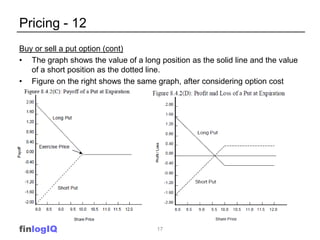

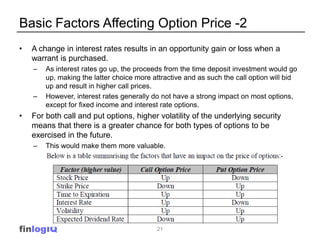

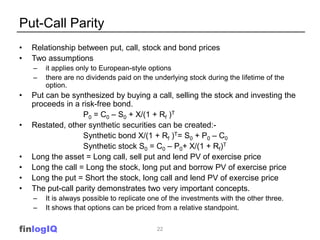

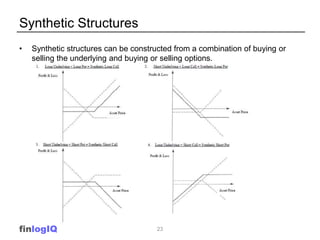

This document provides an overview of options, including definitions, concepts, pricing models, risks, and strategies. It defines options, outlines key terms like premium, strike price, and expiration. It explains pricing models including intrinsic value and factors that affect option prices like underlying price, volatility, and time to expiration. Put-call parity and how options can be used to synthesize other positions are also summarized.