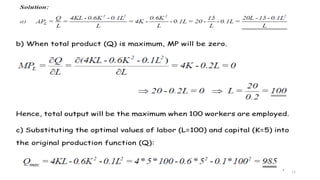

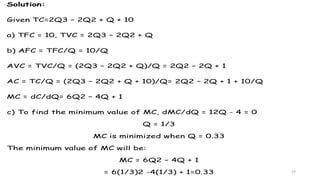

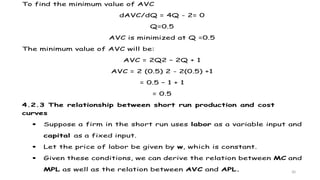

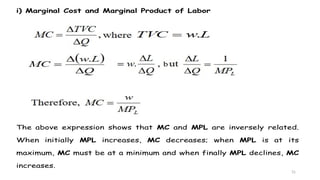

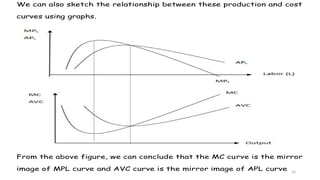

The document discusses the theory of production and costs, explaining the production process as transforming inputs into outputs and the relationships between fixed and variable inputs. It details the concepts of marginal product, average product, total product, and the stages of production, along with short-run cost functions including total, average, and marginal costs. Additionally, it highlights the relationships between production and cost curves, particularly the inverse correlations between marginal costs and marginal products of labor.