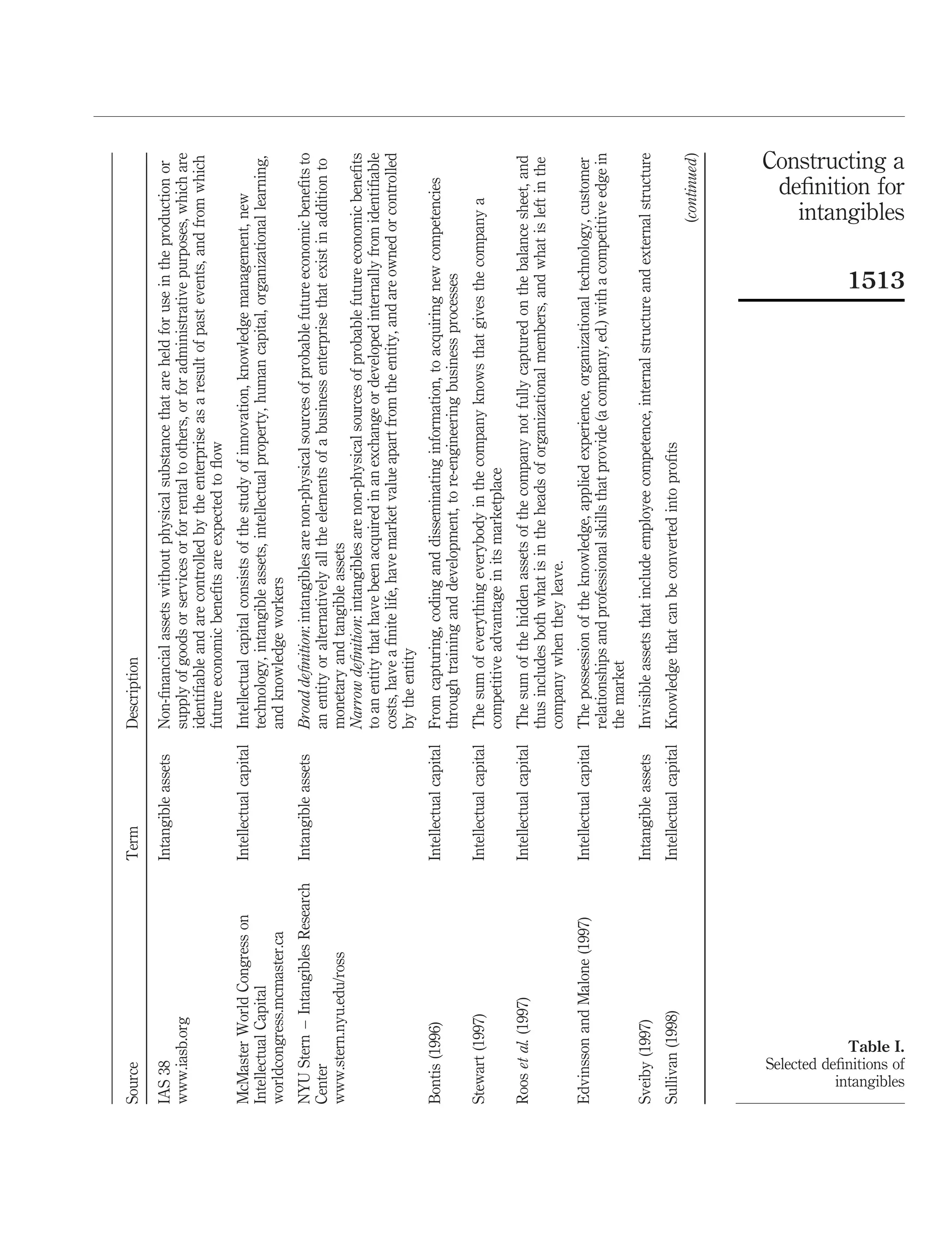

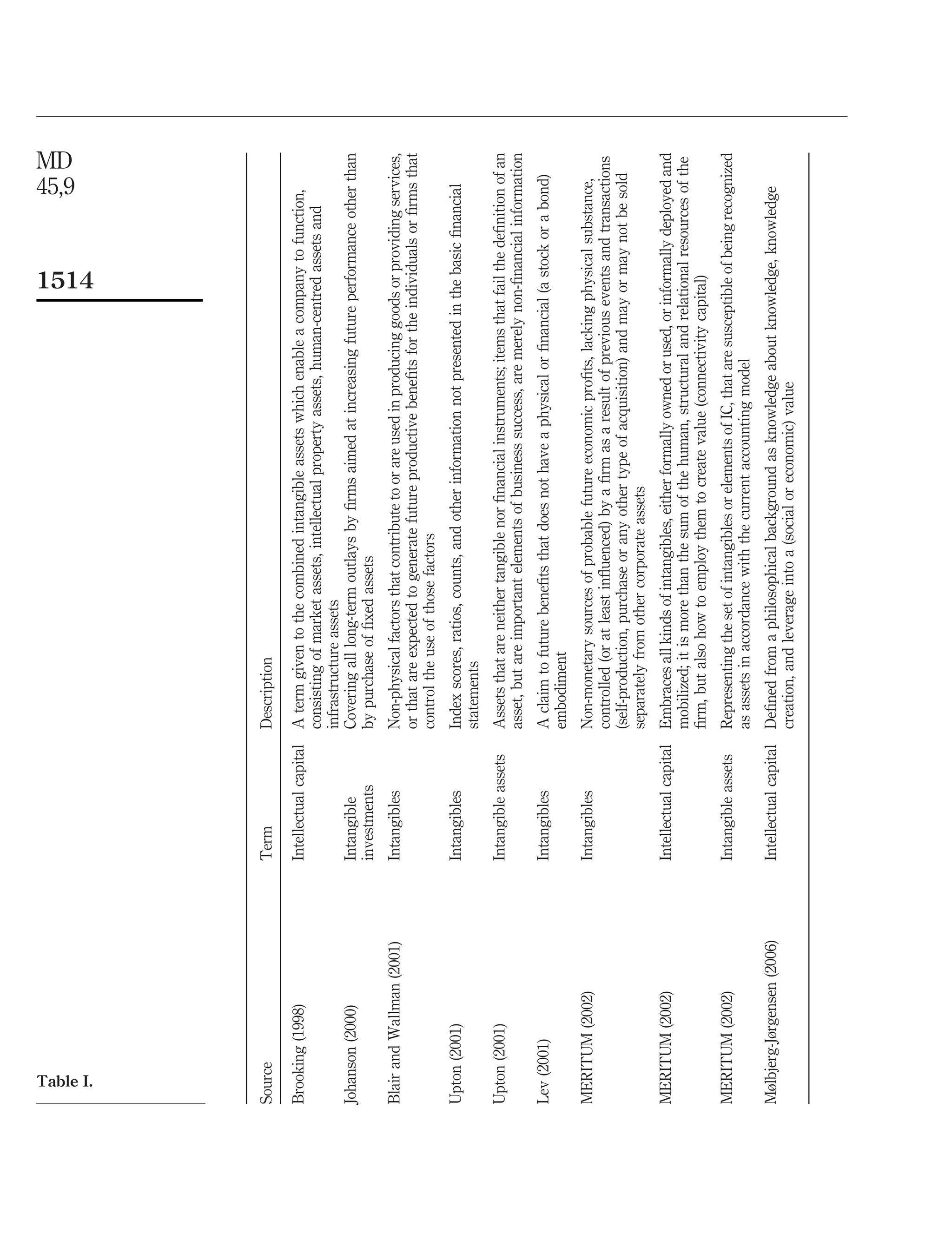

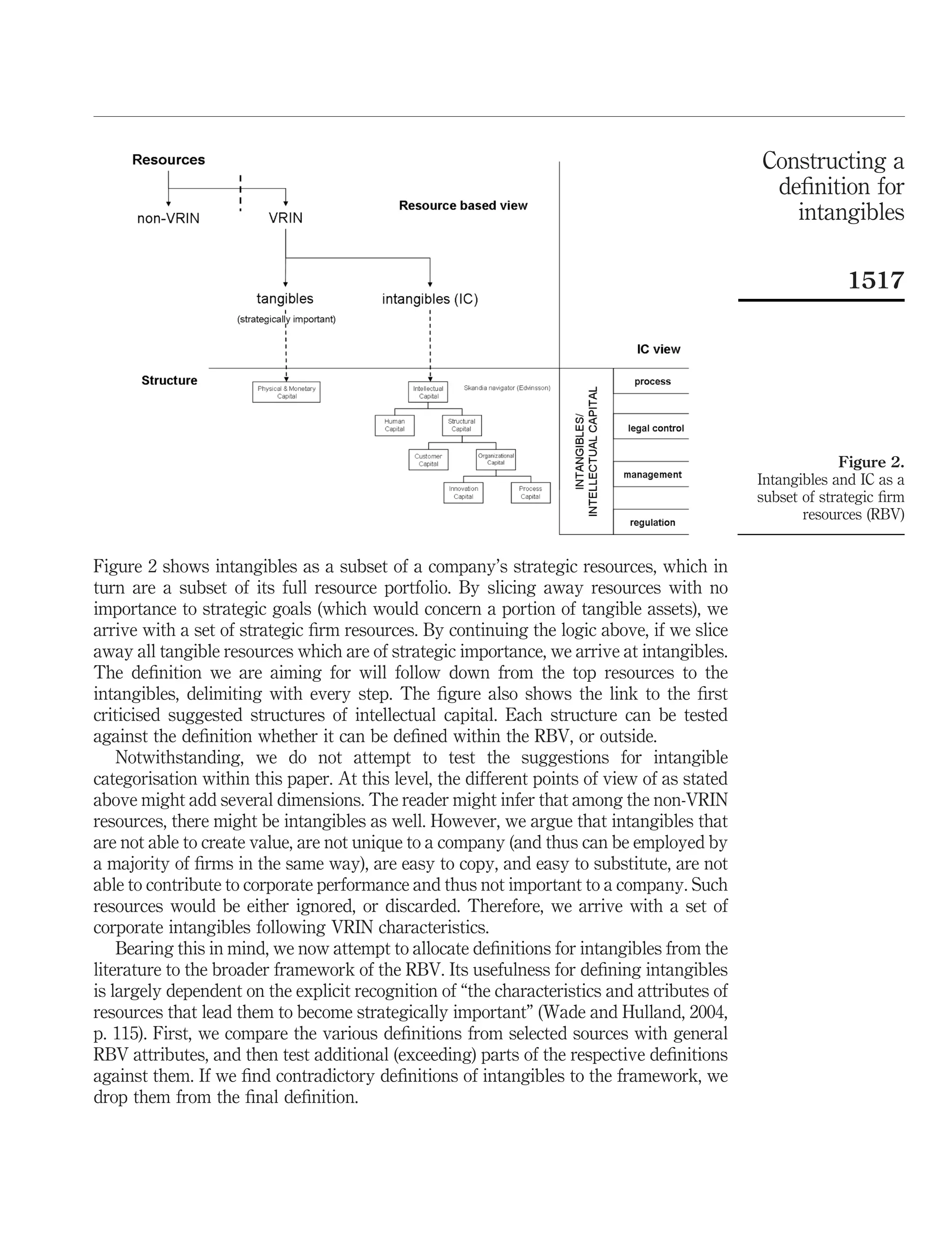

