Download as PDF, PPTX

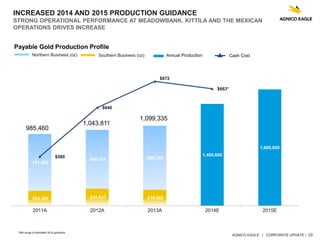

The document provides an update on Agnico Eagle, a gold mining company. It discusses forward-looking production guidance estimates for 2015, including expected ore grades, metal production, costs per ounce, and estimated timing of technical reports. It notes Agnico Eagle expects around 14% production growth in 2015 and all-in sustaining costs in 2015 are expected to decline by 6% from 2014 levels. The document also contains standard cautionary notes about forward-looking statements and the use of non-GAAP measures in evaluations performance.