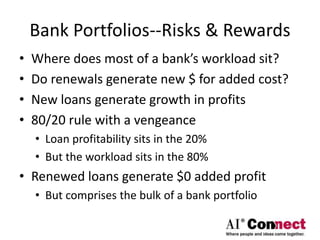

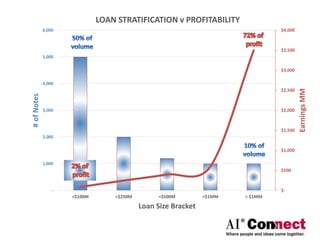

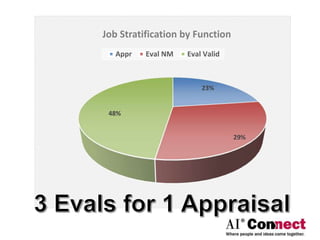

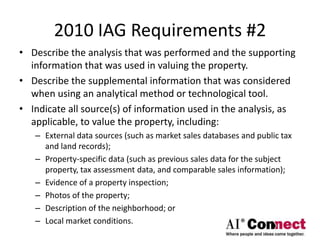

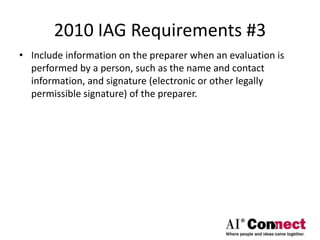

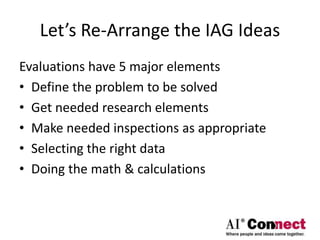

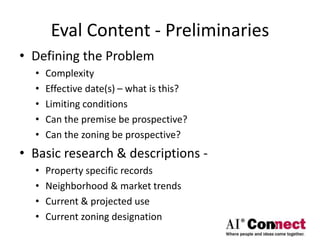

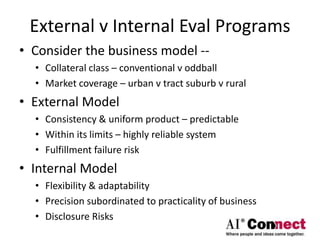

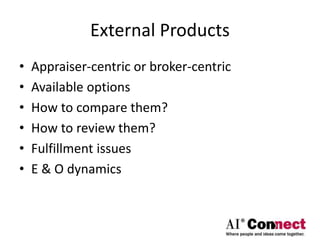

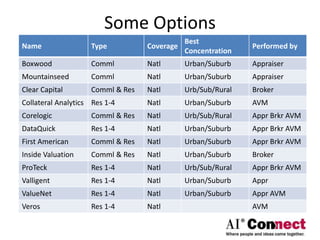

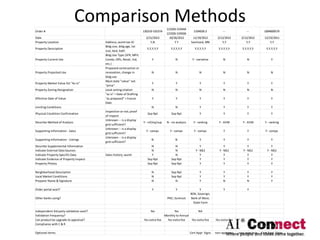

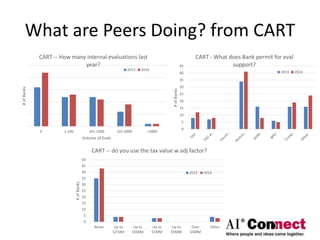

The document discusses the evaluation processes in bank lending, focusing on the regulatory requirements and necessary evaluations versus appraisals for various loan types. It highlights the complexities and risks associated with evaluations, including the 80/20 rule regarding profitability and workload, and the consequences of regulation B on lending practices. Additionally, it outlines vendor management, the significance of compliance, and trends in evaluation programs as banks consider internal versus external solutions.