The document analyzes the current state of the US economy and argues that while GDP and unemployment rates show recovery, income inequality has increased. It summarizes that GDP and unemployment have improved significantly since the recession but wages have grown slowly, many workers are underemployed or dropped from the labor force, and gains have disproportionately benefited the wealthy while median income has declined.

![deficit would only account for 3% of GDP, yet until 2013, the deficit accounted for roughly 7%

of GDP (Freeman).

Despite its criticisms, we still believe the fiscal and monetary policies were successful.

However, we believe the policies that aided the recovery benefited some more than others. For

instance, in lowering the federal funds rate, the prudent savers of the economy suffered as

interest rates declined. The elderly were also negatively affected as they generally have large

savings accounts. In addition, while quantitative easing successfully increased credit availability

for the public, it also implicitly rewarded banks for their risky behavior that caused the recession.

In buying the banks faulty mortgage backed securities, the Fed took the hit for their irresponsible

lending practices. The fiscal policies implemented in response to the recession also came with

mixed results. The TARP act, pushed through Congress with the message of “save our great auto

industry,” bailed out many of the same financial institutions that contributed to the housing

market crash. While the taxpayer funded bailout has been repaid, the underlying message that

large scale fraudulent behavior goes largely unpunished is troubling for the future of our society.

Mr. Sanders has been very opinionated as to his views of both the Federal Reserve and

recent fiscal policy measures. Regarding the Fed’s policy of quantitative easing, Sanders has

stated that while “well intentioned” it requires reformation to better serve every day Americans

(Sanders). He pushes for the removal of conflicts of interest within the Fed writing “unfortunately,

an institution that was created to serve all Americans has been hijacked by the very bankers it

regulates” (Sanders). Additionally, Sanders is opposed to raising interest rates because he believes

that will hurt small business owners looking to make investments. As for his views on fiscal

policy measures, Sanders was extremely critical of the TARP Act of 2008. In particular, Sanders

was displeased with the idea of a bank bailout, however he did not oppose the bailout of the

automakers because that would have led to a loss in thousands of middleclass jobs (Sanders).

Regarding other figures in the political field, both Hillary Clinton and Ted Cruz agree on

the need for a balance budget. Cruz has introduced a balanced budget amendment and Clinton

urges voters to “Look back to 1990s to see how [she would] be fiscally responsible” (Clinton).

The candidates differ in their views of the Fed. Cruz views their actions as guesswork and insists

that “they are debasing the currency with QE1, QE2, QE infinity!” (Cruz). However, he

acknowledges the necessity for a lender of last resort. Clinton appears more moderate,

advocating the effectiveness of the Fed’s actions and firmly supporting QE.

7](https://image.slidesharecdn.com/c3ebdf4c-0358-4677-b0a5-2f18904852f9-160629175004/85/CopyofProject3FinalAnalysisofUSEconomy-8-320.jpg)

![Amadeo, Kimberly. “What Was the Bank Bailout Bill?” Last modified March 26, 2016.

http://useconomy.about.com/od/criticalssues/a/govt_bailout.htm

Bernanke, Ben. “The Crisis and the Policy Response” (speech presented at the Stamp Lecture,

London School of Economics, London, England, January 13, 2009).

“Bernie Sanders on Free Trade.” On the Issues. Last modified April 23rd, 2016. Accessed April

25th, 2016. http://www.ontheissues.org/Free_Trade.htm#Bernie_Sanders

Blinder, Alan S. and Mark Zandi. “The Financial Crisis: Lessons for the Next One.” Center on

Budget and Policy Priorities. October 15, 2015. Accessed April 6th, 2016.

http://www.cbpp.org/research/economy/thefinancialcrisislessonsforthenextone

Board of Governors of the Federal Reserve System (US), Commercial and Industrial Loans. All

Commercial Banks [BUSLOANS], retrieved from FRED. Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/BUSLOANS, April 4, 2016.

Bohn, Henning. “The Economic Consequences of Rising U.S. Government Debt: Privileges at

Risk.” Journal of Economic Literature July (2011): 123. Accessed April 23rd, 2016.

http://www.econ.ucsb.edu/~bohn/papers/BohnDebtConsequences.pdf

Carvalho, Carlos, Stefano Eusepi, Christian Giasse. “Policy Initiatives in the Global Recessio:

What Did Forecasters Expect?” Federal Reserve Bank of New York. Volume 18 (2012).

Accessed March 29, 2016.

