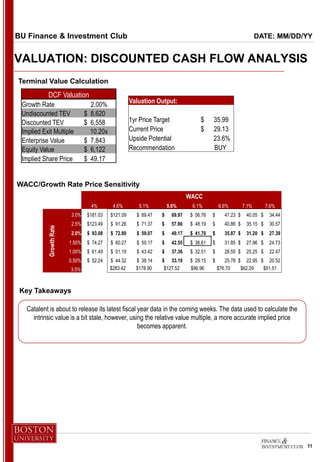

Catalent is the global leader in drug development and manufacturing. It has over 1,300 patents and is well-positioned to benefit from substantial industry growth of 6-10% annually through 2020. While pricing pressures could slow industry growth, Catalent's business model focusing on development, delivery, and supply solutions provides long-term stable revenues. The recommendation is to buy Catalent stock, which trades at $29.13 but has a target price of $35.99 based on discounted cash flow analysis.