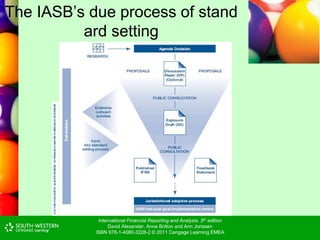

Chapter 3 of 'International Financial Reporting and Analysis' discusses the harmonization of accounting practices, focusing on the role of the EU and the IASB. It outlines the endorsement process of international accounting standards and the history of financial reporting regulation in Europe. The chapter highlights current developments, including IFRS for SMEs and the convergence project among key accounting bodies.