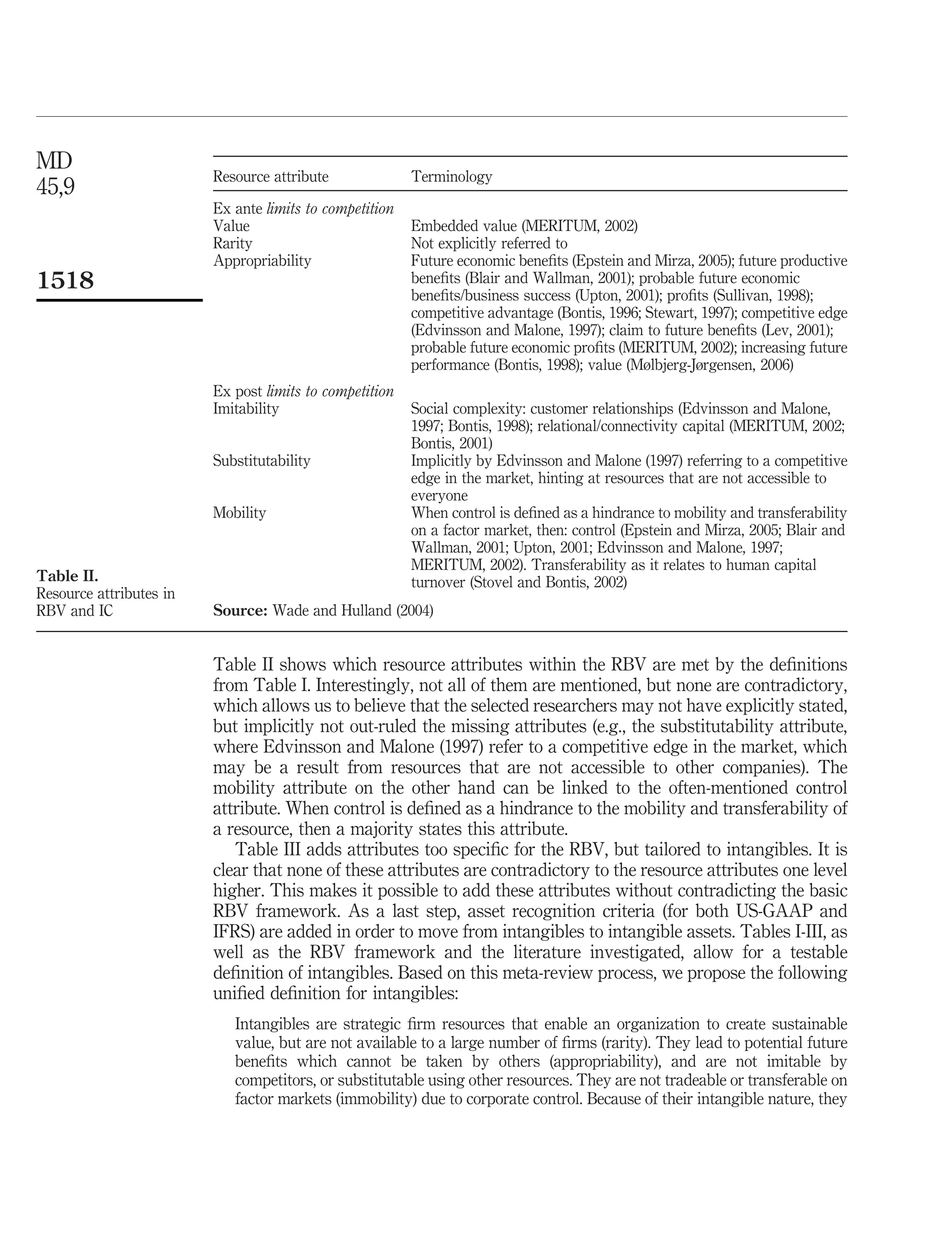

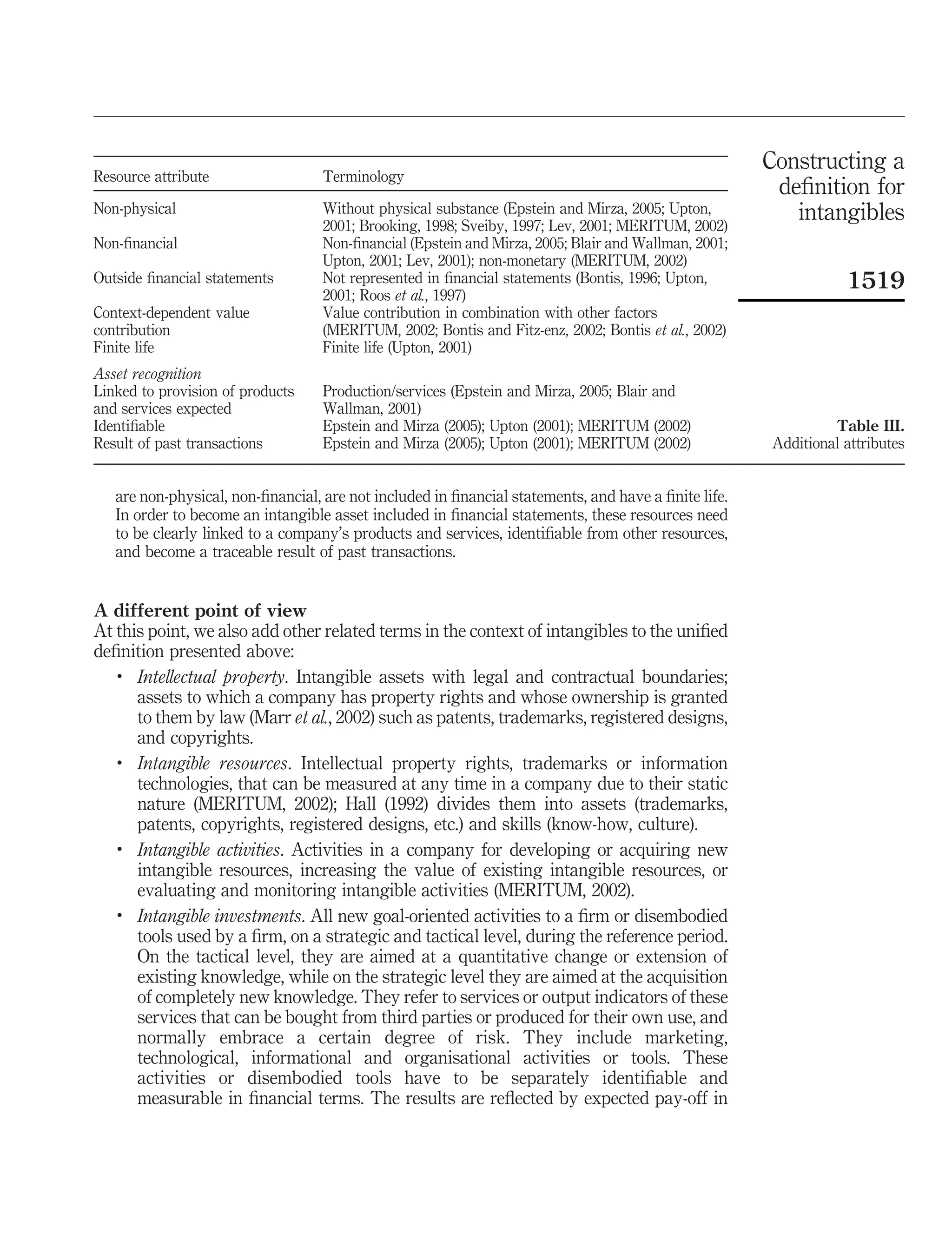

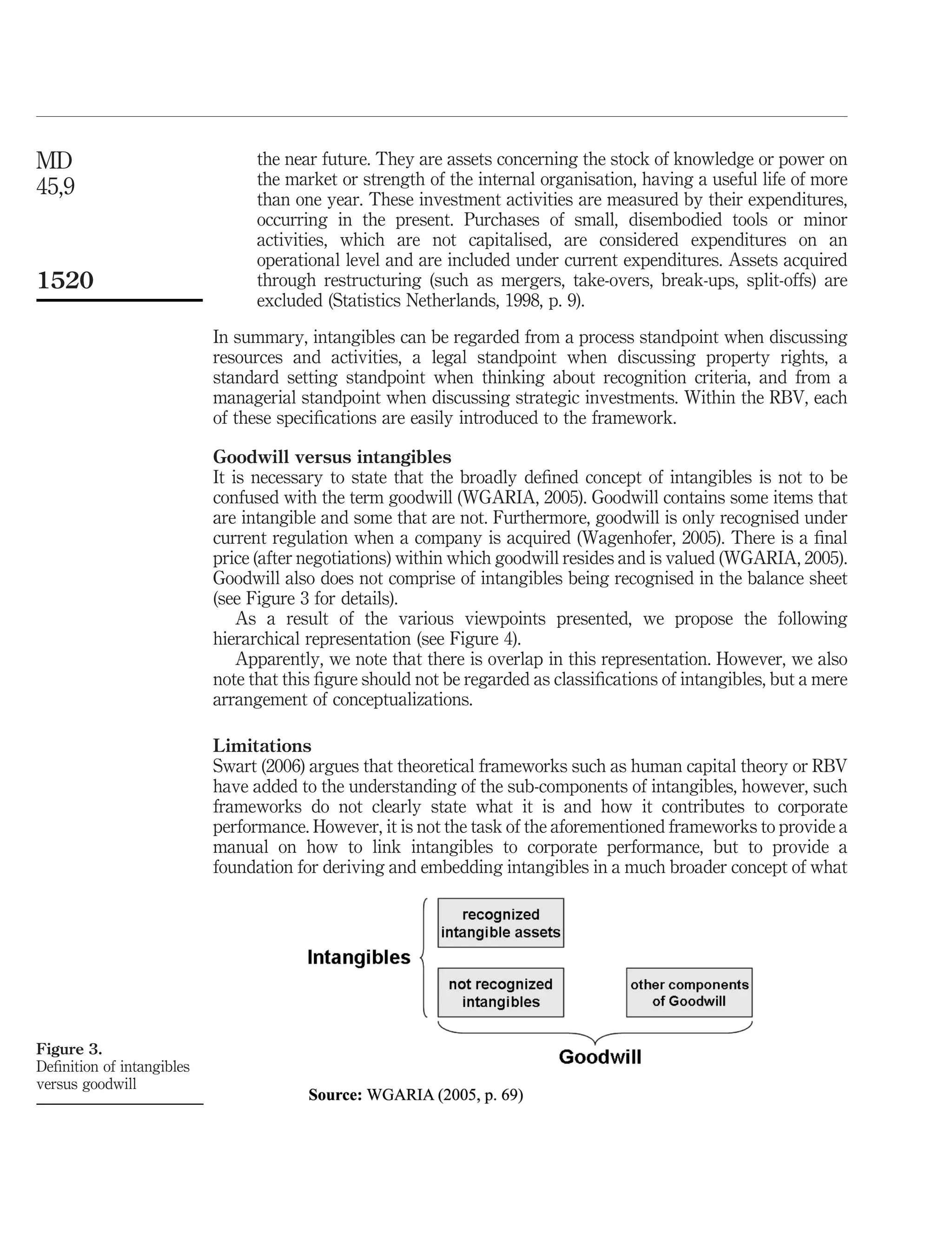

