This summary provides information about a property brochure for Riverside Quarter in 3 sentences:

The brochure provides details about Riverside Quarter, a development of shared ownership apartments located in Putney, London. It includes floor plans, specifications for the kitchens and bathrooms, and information about the local amenities like shops, restaurants, and transportation. The document advertises the exclusive collection of apartments and highlights features like the location along the River Thames.

[Online Business Case Competition 2020] Suncream TeamBich Nguyen

Business Case Study Competition is a nationwide online business case competition organized by Company Insider, patronized by The Trainee Club, attracted more than 300 participating teams.

Our team of 2 members has to make a deep analysis of the business situation and propose solutions to boost revenue & sales.

Looking forward to receiving your feedback.

E-contest 2020 is a citywide competition hosted by YEC Club, attracted more than 300 participating teams. This season provides the theme of trade marketing.

After 3 rounds, our team of 3 members has to propose a trade marketing plan for developing Oreo's sale channels to gain more market share.

Looking forward to receiving your feedback.

Obstacles:

• Turning customer data into usable insights.

• Effort of implementing new technology.

• Integrating with other platforms.

• Integrating channels, e.g., ecommerce, in store, marketplaces

• Store issues: competition, margin compression, store capacity

TrustRobin...app health education....https://youtu.be/57ghR94SYXM

[Online Business Case Competition 2020] Suncream TeamBich Nguyen

Business Case Study Competition is a nationwide online business case competition organized by Company Insider, patronized by The Trainee Club, attracted more than 300 participating teams.

Our team of 2 members has to make a deep analysis of the business situation and propose solutions to boost revenue & sales.

Looking forward to receiving your feedback.

E-contest 2020 is a citywide competition hosted by YEC Club, attracted more than 300 participating teams. This season provides the theme of trade marketing.

After 3 rounds, our team of 3 members has to propose a trade marketing plan for developing Oreo's sale channels to gain more market share.

Looking forward to receiving your feedback.

Obstacles:

• Turning customer data into usable insights.

• Effort of implementing new technology.

• Integrating with other platforms.

• Integrating channels, e.g., ecommerce, in store, marketplaces

• Store issues: competition, margin compression, store capacity

TrustRobin...app health education....https://youtu.be/57ghR94SYXM

Le magasin du futur - Keynote Zappos E-Commerce Paris 2013 par Dominique Piot...Petit Web

Qui ? Dominique Piotet, Pdg de Rebellion Lab et architecte du magasin du futur pour Zappos, qui ouvrira ses portes en janvier 2015 à Las Vegas.

Quoi ? Un keynote lors du salon E-commerce Paris 2013, qui donne un avant gout du premier magasin physique du leader américain de la vente de chaussures, filiale d'Amazon.

Estratégias de atribuição de mídia ON para OFF com visão única do cliente ger...E-Commerce Brasil

Benjamin Thompson - Head of Digital Transformation, Endeavour Drinks Group falou sobre Estratégias de atribuição de mídia ON para OFF com visão única do cliente gerando mais vendas durante o Fórum E-Commerce Brasil 2019.

Branding in Omni-Channel Environment: Fashion Industry of BangladeshAhsanul Kabir Palash

Omni channel marketing offers marketers and retailers a holistic approach to reaching consumers with a more integrated message, through any channel and at any point in their path to purchase.

Interaction with brands has become nonlinear and shaped by many interactions across several touch points. The interconnectivity between these touch points is called omni-channel.

Grocery online: experiências omnicanal integradas em varejo multi-formatoE-Commerce Brasil

Pedro Santos - Head de E-Commerce & Mobile, Supermercado Continente falou sobre Grocery online: experiências omnicanal integradas em varejo multi-formato durante o Fórum E-Commerce Brasil 2019.

10 Retailers Win 2014 Channel Innovation Awards

For the fourth year, Retail TouchPoints is proud to present the Channel Innovation Awards. This award program is designed to honor retailers who are achieving cross-channel success in today’s challenging retail environment.

This year’s 10 winners run the gamut of industry segments, from apparel and toys to wine and home improvement products. They are both U.S. and internationally based retail companies. Most of the winners are selling their products via both brick-and-mortar and e-Commerce web sites, in addition to mobile web sites and other channels.

The 2014 winners’ latest efforts are centered on improving the business through targeted channel strategies. Those strategies feature in-store mobile and digital technology innovations; social media efforts; personalization programs and more. All winners are successfully integrating the benefits of successful channel marketing and services to their customers, and delivering impressive results.

