This document provides an introduction to corporate finance concepts. It outlines different types of risk exposure, the topics that will be covered in the course, and what managerial finance entails. The course will focus on time value of money, risk and return, cost of capital, and business valuation. It defines key terms like the cash conversion cycle and discusses metrics like beta, covariance, and standard deviation that are used to measure risk. Formulas for present and future value, return, and the Capital Asset Pricing Model are also presented.

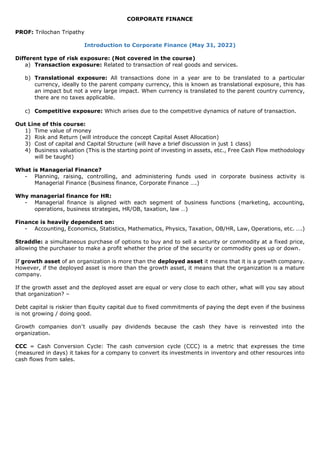

![TIME VALUE OF MONEY

Money has time value because if I invest money today in future it may give positive return if the interest

rate remains positive.

Inflation and rate of interest go hand in hand, if inflation is positive rate of interest will be high and vice-

versa.

Financial Values:

- Present value of Money: = PV = Future Value / [1+r]r

Future value of Money = FV = PV x [1+i]n

For the PV function to work in XL sheet, the PV must be the same, for the NPV function to work in XL sheet,

the PV must be different.

RISK & RETURN: A PRACTICE PERSPECTIVE (June 1, 2022)

While making an investment, we think of risk & return.

Risk – Return Tradeoff: Higher the risk, higher the return and vice-versa.

Beta Measure – Beta is a measure of a stock's volatility in relation to the overall market. By definition, the

market, such as the S&P 500 Index, has a beta of 1.0, and individual stocks are ranked according to how

much they deviate from the market. A stock that swings more than the market over time has a beta above

1.0. For example, a stock with a beta of 0.8 would be expected to return 80% as much as the overall

market. A stock with a beta of 1.2 would move 20% more than the overall market.

Co-Variance: Covariance measures the directional relationship between the returns on two assets. A

positive covariance means that asset returns move together while a negative covariance means they move

inversely.

Risk & Return Fundamentals:

Return:

- Loss or gain experienced from an investment over a period of time Rt = [Pt – Pt-1] / Pt-1 x 100 =

Return, this is called “Discrete Return”

- Holding Period Return: Dividend / Income + Discreet Return

- Dividend % + Discreet Return % = Holding Period Return %

- Capital Gain = Subtract your basis (what you paid) from the realized amount (how much you sold it

for) to determine the difference, and if you want a percentage value, multiply by 100

Price of stock today is 100 and tomorrow it has gone up 120

Pt = Today’s value of the stock

Pt-1 = Yesterday’s value of the stock

Risk:

- Chance of financial loss

- Variability of returns associated with a given asset

- The uncertainty of the returns associated with a given asset

- Standard deviation is a total risk measure

- Beta is a systematic risk measure

Measurement of Risk:

- Standard Deviation

- Variance

- Beta

- Covariance

- Correlation](https://image.slidesharecdn.com/classnotes-220717144331-8efddf35/85/Class-Notes-pdf-2-320.jpg)

