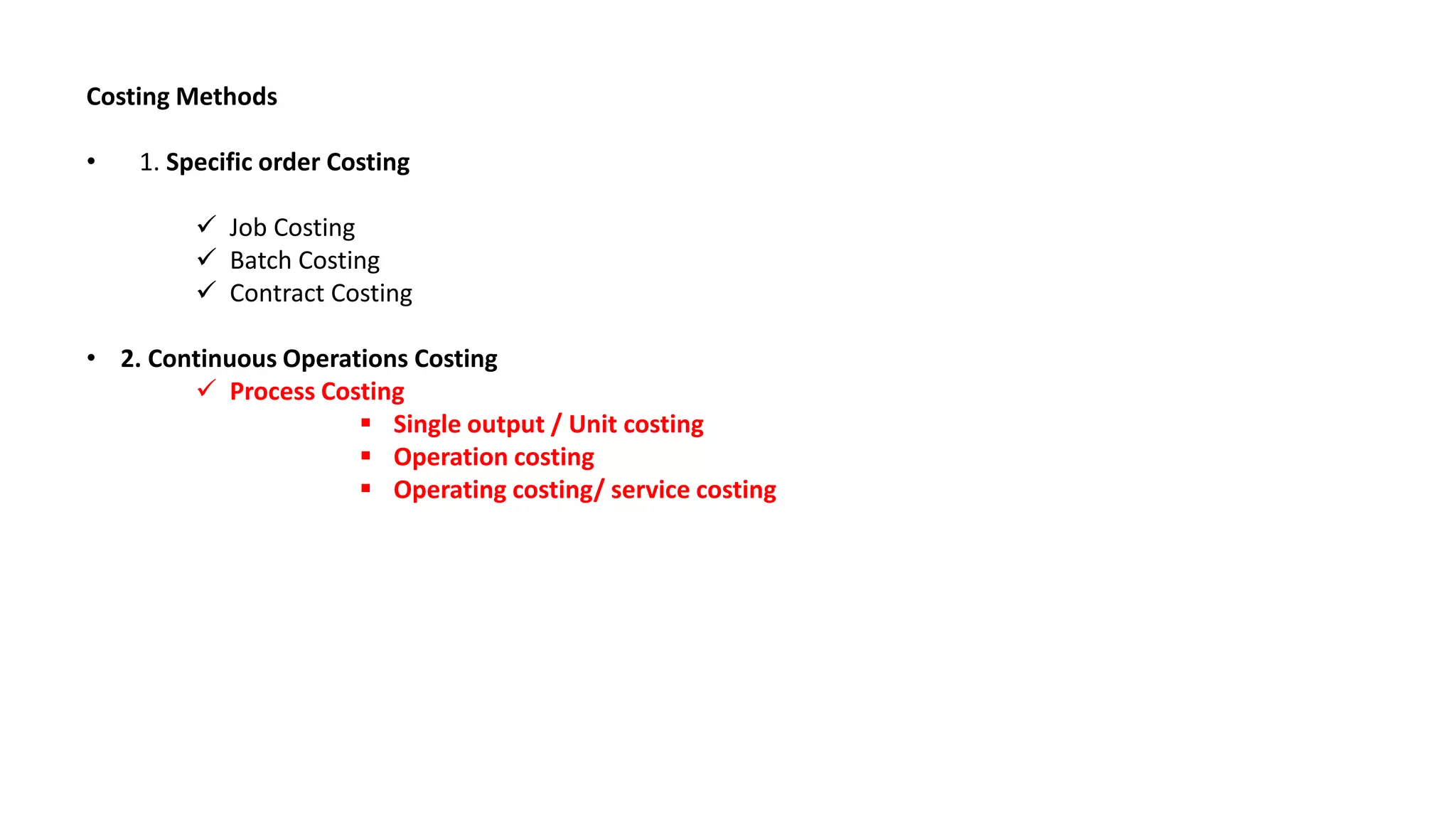

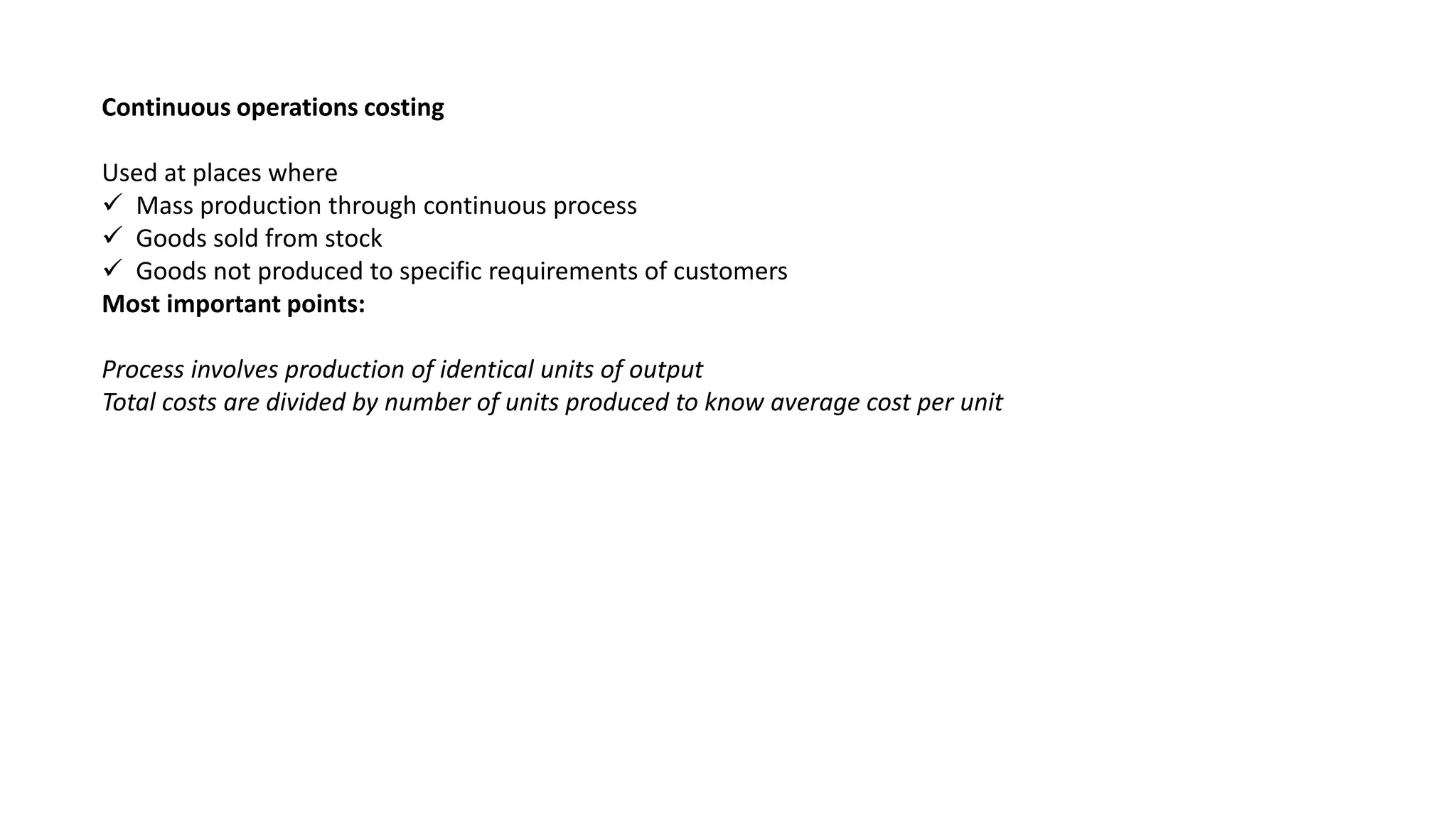

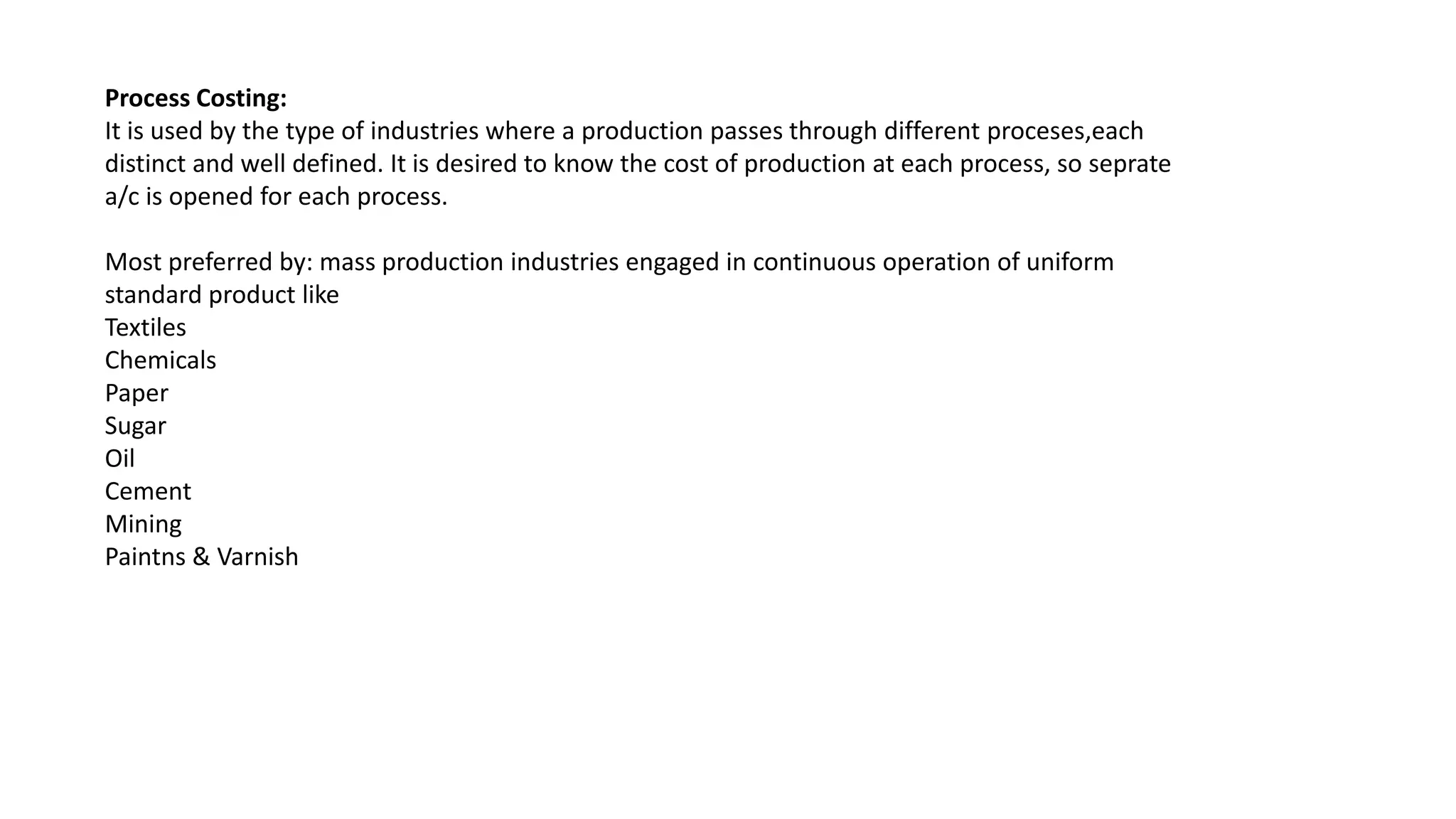

This document discusses different costing methods used in accounting. It outlines specific order costing methods like job, batch, and contract costing. It also discusses continuous operations costing methods like process costing which can be single output, operation, or operating costing. Process costing is preferred for mass production industries that have continuous operations and uniform standard products like textiles, chemicals, paper, sugar, oil, cement, mining, and paints & varnish.