2014 Retail TouchPoints Channel Innovation Award Winners include:

Platinum winners:

-Stage Stores

-Clarks Footwear

Gold winners:

-bebe

-Build.com

Silver winners:

-Toys R Us Canada

-Kidrobot

-Sears

Bronze winners:

-B&H Photo

-Wine Enthusiast

-Country Club Prep

How to Design for an Omni-Channel Shopping ExperienceUserZoom

According to the IDC Retail Insights report, Omni-Channel shoppers will spend 15% to 30% more than Multi-Channel shoppers and they are more likely to be your brand’s influencers and Net Promoter advocates. It is now evident, that brands who make the customer experience omniscient, i.e. continues and universal, will lead the marketplace.

So how do you design for an Omni-Channel shopping experience? View a webinar on-demand with Sean Van Tyne, author of The Customer Experience Revolution, to learn how to craft a uniform experience across channels and touch points.

Twitter Hashtag: #uzwebinar

In this 60-min webinar on-demand you will learn:

-What Omni-Channels are

-Who Omni-Channel Shoppers are

-What a journey map and a service blueprint is

-How to create an Omni-Channel

OmniChannel Retail Best Practices for Brands and RetailersStephany Gochuico

This research work provides retailers practical insights, real-world strategies, solutions, and recommendations to improve customer experience, increase business results and maintain competitive advantage in the retail industry.

CONTENTS

1. Why and what is OmniChannel Retail?

2. What are the consumer behaviours?

3. Who are the Best-in-Class OmniChannel Retailers?

4. What are the OmniChannel Challenges in France?

5. What are the OmniChannel Best Practices?

6. How to deal with Showroomers?

7. How to be successful in implementing OmniChannel?

Bricks + Mobile 2011 - Terrified Retailers Take ControlRemodista

The mobile in-store revolution: If Amazon is taking my customers what I can do about it? What’s working, what’s just hype, and what is coming?

•In this session we will cover how the mobile phone is being used today by consumers to aid their in-store purchasing process.

•We will discuss the in-store research renegades who are using bar code scanners and google search to find better deals while they’re in the store. Is all this gaming and check-in technology hype or valuable?

•How is mobile NFC technology going to impact the checkout process?

•Where does mCommerce fit into the store environment? Is anyone going to scan a QR code while standing in a store

Back The Future: A Retail Transformation StrategyCapgemini

Julian Burnett Chief Information Officer - House of Fraser

The U.K. has given rise to some of the most powerful, long-lived and envied retail brands. But many must now strive to survive against the formidable pressure of market entrants – without the drag of aged stores, processes and systems.

Through technology enabled change and a refocusing upon the fundamentals of great retailing, the strong continue to hold their own and drive a differentiated proposition, leveraging insight to create unique experiences for customers. As House of Fraser embarks upon its own retail transformation, Julian Burnett, CIO and Capgemini alumni, reflects upon the priorities, challenges and approaches of the House of

Fraser Business Technology team and the central role that enterprise architecture plays in helping achieve business goals.

Go-to browsing channels vary

*(38%) start on Amazon

* (35%) search engines

* (21%) brand or retaile web sites

* (6%) e-Commerce marketplaces, such as eBay and Etsy

Le magasin du futur - Keynote Zappos E-Commerce Paris 2013 par Dominique Piot...Petit Web

Qui ? Dominique Piotet, Pdg de Rebellion Lab et architecte du magasin du futur pour Zappos, qui ouvrira ses portes en janvier 2015 à Las Vegas.

Quoi ? Un keynote lors du salon E-commerce Paris 2013, qui donne un avant gout du premier magasin physique du leader américain de la vente de chaussures, filiale d'Amazon.

Estratégias de atribuição de mídia ON para OFF com visão única do cliente ger...E-Commerce Brasil

Benjamin Thompson - Head of Digital Transformation, Endeavour Drinks Group falou sobre Estratégias de atribuição de mídia ON para OFF com visão única do cliente gerando mais vendas durante o Fórum E-Commerce Brasil 2019.

Branding in Omni-Channel Environment: Fashion Industry of BangladeshAhsanul Kabir Palash

Omni channel marketing offers marketers and retailers a holistic approach to reaching consumers with a more integrated message, through any channel and at any point in their path to purchase.

Interaction with brands has become nonlinear and shaped by many interactions across several touch points. The interconnectivity between these touch points is called omni-channel.

Grocery online: experiências omnicanal integradas em varejo multi-formatoE-Commerce Brasil

Pedro Santos - Head de E-Commerce & Mobile, Supermercado Continente falou sobre Grocery online: experiências omnicanal integradas em varejo multi-formato durante o Fórum E-Commerce Brasil 2019.

10 Retailers Win 2014 Channel Innovation Awards

For the fourth year, Retail TouchPoints is proud to present the Channel Innovation Awards. This award program is designed to honor retailers who are achieving cross-channel success in today’s challenging retail environment.