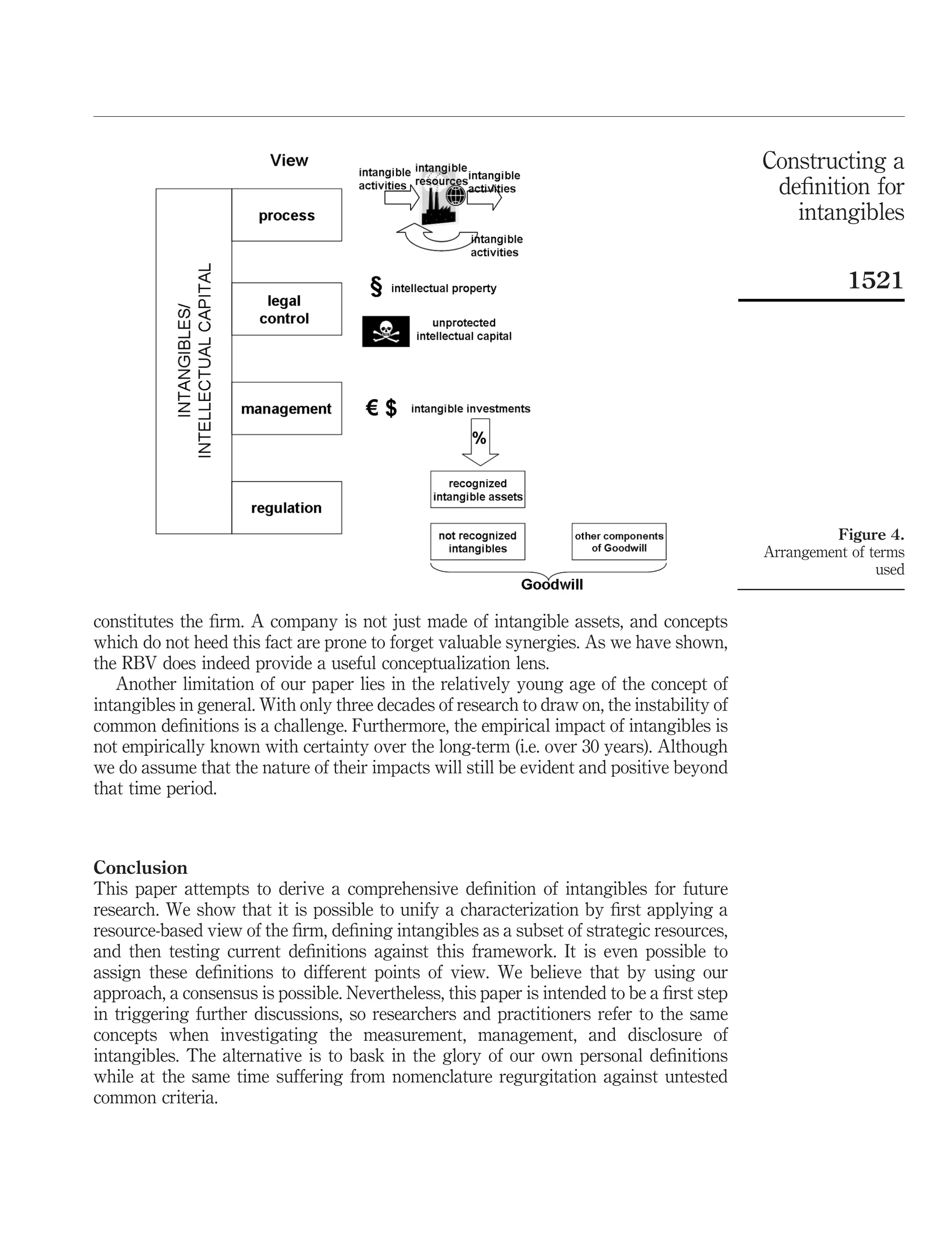

This document discusses various definitions of intangibles that have been proposed in the literature and aims to derive a common definition using the resource-based view of the firm. It reviews definitions that define intangibles based on what they are not (tangible assets), and those that categorize intangibles without defining the overall concept. The resource-based view suggests intangibles should be valuable, rare, inimitable, non-substitutable resources that generate sustained competitive advantage. The document proposes using this framework to construct a unified definition of intangibles.

