Download as PDF, PPTX

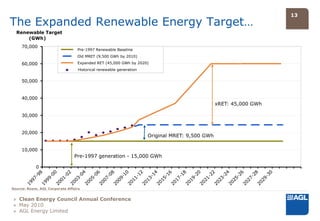

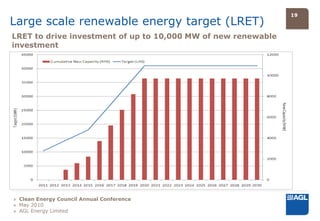

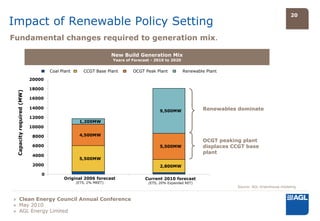

Michael Fraser, CEO of AGL Energy Limited, spoke at the Clean Energy Council Annual Conference in May 2010 about the importance of reforming Australia's Renewable Energy Target. He argued that passing legislation to reform the RET was urgent to avoid loss of jobs, investment, and confidence in energy policy. The reforms aimed to drive investment in renewable energy through mechanisms like the Small-Scale Renewable Energy Scheme and Large-Scale Renewable Energy Target. While the RET would contribute to slightly higher electricity prices, this impact would be minor compared to rises from network charges. Fraser concluded that with the reforms passed, billions could be invested in renewables and jobs.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)