This year’s 10 winners run the gamut of industry segments, from apparel and toys to wine and home improvement products. They are both U.S. and internationally based retail companies. Most of the winners are selling their products via both brick-and-mortar and e-Commerce web sites, in addition to mobile web sites and other channels.

The 2014 winners’ latest efforts are centered on improving the business through targeted channel strategies. Those strategies feature in-store mobile and digital technology innovations; social media efforts; personalization programs and more. All winners are successfully integrating the benefits of successful channel marketing and services to their customers, and delivering impressive results.

2014 Retail TouchPoints Channel Innovation Award Winners include:

Platinum winners:

-Stage Stores

-Clarks Footwear

Gold winners:

-bebe

-Build.com

Silver winners:

-Toys R Us Canada

-Kidrobot

-Sears

Bronze winners:

-B&H Photo

-Wine Enthusiast

-Country Club Prep

How to Design for an Omni-Channel Shopping ExperienceUserZoom

According to the IDC Retail Insights report, Omni-Channel shoppers will spend 15% to 30% more than Multi-Channel shoppers and they are more likely to be your brand’s influencers and Net Promoter advocates. It is now evident, that brands who make the customer experience omniscient, i.e. continues and universal, will lead the marketplace.

So how do you design for an Omni-Channel shopping experience? View a webinar on-demand with Sean Van Tyne, author of The Customer Experience Revolution, to learn how to craft a uniform experience across channels and touch points.

Twitter Hashtag: #uzwebinar

In this 60-min webinar on-demand you will learn:

-What Omni-Channels are

-Who Omni-Channel Shoppers are

-What a journey map and a service blueprint is

-How to create an Omni-Channel

OmniChannel Retail Best Practices for Brands and RetailersStephany Gochuico

This research work provides retailers practical insights, real-world strategies, solutions, and recommendations to improve customer experience, increase business results and maintain competitive advantage in the retail industry.

CONTENTS

1. Why and what is OmniChannel Retail?

2. What are the consumer behaviours?

3. Who are the Best-in-Class OmniChannel Retailers?

4. What are the OmniChannel Challenges in France?

5. What are the OmniChannel Best Practices?

6. How to deal with Showroomers?

7. How to be successful in implementing OmniChannel?

Bricks + Mobile 2011 - Terrified Retailers Take ControlRemodista

The mobile in-store revolution: If Amazon is taking my customers what I can do about it? What’s working, what’s just hype, and what is coming?

•In this session we will cover how the mobile phone is being used today by consumers to aid their in-store purchasing process.

•We will discuss the in-store research renegades who are using bar code scanners and google search to find better deals while they’re in the store. Is all this gaming and check-in technology hype or valuable?

•How is mobile NFC technology going to impact the checkout process?

•Where does mCommerce fit into the store environment? Is anyone going to scan a QR code while standing in a store

Back The Future: A Retail Transformation StrategyCapgemini

Julian Burnett Chief Information Officer - House of Fraser

The U.K. has given rise to some of the most powerful, long-lived and envied retail brands. But many must now strive to survive against the formidable pressure of market entrants – without the drag of aged stores, processes and systems.

Through technology enabled change and a refocusing upon the fundamentals of great retailing, the strong continue to hold their own and drive a differentiated proposition, leveraging insight to create unique experiences for customers. As House of Fraser embarks upon its own retail transformation, Julian Burnett, CIO and Capgemini alumni, reflects upon the priorities, challenges and approaches of the House of

Fraser Business Technology team and the central role that enterprise architecture plays in helping achieve business goals.

Go-to browsing channels vary

*(38%) start on Amazon

* (35%) search engines

* (21%) brand or retaile web sites

* (6%) e-Commerce marketplaces, such as eBay and Etsy

The need for quality environments

and fixture programs has never been greater for the

outlet channel. Meeting the customers’ expectations

relies on understanding the influencers and trends in this

evolving market. Here are four trends in the evolution

of the outlet retail environment, as well as, six areas of

focus that will drive success for branded retail in the

outlet channel

The short and long term challenges with top-line growth during a crisis demand different ways of working and thinking from the everyday.

In this short webinar we will look at the levers that might help rapidly adapt your retail business to changing market situations – with insights and inspiration from actual retail cases – and we will discuss possible initiatives that can grow your retail top line.

Creating loyal omnichannel customers is critical. Retailers who embrace the customer-centric trend and build better shopping experiences will leap ahead of the competition.

Building a blended customer experience isn't easy. Need some help getting started? Check out our latest in retail trend research.

