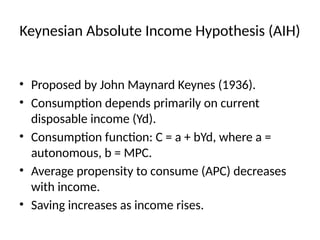

Keynesian Absolute IncomeHypothesis (AIH)

• Proposed by John Maynard Keynes (1936).

• Consumption depends primarily on current

disposable income (Yd).

• Consumption function: C = a + bYd, where a =

autonomous, b = MPC.

• Average propensity to consume (APC) decreases

with income.

• Saving increases as income rises.

3.

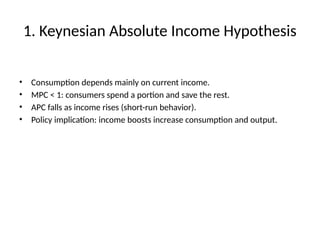

1. Keynesian AbsoluteIncome Hypothesis

• Consumption depends mainly on current income.

• MPC < 1: consumers spend a portion and save the rest.

• APC falls as income rises (short-run behavior).

• Policy implication: income boosts increase consumption and output.

4.

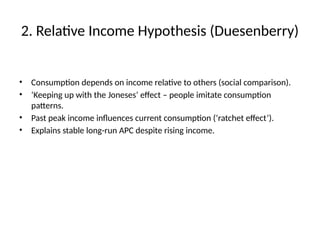

2. Relative IncomeHypothesis (Duesenberry)

• Consumption depends on income relative to others (social comparison).

• ‘Keeping up with the Joneses’ effect – people imitate consumption

patterns.

• Past peak income influences current consumption (‘ratchet effect’).

• Explains stable long-run APC despite rising income.

5.

3. Fisher’s IntertemporalModel of

Consumption

• Consumers maximize lifetime utility subject to intertemporal budget

constraint.

• Choice between current and future consumption depends on interest rate

(r).

• Borrowing and saving smooth consumption over time.

• Core equation: C1 + C2/(1+r) = Y1 + Y2/(1+r).

6.

4. Modigliani’s Life-CycleHypothesis

• Consumption and saving depend on expected lifetime income, not just

current income.

• Individuals save during working years and dissave in retirement.

• Consumption smoothing: goal is stable consumption throughout life.

• Formula: C = aW + bY (W=wealth, Y=current income).

7.

5. Friedman’s PermanentIncome Hypothesis

• Current income = Permanent + Transitory income (Y = Yp + Yt).

• Consumption depends mainly on permanent income (C = aYp).

• Temporary income changes lead to saving, not spending.

• Explains why short-run APC fluctuates but long-run APC is stable.

8.

Comparison Summary

• Keynes:Consumption depends on current income.

• Duesenberry: Relative income and habits matter.

• Fisher: Consumers optimize across time with interest rate influence.

• Modigliani: Life-stage planning drives consumption/saving behavior.

• Friedman: Consumption reflects permanent, not temporary, income.

Editor's Notes

#2 Keynes viewed consumption as linked to current income. Poor households spend most of their income, while richer ones save more. This model doesn’t include future expectations.

#3 Explain that Keynes believed people consume based on what they currently earn, not future expectations. Use a simple upward-sloping C-Y diagram where the consumption line starts above origin (autonomous consumption).

#4 Highlight how social norms and habits matter more than just income level. Show a figure comparing two families with different relative incomes but similar consumption patterns.

#5 Discuss trade-offs between consuming today or tomorrow. Use a two-period diagram showing budget constraint and indifference curves intersecting at equilibrium.

#6 Show a diagram with age on x-axis and income, consumption, and saving curves. Explain how people build up wealth mid-life and run it down later.

#7 Use a figure showing Y (current) fluctuating around Yp (permanent). Emphasize smoothing behavior and how people respond differently to temporary income changes.

#8 Summarize that all theories attempt to explain why consumption doesn’t move one-for-one with income, but differ in focus: current vs lifetime vs social vs permanent components.