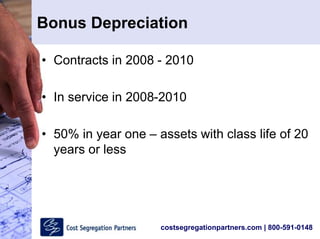

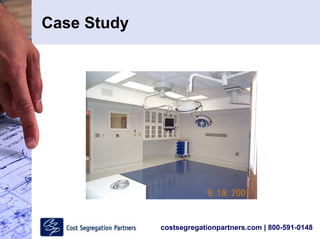

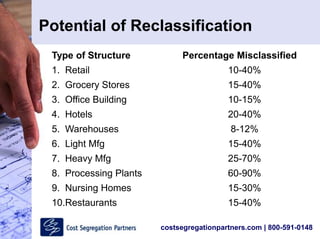

A cost segregation study comprehensively analyzes a commercial building to identify hidden personal or tangible property that can be depreciated over shorter tax periods, resulting in increased tax savings. Cost segregation studies analyze purchase costs, construction documents, and property components to classify portions of building costs, such as electrical, plumbing and HVAC, as assets with recovery periods of 5, 7, or 15 years rather than 39 years. Done properly, 15-50% of total costs can be segregated, providing increased depreciation deductions and cash flow through reduced tax liability.

![Cost Seg Slide Show Doc[1]](https://cdn.slidesharecdn.com/ss_thumbnails/costsegslideshowdoc1-12750742793667-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Cost Segregation PP - COBE - Updated 2015 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/77e09766-a95f-4fef-865a-da3d3dabe71b-150804191510-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)