Informes PwC - Encuesta Total Retail GlobalPwC España

El informe "Hacia un modelo de Total Retail", elaborado por PwC, analiza las expectativas y hábitos de consumo del comprador online, a partir de 15.000 entrevistas a compradores digitales de todo el mundo, y las implicaciones para las compañías del sector de distribución y consumo en los próximos años.

Informe de PwC sobre las expectativas y hábitos de consumo del comprador onlineMaría Bretón Gallego

El informe Hacia un modelo de ‘Total Retail’, elaborado por PwC, analiza las expectativas y hábitos de consumo del comprador online, a partir de 15.000 entrevistas a compradores digitales de todo el mundo, y las implicaciones para las compañías del sector de distribución y consumo en los próximos años.

Internet y las nuevas tecnologías han multiplicado la influencia del consumidor, pero, ¿qué les están pidiendo a las marcas? Las nuevas expectativas y hábitos del consumidor digital tendrán importantes implicaciones para las compañías del sector en los próximos años

Adaptation helps retailers and property owners meet changing consumer needs and expectations. An article in the Property Institute's Property Professional Magazine by First Retail Group's Managing Director, Chris Wilkinson.

2021 Omnichannel Guide: A Four-Pillar Approach to Holistic Commerce Successrun_frictionless

An omnichannel approach isn’t just another way of saying that you sell on multiple marketplaces. It’s about delivering a consistent brand experience that transcends specific channels to meet customers where they are and build a personal connection, as well as optimizing your business for the future through channel diversification and comprehensive integration of your data and systems.

https://runfrictionless.com/b2b-white-paper-service/

Some important notes about retail industry such as:

Strategic Levers of Retailing,

Functions Performed by Retailers,

Types of Retailers,

Customers Perception and Buying Behavior,

Merchandise Management,

Issues with Merchandise Management.

This report highlights the increasingly competitive nature

of the retail market, identifying changing consumer

behaviour as a key driver behind this. Consumers today

own much more ‘stuff’ than previous generations, making

it more difficult to persuade them to purchase additional

products. Consumers are also time-pressured, so convenience

and speed has taken priority.

All these factors, combined with supply side considerations - more intense focus on price, a deflationary retail environment and even greater choice - means retail growth will be much harder to achieve over the next ten years. For this reason, it is vital that retailers secure customer loyalty.

Understanding consumers’ behaviour, wants and needs is essential to build this loyalty. This isn’t just about knowing what customers want to buy, but truly understanding how and where they want to buy, their motivations and what they expect from their overall shopping experience.

This also means that retailers need to re-evaluate how to reach customers and reappraise traditional marketing techniques – many of which are still relevant, but are less impactful and influential in today’s environment. This deeper understanding will ultimately help retailers secure loyalty in the era of the unfaithful consumer.

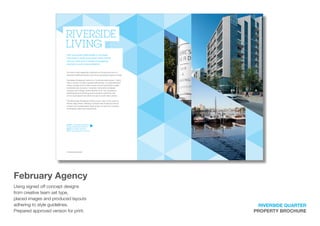

1. Riverside quarter

property brochure

February Agency

Using signed off concept designs

from creative team set type,

placed images and produced layouts

adhering to style guidelines.

Prepared approved version for print.

Above: Computer generated

image of Riverside Quarter

Below: The River Thames

Left: Duke’s Head Pub, Putney

4 Riverside Quarter

The local area offers shops of all types

and sizes to meet your every need; rarely

will you find such a range of shopping

choices in such close proximity.

For day-to-day essentials, Hudson’s on the ground floor of

adjacent Milliners House is the most convenient place to shop.

Southside Shopping Centre is a 14 minute walk away (1.2km),

with a choice of major supermarket stores, a comprehensive

array of shops and a wide choice of food and drink outlets.

Southside also houses a 14-screen Cineworld multiplex

cinema and a Virgin Active Health Club. The complex is

developing and growing and is poised to become one

of the most significant retail venues in south west London.

The Exchange Shopping Centre is just 1.4km to the west on

Putney High Street, offering a unique mix of famous brand

names and independent retail stores, as well as a number

of relaxing cafes and restaurants.

RIVERSIDE

LIVING

2. Riverside quarter

property brochure

SPECIFICATION

Kitchen

apartments except Types 101 & 102)

Appliances

extract hood

combination (separate fridge and freezer

to Type 209)

Bathroom

(1 Eastfields Avenue)

Eastfields Avenue)

Hallway and Living Areas

kitchen, living room and hallway

heating with zone controls

Internal doors

and bedrooms*

and bedrooms

battery backup

General

all apartments

common areas

Parking

select apartments

at Riverside Quarter will not be eligible for a

Wandsworth Council car parking permit

*Purchaser’s responsibility to obtain decoding

equipment and subscription services.