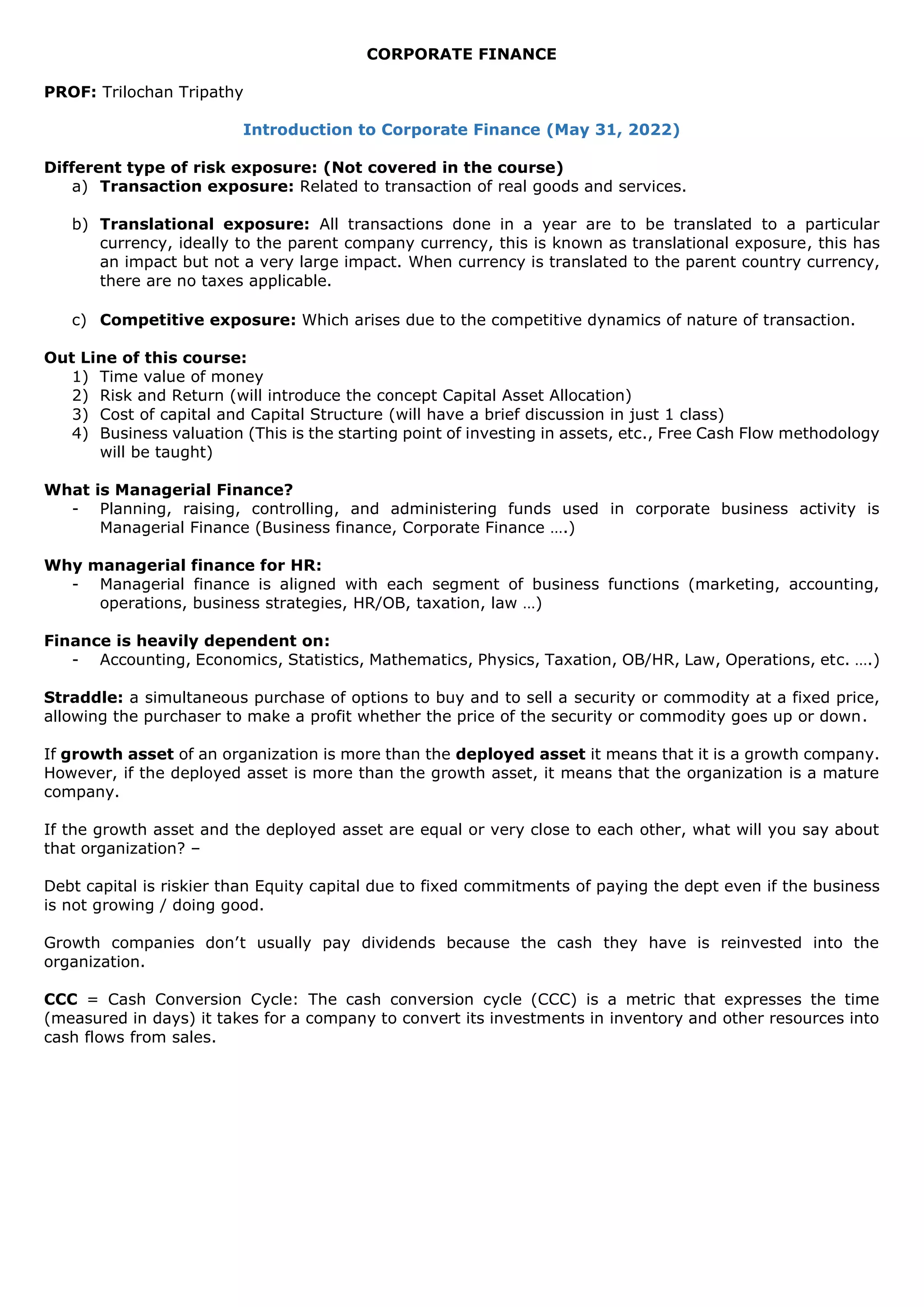

![Gold and Equity are inversely affected to each other. Whenever the market falls gold rises and vice-versa.

Gold and Equity have a negative correlation.

Annualizing Return

- From monthly return to annualized return:

- Annual gross return = [1+Rm]^12-1

- Rm here = monthly return

- Nominal return is the return computed before inflation, post computing inflation the return got is

known as Real / Net return

▪ Leverage Theory: The good news and bad news having the same impact will reduce the stock price

faster than increase it for good news

▪ Systematic Risk cannot be diversified – called as Market Risk, means imposed by the market

▪ Non-systematic Risk can be diversified – Risk taken at an individual / organizational level

▪ Total Risk can be measured by standard deviation

▪ Beta measures the market risk which is the Systematic Risk

CAPM Model (Capital Asset Pricing Model)

E(ri) = rf + [Beta i x (E(rm) – rf)]

- Rl = Alpha + Beta (Rm – Rf)

- Beta = Systematic Risk = Covariance (Rm,Ri) / Variance (Rm). Variance divided by another variance

will always be 1 – but for the MARKET only, for an individual security it will give some figure.

- Rm = Market Return (Also known as Market Average Return) = Rm, also known as Index Return

- Ri = Individual Return

- Rf = Risk free rate (there are no assets which are risk free), Treasury Bond Yield

- Difference between Rm and Rf is known as How much return the market is offering over and above

the risk, also known as Market Risk Premium

- Beta x Difference between Rm and Rf is known as How much return the market is offering over and

above the risk. = Market Risk associated return this is also known as Risk Premium associated with

that security.

- Square of Standard Deviation = Variance

The adjusted closing price amends a stock's closing price to reflect that stock's value after accounting

for any corporate actions. The closing price is the raw price, which is just the cash value of the last

transacted price before the market closes.](https://image.slidesharecdn.com/classnotes-220717144331-8efddf35/85/Class-Notes-pdf-3-320.jpg)