“Congressional Budget Office,” accessed April 22nd, 2016,

https://www.cbo.gov/topics/budget

Engen, Eric M and Glenn Hubbard. “Federal Government Debt and Interest Rates.” National

Bureau of Economic Research Vol 19 (2005): 83162. Accessed April 24th, 2016

http://www.nber.org/chapters/c6669.pdf

“The Federal Reserve’s Response to the Financial Crisis and Actions to Foster Maximum

Employment and Price Stability.” Last modified June 4, 2015.

https://www.federalreserve.gov/monetarypolicy/bst_crisisresponse.htm

FOMC Press Release. Last modified March 16, 2016.

https://www.federalreserve.gov/newsevents/press/monetary/20160316a.htm

12](https://image.slidesharecdn.com/c3ebdf4c-0358-4677-b0a5-2f18904852f9-160629175004/85/CopyofProject3FinalAnalysisofUSEconomy-13-320.jpg)

![Long, Heather. “US Has Lost 5 Million Manufacturing Jobs Since 2000.” CNN Money. March

29th, 2016. Accessed April 25th, 2016.

http://money.cnn.com/2016/03/29/news/economy/usmanufacturingjobs

“Monthly Budget Review for March 2016,” Congressional Budget Office, accessed April 23rd,

2016,

https://www.cbo.gov/sites/default/files/114thcongress20152016/reports/51442MBR.pdf

“Monthly Treasury Statement,” accessed April 23rd, 2016,

https://www.fiscal.treasury.gov/fsreports/rpt/mthTreasStmt/mts0216.pdf

“The Politics and Elections Portal.” Last modified January 3, 2016.

http://2016.presidentialcandidates.org/Clinton/?on=deficitdebt

Rudebusch, Glenn D. “The Fed’s Monetary Policy Response to the Current Crisis.” Federal

Reserve Bank of San Francisco. May 22, 2009. Accessed March 22, 2016.

http://www.frbsf.org/economicresearch/publications/economicletter/2009/may/fedmonetaryp

olicycrisis/

S&P Dow Jones Indices LLC, Dow Jones Industrial Average© [DJIA]. Retrieved from FRED.

Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/DJIA. February 11,

2016.

Sanders, Bernie. “To Rein in Wall Street, Fix the Fed.” The New York Times. December 23,

2015. accessed March 26, 2016

http://www.nytimes.com/2015/12/23/opinion/berniesanderstoreininwallstreetfixthefed.ht

ml?_r=0

Singh, J, “Revenue and Capital Receipts of Government Receipts: It’s Definition and

Differences,” accessed April 22nd, 2016,

http://www.economicsdiscussion.net/revenue/revenueandcapitalreceiptsofgovernmentreceip

tsitsdefinitionanddifferences/765

US. Bureau of the Census, Real Median Household Income in the United

States[MEHOINUSA672N], retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/MEHOINUSA672N, February 14, 2016.

14](https://image.slidesharecdn.com/c3ebdf4c-0358-4677-b0a5-2f18904852f9-160629175004/85/CopyofProject3FinalAnalysisofUSEconomy-15-320.jpg)

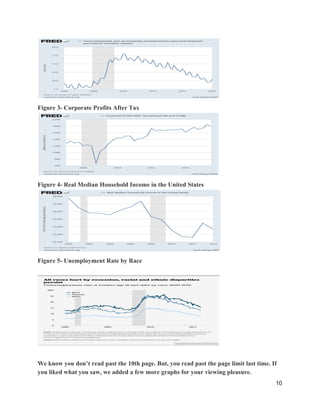

![US. Bureau of Economic Analysis, Corporate Profits After Tax (without IVA and CCAdj) [CP],

retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/CP, February 12, 2016.

US. Bureau of Economic Analysis, Federal government budget surplus or deficit ()

[M318501A027NBEA], retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/M318501A027NBEA, April 23, 2016.

US. Bureau of Economic Analysis, Real Gross Domestic Product [A191RO1Q156NBEA],

retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/A191RO1Q156NBEA, February 14, 2016.

US. Bureau of Economic Analysis, Real Gross Private Domestic Investment[GPDICA],

retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/GPDICA, April 4, 2016.

US. Bureau of Labor Statistics, Civilian Unemployment Rate [UNRATE], retrieved from FRED,

Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/UNRATE, April 4,

2016.

US. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items

[CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/CPIAUCSL, April 4, 2016.

US. Bureau of Labor Statistics, Employed full time: Median usual weekly real earnings: Wage

and salary workers: 16 years and over [LES1252881600Q], retrieved from FRED, Federal

Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/LES1252881600Q, April 4,

2016.

US. Bureau of Labor Statistics, Total unemployed, plus all marginally attached workers plus

total employed part time for economic reasons [U6RATENSA], retrieved from FRED, Federal

Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/U6RATENSA, February

14, 2016.

US. Department of the Treasury. Fiscal Service, Federal Debt: Total Public Debt[GFDEBTN],

retrieved from FRED, Federal Reserve Bank of St. Louis

https://research.stlouisfed.org/fred2/series/GFDEBTN, April 23, 2016.

15](https://image.slidesharecdn.com/c3ebdf4c-0358-4677-b0a5-2f18904852f9-160629175004/85/CopyofProject3FinalAnalysisofUSEconomy-16-320.jpg)

![4th Qtr Year End 2011 Economic Review Feb 15 [Autosaved] [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/4thqtryearend2011economicreviewfeb15autosavedautosaved-13439227651427-phpapp01-120802105911-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)