Caveat at bottom:

The above specification is a general guide

only and may be subject to change. Please

contact a member of the Sales Team for

specific details.

FLOORPLANS

Riverside Quarter 15

An exclusive collection of Shared Ownership apartments at Riverside Quarter.

3. Property brochure

CBRE

Produced spreads for a property

magazine called Shopfront aimed at the retail

sector. Sourced imagery, created charts and

took direction from the marketing manager with

regards to styling. Fast layout skills were essential

due to a tight deadline.

21

1Notatallimportant

4Veryimportant

2

N

ot ver

y

im

portant

3

Fairly important

Price

Cleanliness

Convenience

Security

Parking

Free parking

Range of retailers

Information points/signage

Specific retailers

Range of services

Being covered

Presence of independent shops

Presence of a hypermarket/supermarket

Environmental business practices

Size of shops

Good place to meet friends/spend time

Presence of a department store

Presence of one or two large fashion shops

Extensive range of catering facilities

Coffee shops

Free Wifi

Good quality restaurants

Entertainment facilities

Hosting of events

CBRE | SHOPFRONT 2014/15CBRE | SHOPFRONT 2014/1520

AS SHOPPING CENTRES STRIVE TO DEVELOP THEIR

‘EXPERIENTIAL’ OFFER, ALBERT HOOGLAND, EMEA HEAD

OF SHOPPING CENTRE MANAGEMENT, ARGUES THAT

EFFECTIVELY MANAGING ‘BASICS’ LIKE CLEANLINESS AND

SAFETY IS STILL CRUCIAL TO SUCCESS.

WE ASKED: “HOW IMPORTANT ARE THE FOLLOWING

FACTORS IN A NON-FOOD SHOPPING TRIP?”

THEY SAID:

Managing a shopping centre is a balancing act – I’m sure some

would call it a high wire act. There’s a need to balance the varied

and often competing needs of tenants, as well as the different

tastes and requirements of various consumer groups. More

recently, shopping centre managers have also felt the need to

strike a balance between getting the basics right and investing

in ways to differentiate their schemes from both rival shopping

destinations and the lure of the internet.

In doing so, is there a risk that attention paid to the basics is

pushed aside in the headlong charge to provide new and better

experiences? Any schemes tempted to let this happen would do

well to read through a copy of CBRE’s survey – How Consumers

Shop 2014 – which questioned 21,000 consumers across 21

countries and encompasses three million data points.

When these consumers were asked what motivates them to

visit a shopping centre, it was the basics – price, convenience,

cleanliness and security – that came out top; with the softer, more

experiential elements further down the list.

This doesn’t mean I’m suggesting that atmosphere, experience

and entertainment should be ignored: once again it comes back

to balance. In my view, if you can get your basics perfectly in

order, in the most efficient and cost-effective way, you will have

more resources (both time and financial) available to take your

scheme to the next level in terms of creating consumer experience

and connecting with your retailers in a more empathetic and

cooperative way.

The challenge is how to go about doing that, and this starts with

understanding the basics. For example, what is clean? More

specifically, how do my customers and my retailers perceive clean?

It’s not rocket science to understand that customers’ perceptions

on cleanliness in a prime, luxury-oriented mall are different from

ALBERT HOOGLAND

t: +31 30 634 80 35

e: albert.hoogland@cbre.com

CREATE YOUR

EXPERIENCE…

BUT DON’T

FORGET THE BASICS

Note: Excludes ‘don’t know’

Source: How Consumers Shop 2014, CBRE

those of a neighbourhood centre in a small town. There are plenty

of points in between, though, and only by understanding where

your scheme belongs on this spectrum and working closely with

your cleaning contractor to fulfil these requirements economically

will you be able to ensure you’ve got the balance right. The same

goes for other elements such as security.

AN ANALYTICAL APPROACH TO SHOPPING

CENTRE MANAGEMENT

With a portfolio of shopping centres under management that now

numbers more than 230 schemes in 21 countries, CBRE’s EMEA

Shopping Centre Management team has plenty of experience in

striking the right balance to get the best out of an asset.

More recently, we’ve begun to back that experience with a

more analytical approach to the task. We’ve partnered with

two specialist consultancies, Cyber and Locatus, to create the

Shopping Centre Quality Monitor, a unique product for assessing

and comparing the quality of individual shopping centres.

Quality is assessed on the basis of three key elements: Basics,

Service and Experience. Each has 65 measurable and trackable

components, providing a much more detailed picture of the

strengths and weaknesses of a scheme than has hitherto been

possible.

