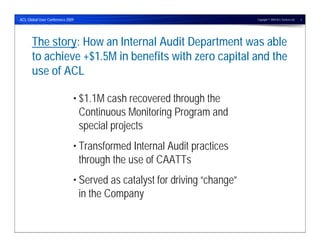

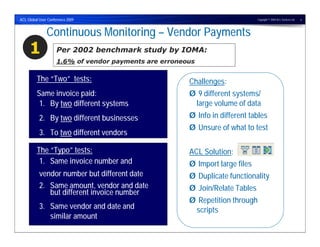

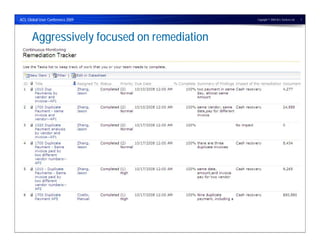

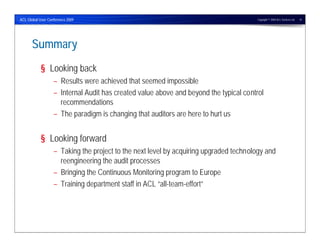

The internal audit department at Stanley Works was able to achieve over $1.5 million in benefits using ACL software with no capital expenditure. They recovered $1.1 million through a continuous monitoring program and special projects, transformed audit practices by introducing computer-assisted audit techniques, and drove change within the company. The department used ACL to perform duplicate payment analysis, payroll fraud detection, and analytical procedures to audit areas of risk. Looking back, results seemed impossible but value was created, and looking forward the department plans to expand programs and train staff on ACL.