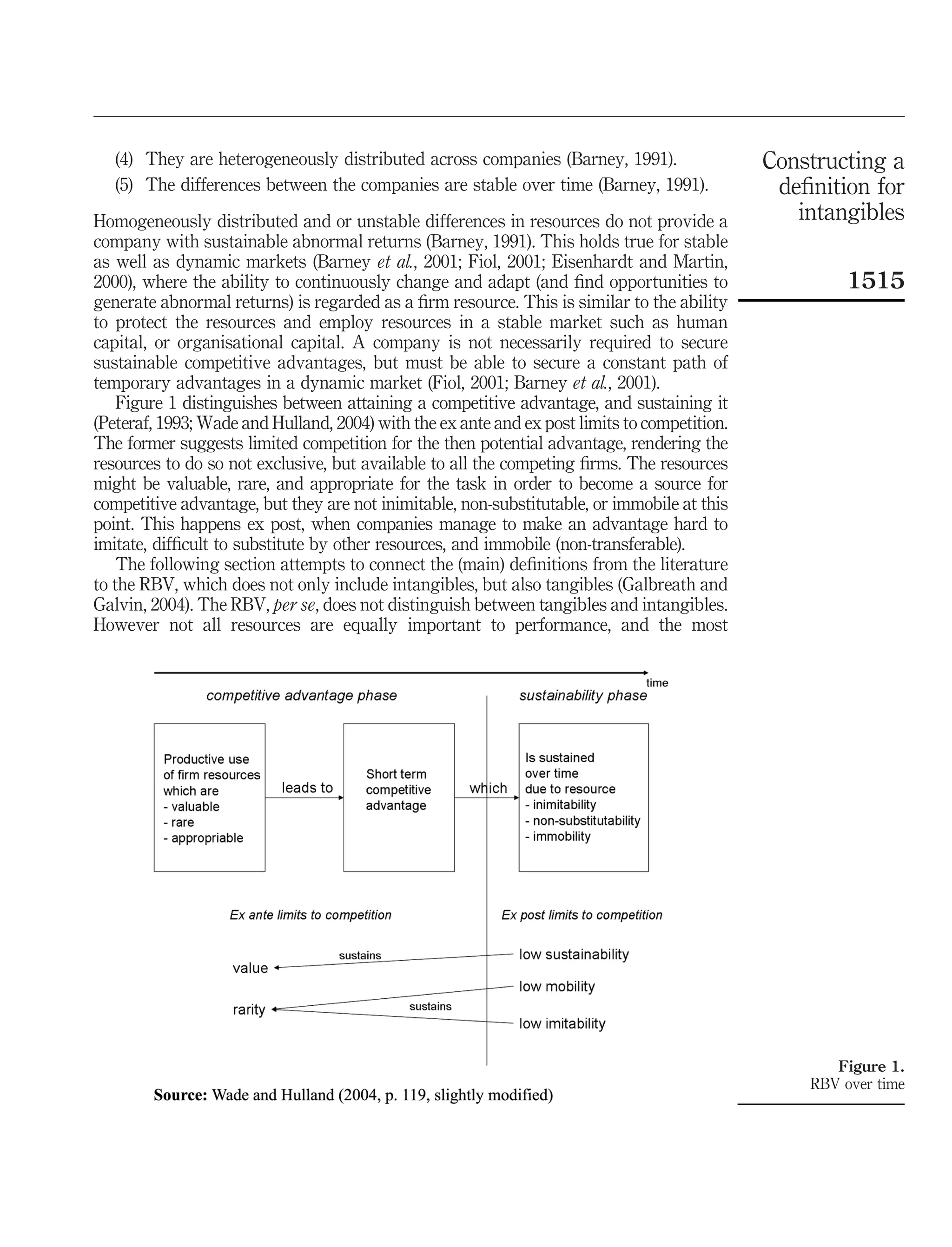

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)