Downloaded 13 times

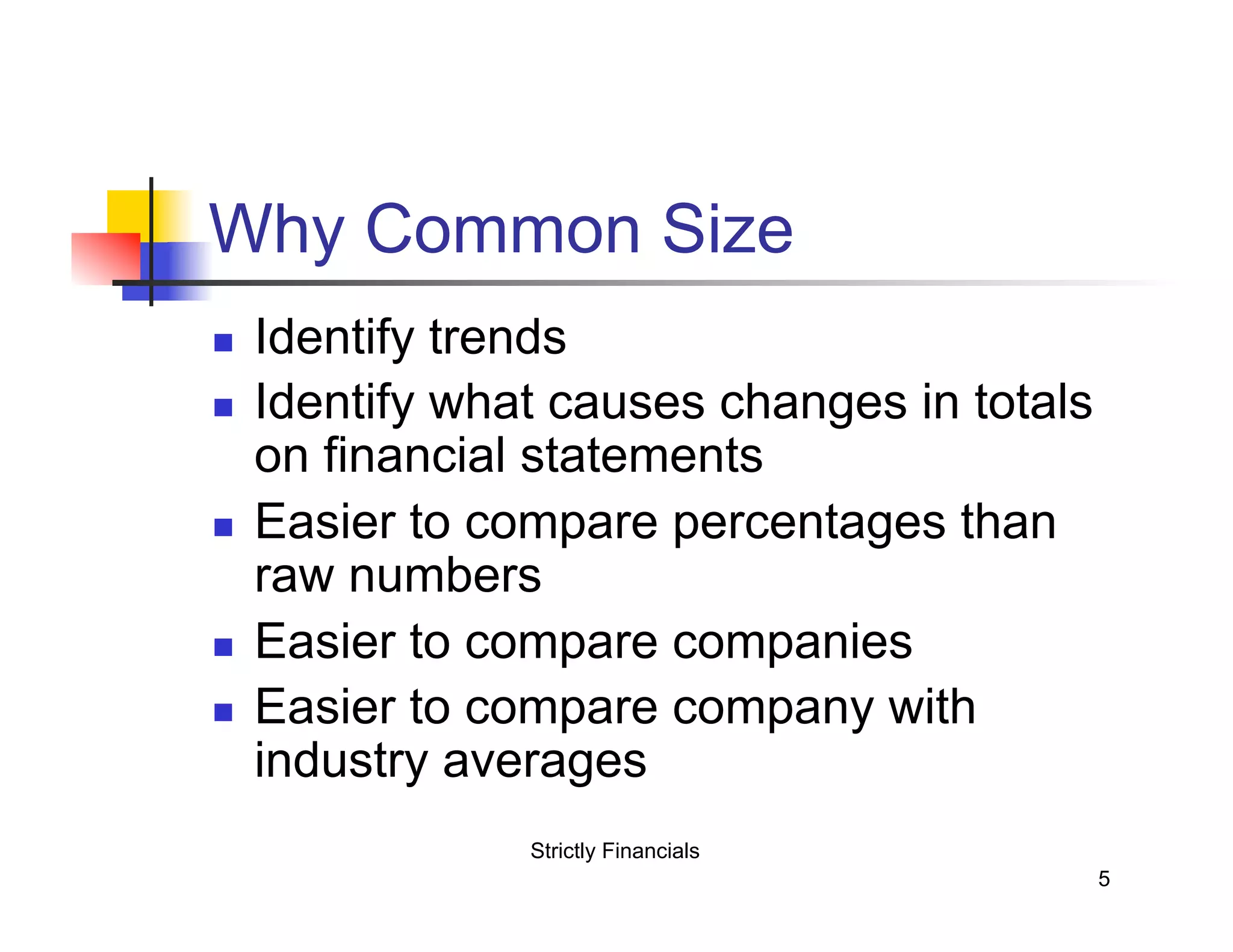

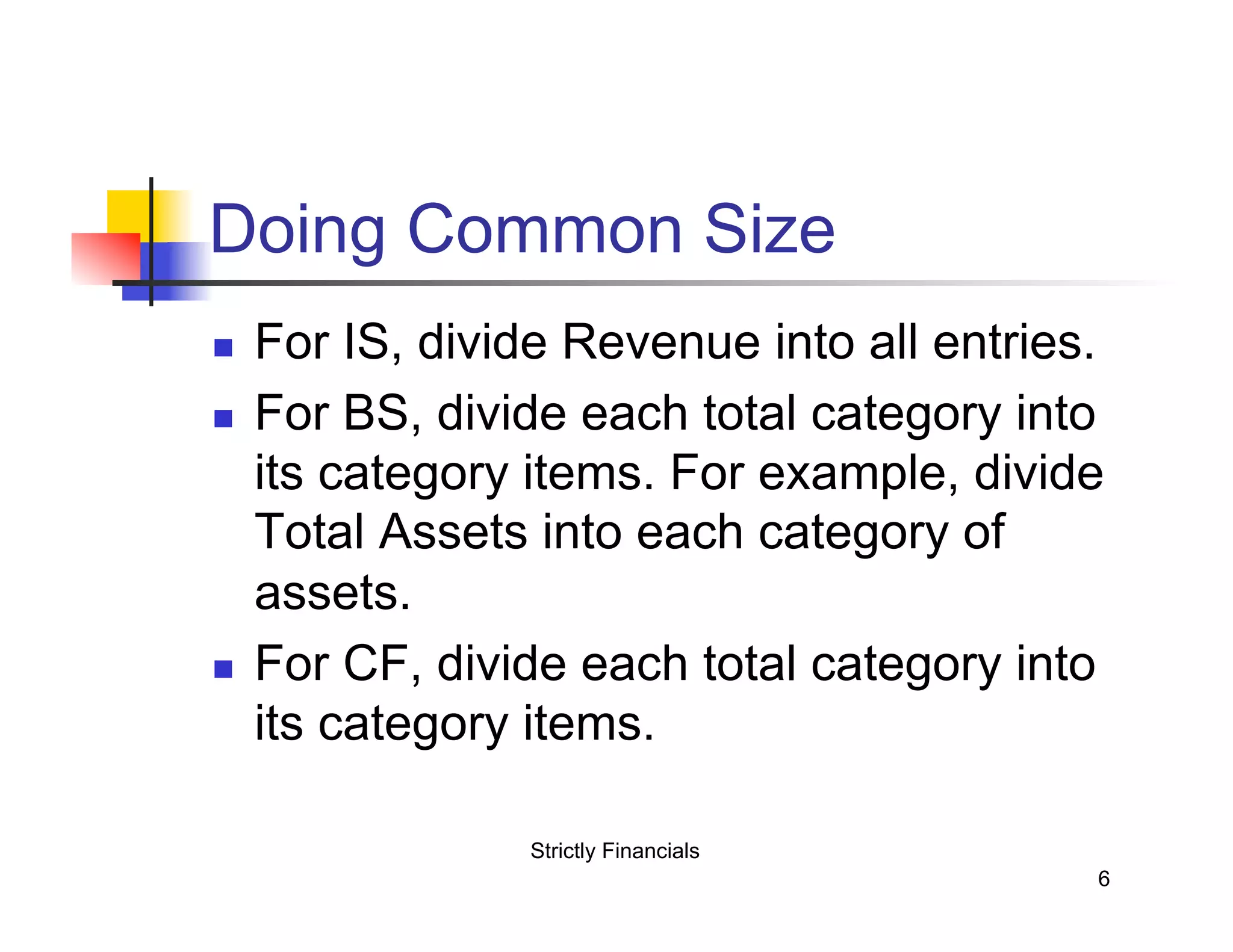

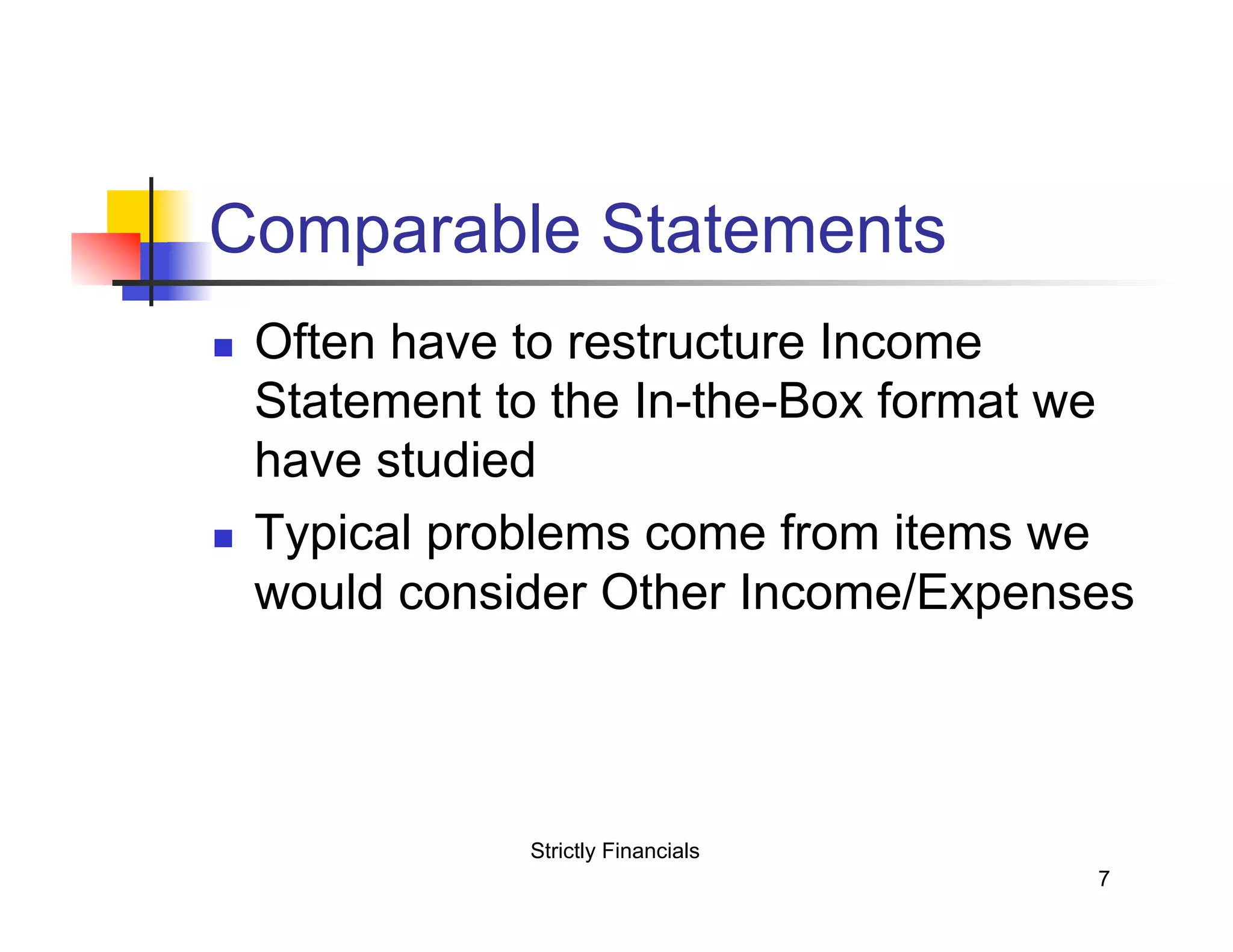

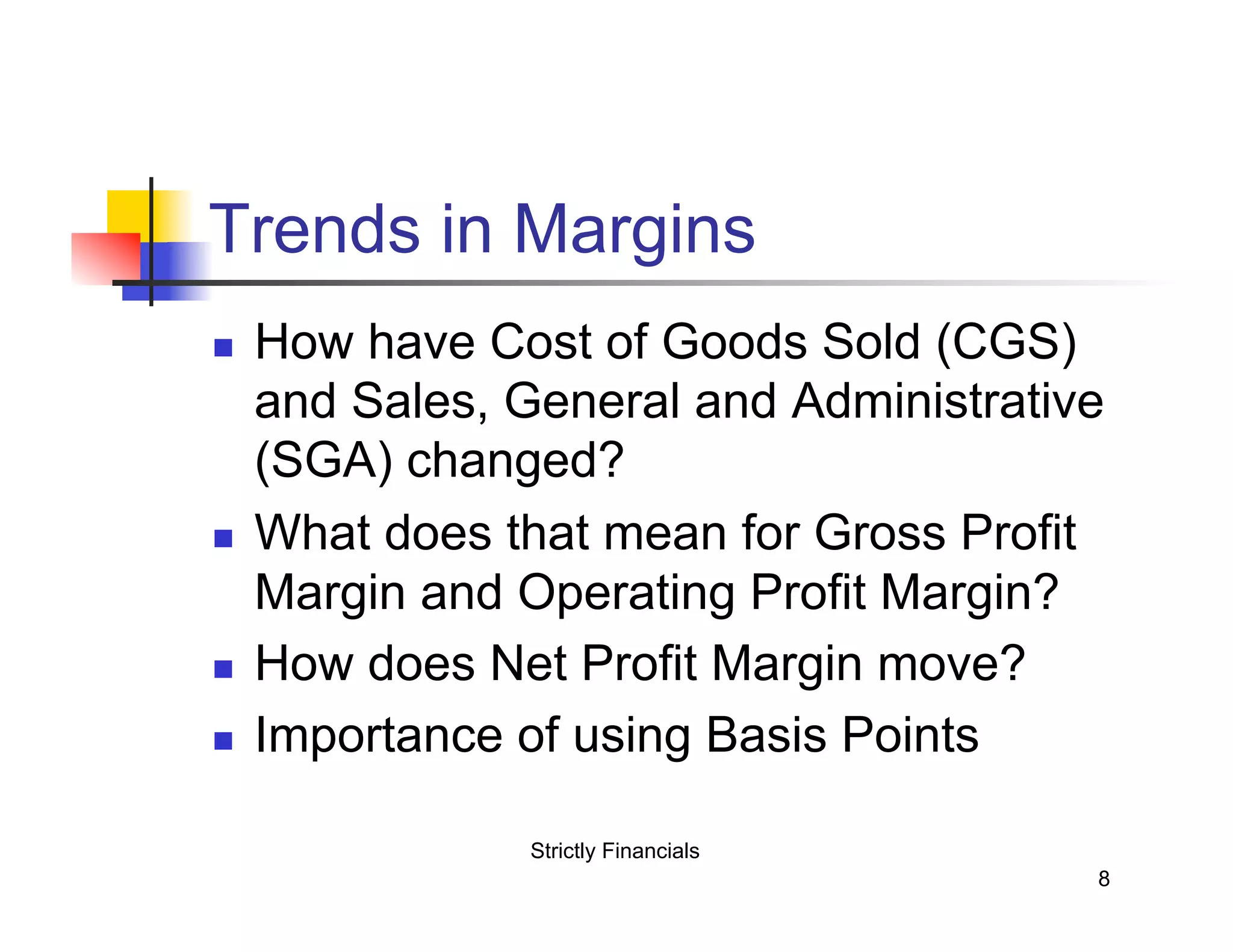

The document explains common size analysis, a technique that converts financial statement entries into percentages of revenue, facilitating trend identification and comparisons among companies and industry averages. It outlines methods for creating common size statements across income, balance sheets, and cash flow statements, emphasizing the importance of margins and financial ratios. The analysis aids in understanding a firm's performance by examining strengths, weaknesses, and strategic effectiveness.