Working with our partners we deployed this methodology among

a group of some 100 shopping centres in the Netherlands two

years ago. We are now about to repeat the exercise, so we can

track the progress made since that first assessment. We are also

piloting the Quality Monitor in selected Central and Eastern

European countries, with a view to eventually extending it across

our entire European portfolio.

IMPROVING THE LANDLORD/TENANT

RELATIONSHIP IS KEY

It’s one thing to know where you need to improve, quite another

to actually achieve those improvements. And here a lot of the

challenge comes back to retailer relationships. Although things

have improved in recent years, the landlord/tenant relationship

can still be too adversarial at times. As managers, we must strive

ever harder to convince retail groups about the mutual benefits

that can be derived from working more closely together. It’s easy

to say ‘but they just won’t listen’ – we must ask ourselves what we

can change in our own attitudes to get the retailers’ attention.

In this omnichannel world the big brands don’t care what journey

the consumer takes to get to them – via physical store, their

laptop or their smartphone – but they do want that revenue. When

cooperation between the shopping centre and retailer is good,

the centre can play a role in that omnichannel customer journey,

perhaps by installing click and collect points with adjoining

changing rooms, for example?

This is something the shopping centre can offer which the high

street retail environment can’t – an advantage we should be

careful not to neglect.

4. Property brochure

22 23CBRE | SHOPFRONT 2014/15 CBRE | SHOPFRONT 2014/15

CONFIDENCE IS RETURNING TO THE SPANISH RETAIL

MARKET AS INVESTORS SCRAMBLE FOR THE BEST ASSETS

AMID RECORD TRANSACTION VOLUMES.

ALEX BARBANY

t: +34 93 444 7711

e: alex.barbany@cbre.com

After three years of painful recession, the Spanish economy

has finally returned to growth in 2014, with a similarly positive

performance expected to continue into 2015. A feeling that

there’s now light at the end of the tunnel has truly taken hold,

putting smiles back on the faces of many.

Even stubbornly high (above 20%) unemployment levels have

failed to dampen consumer confidence, which is back to its

pre-crisis levels after increasing substantially during the past 12

months. This is having its biggest effect in the wealthiest regions,

SPAIN

where the money didn’t really disappear but spending was held

back by a lack of confidence. Elsewhere, though, it may still take

some time before the macroeconomic improvements filter through

to the retail market.

As a result, we are seeing an increasing polarisation of trading

performance between the dominant regional shopping centres,

where sales are growing by double-digits, and the rest, where

sales are flat or falling.

INVESTORS FLOCK TO SPAIN

The most significant retail story of the year is undoubtedly the

flood of investment capital into the Spanish shopping centre

segment. At the time of going to press investment volumes had

already reached €1.7 billion and by the end of 2014 that figure

could well have climbed to between €2 and €2.5 billion. For

comparison, the previous record volume was €2 billion achieved

in 2007, on the eve of the financial crisis.

Among the principal buyers are the newly-created Socimis

(equivalent to REITS) such as MERLIN and Lar, together with fund

managers, notably CBRE Global Investors and TIAA Henderson,

and private equity investors including Oaktree and Incus Capital

among others.

Their enthusiasm for the best assets has seen yield compression

of around 125-150 bps during the last 12 months, with prime

shopping centres now being traded at net initial yields of around

5.5%-5.75%, while prime high street properties yield around

4.5%. Looking ahead, we predict that values of secondary high

street assets will rise during the next couple of years, as investors

switch their attention to this part of the market due to the total lack

of investment opportunities on the prime streets.

The surging investment market is also having a major knock-on

effect in the development area, in two distinct ways. The first is an

upturn in refurbishments and extensions, as new owners free up

funds to asset manage their new properties, many of which have

been starved of investment in recent years due to the financial

constraints in the market. The second is a new wave of greenfield

developments by the retail specialists, who have been crowded

out of the investment market by the pure financial players.

Notable pipeline schemes that underline this trend include

Carrefour Property’s 60,000 sq m S’Estada in Palma de Mallorca,

General de Galerias Comerciales’ c.90,000 sq m Parque

Nevada in Granada, plus four projects by Intu in Malaga, Vigo,

Valencia and Mallorca, each around 200,000 sq m

Unibail-Rodamco, meanwhile, has two major extension/

refurbishments projects in Barcelona.

RETAILERS ALSO FLOCKING IN

Spain never really went off the radars of the international retailers,

but 2014 has seen a significant upturn in new brands arriving.

This is particularly apparent in the aspirational/luxury segment,

where sales are underpinned by the millions of tourists who flock

to Madrid and Barcelona. New arrivals here include Longchamp,

Canali, Brunello Cucinelli, Jo Malone, Dior, Twin-Set and Coach.

