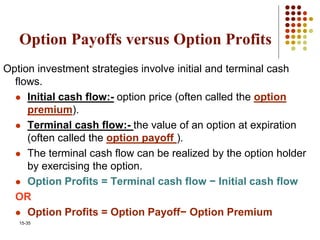

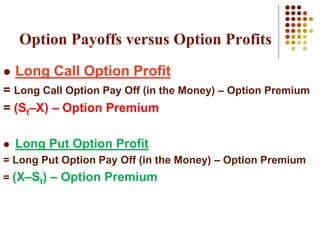

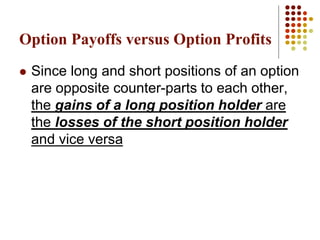

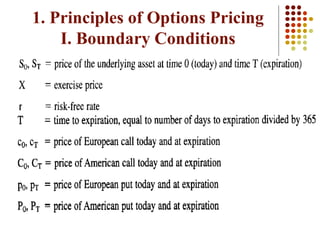

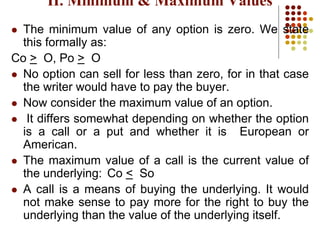

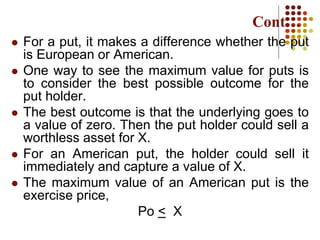

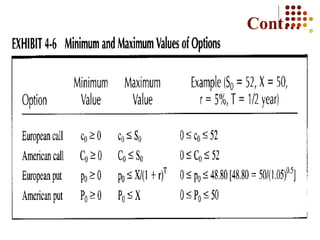

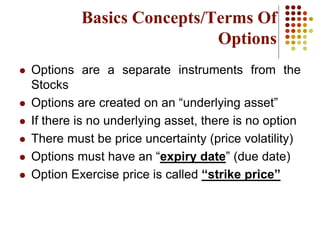

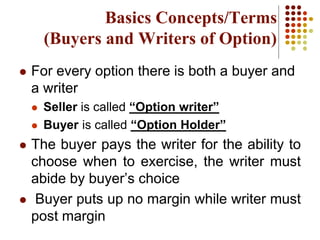

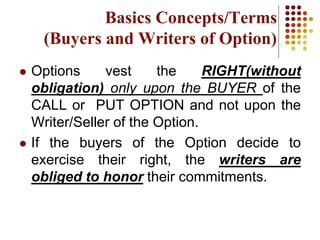

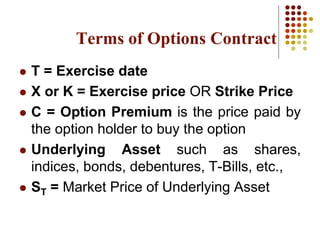

The document outlines key concepts related to options derivatives. It discusses:

1. Options provide the right to buy or sell an underlying asset at a fixed price, allowing investors to hedge risk bidirectionally unlike futures which only hedge in one direction.

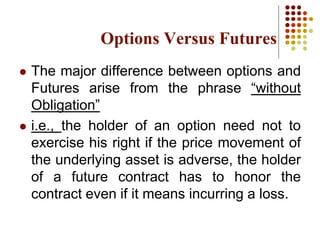

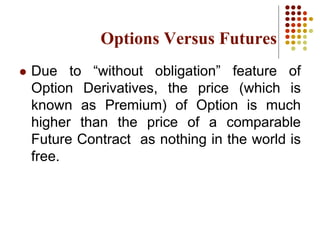

2. The major difference between options and futures is that options do not impose an obligation - the holder can choose not to exercise the right.

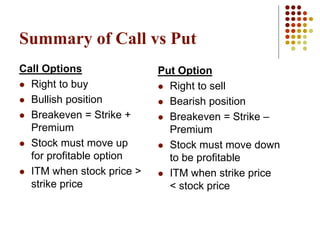

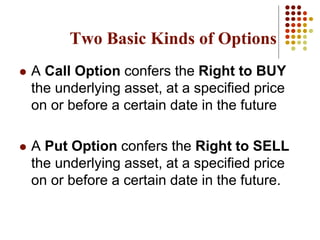

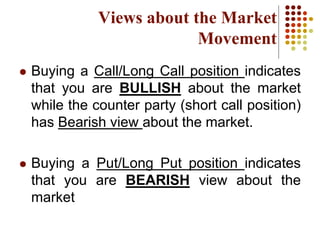

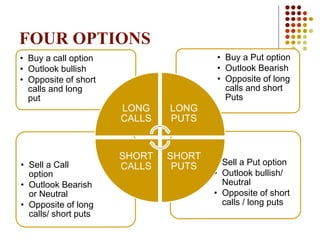

3. There are two main types of options - calls, which give the right to buy, and puts, which give the right to sell. Positions can be long, indicating a bullish outlook, or short, indicating a bearish outlook.

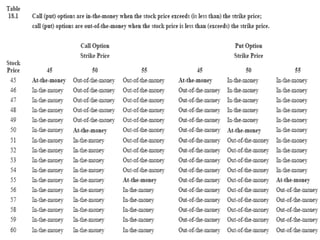

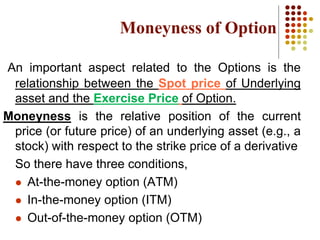

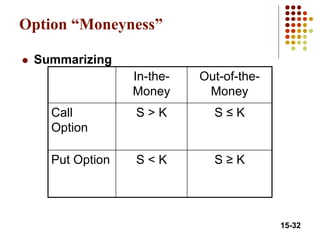

![ At The Money (ATM): An Option is an

ATM Option when strike price is same as

current spot price [X = ST], so the decision

to exercise becomes irrelevant.

In The Money (ITM): when two prices are

such that it is profitable for the Option

holder to exercise the option.

Out of The Money (OTM): when it is better

for the holder not to exercise the option.

Moneyness of Option](https://image.slidesharecdn.com/options-220718004944-72ae30c1/85/Options-pptx-30-320.jpg)

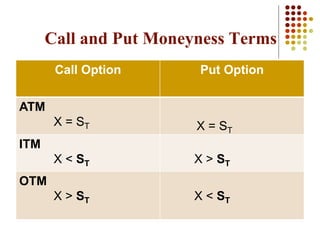

![Call Option Moneyness Terms

At The Money (ATM): when strike price is same as

current spot price [X = ST] and payoff from exercising

is zero

In The Money (ITM): A Call Option will be ITM when

strike price is below the current spot price [X < ST] and

the payoff from exercising is positive i.e., (St–X) > 0

Out of The Money (OTM): A Call Option will be OTM

when the strike price is above the current spot price

[X > ST] and the payoff from exercising is zero

i.e., (St–X) < 0 so no reason to exercise](https://image.slidesharecdn.com/options-220718004944-72ae30c1/85/Options-pptx-33-320.jpg)