CFP Board Conference Poster-Final-02-17

•

1 like•116 views

Poster from research study presented at February 2017 CFP Board Academic Research Colloquium for Financial Planning and Related Disciplines.

Recommended

Recommended

More Related Content

Similar to CFP Board Conference Poster-Final-02-17

Similar to CFP Board Conference Poster-Final-02-17 (20)

More from Barbara O'Neill

More from Barbara O'Neill (20)

Recently uploaded

Recently uploaded (20)

CFP Board Conference Poster-Final-02-17

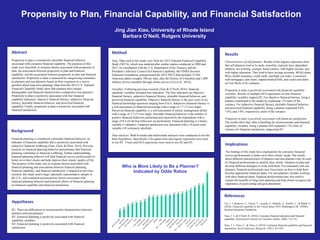

- 1. Jing Jian Xiao, University of Rhode Island Barbara O’Neill, Rutgers University Propensity to Plan, Financial Capability, and Financial Satisfaction Background Financial planning is considered a desirable financial behavior, an indicator of financial capability that is positively associated with subjective financial wellbeing (Xiao, Chen, & Chen, 2014). Previous research on financial planning behavior demonstrates that financial planning contributes to financial wellbeing. Further understanding financial planning behavior will help financial service professionals to better serve their clients and help improve their clients’ quality of life. The purpose of this study was to examine factors associated with financial planning and associations between financial planning, financial capability, and financial satisfaction. Compared to previous research, this study used a large, nationally representative sample in the U.S., and examined socioeconomic factors associated with financial planning behavior and potential effects of financial planning on financial capability and financial satisfaction. Abstract Propensity to plan is considered a desirable financial behavior associated with consumer financial capability. The purposes of this study were threefold: to examine factors associated with propensity to plan, the association between propensity to plan and financial capability, and the association between propensity to plan and financial satisfaction. Propensity to plan is measured by categorizing consumers as planners and non-planners based on their responses to a survey question about long-term planning. Data from the 2015 U.S. National Financial Capability Study show that planners have unique demographic and financial characteristics compared to non-planners. Propensity to plan is positively associated with four financial capability indicators: objective financial literacy, subjective financial literacy, desirable financial behavior, and perceived financial capability. Finally, propensity to plan is positively associated with financial satisfaction. Method Data. Data used in this study were from the 2015 National Financial Capability Study (NFCS), which was modeled after similar studies conducted in 2009 and 2012. In consultation with the U.S. Department of the Treasury and the President’s Advisory Council on Financial Capability, the FINRA Investor Education Foundation commissioned the 2015 NFCS that included 27,564 American adults (roughly 500 per state, plus the District of Columbia) and 1,000 military service members through online surveys (Lin et al., 2016). Variables. Following previous research (Xiao & O’Neill, 2016), financial capability variables included four indicators. The four indicators are objective financial literacy, subjective financial literacy, desirable financial behavior, and perceived financial capability. Objective financial literacy is the quiz score of six financial knowledge questions ranging from 0 to 6. Subjective financial literacy is a self-assessment of financial knowledge with a range of 1-7 (7=very high). Perceived financial capability is a self-assessment of money management ability with a range of 1-7 (7=very high). Desirable financial behavior is the number of positive financial behaviors performed and reported by the respondents with a range of 0-4 (4=all four behaviors are performed). Financial planning is a binary variable (1=planner). Financial satisfaction was measured with a 10-point scale variable (10=extremely satisfied). Data analyses. Both bivariate and multivariate analyses were conducted to test the three hypotheses. Specifically, Chi-square tests and logistic regression were used to test H1. T-tests and OLS regressions were used to test H2 and H3. Results Characteristics of self planners. Results of the logistic regression show that self planners tend to be male, nonwhite, married, have dependent children, are working, younger, home owners, with higher income, and with higher education. They tend to have savings accounts, 401(k) plans, IRAs, health insurance, credit cards, and high cost loans. Consumers with mortgages, auto loans, unpaid medical bills, and credit card debts are less likely to be a planner. Propensity to plan is positively associated with financial capability variables. Results of multiple OLS regressions on four financial capability variables support H2. For objective financial literacy, being a planner contributed to the model by explaining .2% more of the variance. For subjective financial literacy, desirable financial behavior, and perceived financial capability, being a planner explained 4.8%, 7.6%, and 3.0%, respectively, more of the variance. Propensity to plan is positively associated with financial satisfaction. The results show that, after controlling for socioeconomic and financial capability variables, being a planner still explained 1.2% more of variance for financial satisfaction, supporting H3. Implications The findings of this study have implications for consumer financial service professionals to better serve their clients’ needs. The results about different characteristics of planners and non-planners may be used by financial professionals to identify their clients’ intention to plan and develop different strategies to work with them. For consumers who are planners, financial professionals may focus more on how to help them develop appropriate financial plans. For non-planners, besides working with their financial plans, financial professionals may also need to explain the benefits of long-term planning and help clients recognize the importance of goal-setting and goal attainment. Hypotheses H1. There are differences in socioeconomic characteristics between planners and non-planners. H2. Financial planning is positively associated with financial capability variables. H3. Financial planning is positively associated with financial satisfaction. 0.38 0.45 0.64 0.72 0.77 0.81 0.89 1.08 1.09 1.10 1.13 1.16 1.17 1.22 1.26 1.26 1.36 1.46 1.58 1.69 1.73 2.33 Who is More Likely to Be a Planner? Indicated by Odds Ratios References Lin, J. T. Bumcrot, C., Ulicny, T., Lusardi, A., Mottola, G., Kieffer, C., & Walsh, G. (2016). Financial capability in the United States 2016. Washington, DC: FINRA Investor Education Foundation. Xiao, J. J., & O’Neill, B. (2016). Consumer financial education and financial capability. International Journal of Consumer Studies, 40(6), 712-721. Xiao, J. J., Chen, C., & Chen, F. (2014). Consumer financial capability and financial satisfaction. Social Indicators Research, 118(1), 415-432.