In another significant move, the Saudi Arabian franchise specialist

Fawaz AlHokair has entered the Spanish market via a takeover of

the domestic group Blanco. As well as promising to revitalise this

brand, it seems likely that Fawaz AlHokair will bring some of the

many other brands it controls to the market in the coming years.

Established retailers, particularly in the fashion segment, are

seeking to rationalise their estates into fewer numbers of larger

stores. Zara, for example is now looking for a minimum of

2,500 sq m, Mango is after flagships of around 2,000 sq m,

while H&M seeks 3,000 sq m units in shopping centres and

anything up to 7,000 sq m on high streets, the latter necessitating

multiple floors. These groups are using their additional space to

show off other lines within their portfolios, while also rolling out

numerous sub-brands.

Such moves are again serving to consolidate performance

around the best performing street and mall environments, while

some poorer performing malls have been forced to close, further

boosting the market share of the ‘winners’.

2014 HAS

SEEN A

SIGNIFICANT

UPTURN IN

NEW BRANDS

ARRIVING

KEY TRENDS IDENTIFIED:

Investment capital flooding into Spain and fighting for the

best assets; consumer confidence on the rise again; retail

specialists planning a wave of new schemes

5. Property brochure

38 39CBRE | SHOPFRONT 2014/15 CBRE | SHOPFRONT 2014/15

REBECCA PEARCE, EMEA HEAD OF SUSTAINABILITY AT CBRE, INVESTIGATES THE

POTENTIAL FOR ENVIRONMENTAL SUSTAINABILITY TO BE HARD-WIRED INTO THE

RETAIL LEASING PROCESS.

Whatever one’s views on the ultimate impacts of climate change,

nobody can deny that our planet is using up its natural resources –

and generating landfill waste – at far too rapid a rate. The dilemma

at both governmental and corporate levels has been around working

out the practical steps that can be taken to slow down this effect and

make our lives more sustainable.

In retail real estate the solution could well come in the form of the

green lease. This is an initiative that has been around for a while

now, forming part of a growing movement to get landlords and

tenants working closer together to reap the environmental and

financial benefits from more sustainable behaviour.

So what is a green lease? It can take several forms, some involving

binding obligations, others implemented on a voluntary basis. In

the former case, green commitments are hard-wired into the lease

agreement itself, with potential penalties for non-compliance. In

the latter case, the commitments are often grouped into an annex

to the lease or incorporated into a non-binding memorandum of

understanding.

Typical elements within a green lease are targets around energy and

water consumption, also generation of waste to landfill. Perhaps

most significant, however, are the requirements for information

sharing in these energy/waste matters, in order to set workable

benchmarks that can drive improved performance. This requires

quite a leap of faith given the traditionally stand-offish nature of

the landlord/tenant relationship, where information has often been

closely guarded.

Some landlords are already grasping the nettle, however. Redevco

is one of the pioneers in this regard: for the past six years it has

been collecting energy/water consumption data from some 1,100

tenants, which it makes public in the form of the Redevco Retailer

Sustainability Benchmark. This is an online scorecard tool that

any retailer can consult in order gain a better insight into their

environmental performance versus their peers.

In Asia, the green lease has become a reality in several markets,

notably Singapore and Malaysia. The developer making much

of the running is Lend Lease, which has rolled out green leases

in Singapore for the 313@somerset mall which it manages, and

also at its Jem mixed use scheme, which includes an 818,000 sq ft

shopping mall. The Lend Lease green lease encourages retailers

to make use of highly efficient lighting systems, adopt recycling

strategies and reduce overall tenancy waste.

DO TENANTS HOLD THE GREEN KEYS?

While landlords appear to be making the running with green

leases, in many ways it’s the tenants who hold the key to the

concept’s ultimate success. This works in two ways: accepting green

lease clauses during the lease negotiation process; also taking a

partnership approach to energy-saving investments.

As anyone who has taken part in a lease negotiation will know,

achieving the former is not an easy task, particularly when it comes

to the legal process. Easing this bottleneck is the aim behind a new

campaign by the International Council of Shopping Centres, which

is asking the chief executives of landlords, property managers and

tenants to put their names to a sustainability declaration, with a view

that this top-level endorsement can be used to punch through legal

and other barriers.

So far a host of high profile names in the property industry have

signed up. They include Redevco, Unibail-Rodamco, ECE, M&G

Real Estate, TIAA Henderson Real Estate, BANEASA Developments

SRL, Land Securities, Immochan and CBRE. At the time of going to

press ICSC was reaching out to retailers also.

The second issue, around co-funding investment in green initiatives,

is naturally a thorny topic. The industry has long suffered from the

so-called split incentive dilemma, whereby investments made by

landlords in areas such as energy efficiency are reflected in cheaper

service charges for tenants but do not contribute to the landlord’s

bottom line until the next rent negotiation, if at all.

