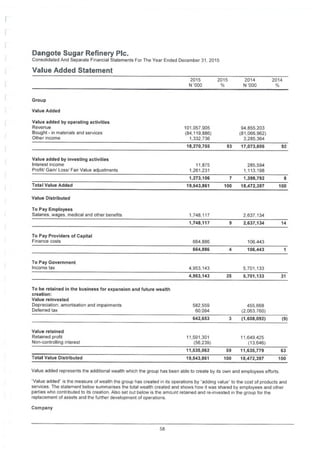

Downloaded 39 times

![Deloitte. PO Sox 96S

Marina

Lagos

Nigeria

Akintola Williams Deloitte

235 Ikorodu Road

llupe]u

Lagos

Nigeria

Tel; -234 (1) 271 7800

fax: -234 (1)271 7801

www.deloilte.com/ng

REPORT OF THE INDEPENDENT AUDITOR TO THE MEMBERS OF

DANGOTE SUGAR REFINERY PLC

We have audited the accompanying financial statements of Dangote Sugar Refinery Pic (“the Company”) and its subsidiary

(together referred to as the Group) which comprise the consolidated and separate statements of financial position as at 31

December 2015, the consolidated income statement, statement of changes in equity, statement of cash flows for the year then

ended 31 December 2015, a summary of significant accounting policies and other explanatory information.

Directors’ Responsibility for the Financial Statements

The Directors are responsible for the preparation and fair presentation of these financial statements in accordance with the

Companies and Allied Matters Act, CAP C20, LFN 2004, Financial Reporting Council of Nigeria Act 2011, the International

Financial Reeporting Standards and for such internal control as the Directors determine are necessary to enable the preparation

of financial statements that are free from material misstatements, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance

with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform

the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements.

The procedures selected depend on the auditors’ judgement, including the assessment of the risks of material misstatement of

the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control

relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal

control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting

estimates made by the Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements give a true and fair view of the financial position of Dangote Sugar Refinery Pic and its

subsidiaries as at 31 December 2015 and of its financial performance and cash flows for the year ended 31 December 2015 in

accordance with the Companies and Allied Matters Act CAP C20 LFN 2004 and the Financial Reporting Council of Nigeria Act,

2011 and the International Financial Reporting Standards.

Other reporting responsibilities

In accordance with the Sixth Schedule of Companies and Allied Matters Act CAP C20 LFN 2004, we expressly state that:

We have obtained all the information and explanation which to the best of our knowledge and believe were necessary for

the purpose of our audit.

i)

The Group has kept proper books of account, so far as appears from our examination of those books.ii)

iii) The Group’s financial position and its statement of profit or loss and other comprehensive income are in agreement with

the books of account.

Jelili Adebisi- FRC/2013/ICAN/000000004247

For: Akintola Williams Deloitte

Chartered Accountants

Lagos, Nigeria

/tt March 2016 St9«0

List of partners and partner equivalents available on the website

Associate of Deloitte Africa, a Member of Deloitte Touche Tohmatsu Limited](https://image.slidesharecdn.com/dangotesugarannualreport2015-170222135458/85/Dangote-sugar-annual-report-2015-5-320.jpg)

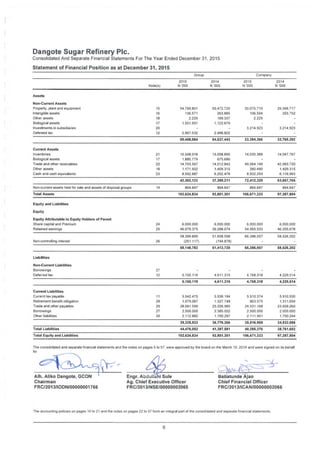

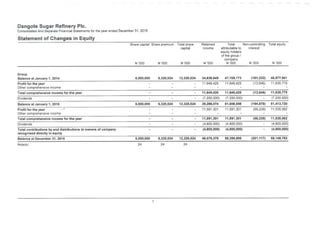

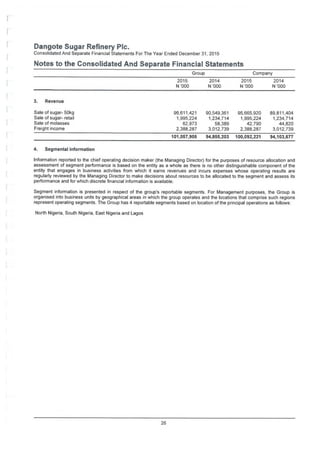

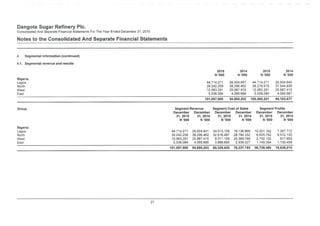

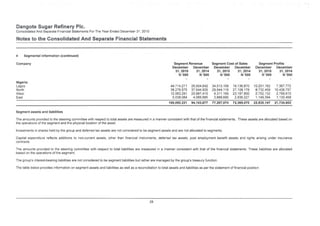

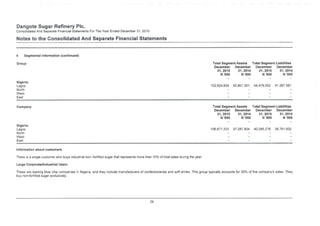

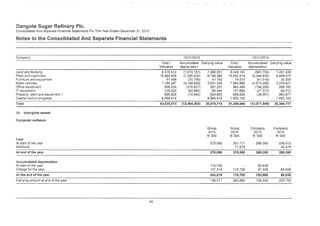

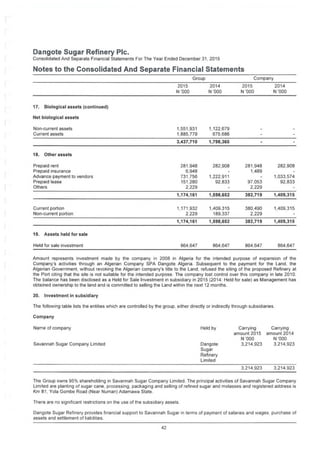

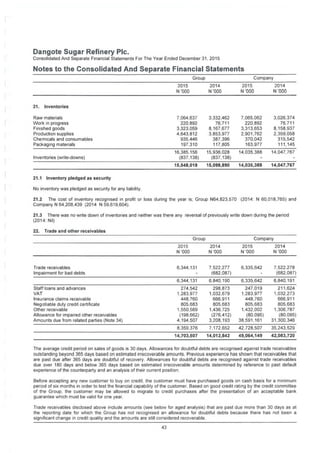

The document provides financial information for Dangote Sugar Refinery PLC for the year ended December 31, 2015. It includes the directors' responsibilities, independent auditor's report, consolidated and separate statements of profit or loss and other comprehensive income, financial position, changes in equity, and cash flows. The directors approved the financial statements on March 10, 2016. Key details include total revenue of N101 billion, profit for the year of N11.5 billion, total assets of N102.6 billion, and total equity of N58.1 billion.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)