With this in mind, the announcement last year by

Marks & Spencer that it was collaborating with the UK’s Better

Buildings Partnership on green clauses via memoranda of

understanding, could prove telling.

Speaking at the time of the announcement, Clem Constantine,

M&S’ then Director of Property, commented: “Currently it can

be difficult for landlords and tenants to work together when it

comes to a building’s environmental performance, particularly

for older leases. There’s often no real structure for measurement,

incentives or sharing of goals. Green leasing changes this

situation as it provides the framework within which both can

work together. And both will benefit, a store with a reduced

environmental impact and lower costs is more marketable for

landlords and more cost effective for tenants to occupy – a

genuine win, win.”

Such moves towards greater collaboration can only be beneficial

to the prospects for green leases. In many markets this forms the

last real stumbling block, since the logical arguments for saving

money through energy conservation have long since been won.

It feels as though we are on the cusp of broader green lease

adoption; it’s up to everyone within the retail real estate sector

to turn this promise into reality.

REBECCA PEARCE

t: +44 20 3257 6232

e: rebecca.pearce@cbre.com

6. EFT Energy Annual Report

Latitude

Using style guides and concept designs

from creative team at Latitude set type

and produced layouts adhering to corporate

guidelines. Prepared approved version

for print.

9. Property brochure

CBRE

Using CBRE brand guidelines produced

a brochure with content supplied from the

marketing team. Created graphs, charts and set

copy to a baseline grid. Accessed their image

library and chose appropriate photography.

UKDEVELOPMENTFUNDING-ISITAVAILBLE?

10 11

UKDEVELOPMENTFUNDING-ISITAVAILBLE?

REGIONAL FOCUS: ‘ A TALE OF TWO CITIES ’, EXEMPLARS OF THE TRENDS IN DEVELOPMENT FUNDING.

DIAGRAM A: DEVELOPMENT FUNDING EVOLUTION

New structured finance models

A. Gap funding

Equity

20% to 30%

Mezzanine

15% to 25%

Senior Debt

Development finance

40% to 55%

B. Highly structured

Mezzanine 10% to 20%

Preferred Equity 10% to 20%

Grant funding 10% to 20%

Equity 5% to 15%

Senior Debt

Development finance

40% to 55%

Equity

10% to 30%

Old Model

Senior Debt

50% to 70% for speculative

90% + for fully-let

STRUCTURED FINANCE:

BRIDGING THE GAP

LONDON: BENEFITING FROM AVAILABILITY

OF FUNDING

MANCHESTER: REGIONAL TEMPLATE FOR

THE FUTURE

Continues to dominate development funding

allocations.

Availability of funding is matching improving economic

strength and property growth.

Decent schemes with strong sponsors have access to

the most varied and cost-effective funding sources.

Pre-let schemes preferred, but flagship speculative

developments are possible.

Residential development is especially attractive:

continued upward pressure on house prices and

constrained supply.

Undergoing rejuvenation, where traditional lenders, new

funds and alternative capital providers are emerging to

support landmark schemes.

Scheme viability and structured finance solutions are key.

Innovative funding schemes are available (e.g. the North

West Evergreen Fund).

Highly supportive council and local authorities.

This revitalisation is anticipated to emanate across other

regions, which are showing similar early signs

of stimulation.

EVOLUTION TOWARDS

STRUCTURED FINANCE

SOLUTIONS

Diagram A demonstrates how the old model of significant

leverage coupled with equity has become unviable.

We are witnessing an evolution into more detailed

structured financings, consisting of various components,

becoming more common. Previous innovations would

have typically been led by the banks, but the onus is now

on the developers and their advisors to be creative if their

schemes are to be realised.

Prohibitively expensive funding is often as problematic

as an outright lack of finance as it jeopardises scheme

viability. As a solution, tiered capital structures can be

delicately assembled that carefully balance the various

costs or return hurdles of each type of finance to achieve

an overall blended rate that is feasible for the developer

and attractive to funders.

CBRE has witnessed regional schemes that have utilised

multiple combinations of senior debt, junior debt,

preferred equity and grant funding. In such situations,

these structures are often the developer’s only choice,

but can work very efficiently.

Grant funding derived from European and local

government bodies, such as the Homes and Communities

Agency and European Regional Development Fund, has

become an elusive yet crucial component of the funding

package for developers, especially outside London and

the South East. Where such grants can be secured, the

developer effectively bridges the gap between debt and

equity with little or no return hurdle, meaning more free

cash to service the other finance components.

Grant funding has become an

elusive yet crucial component of

the funding package

10. Property brochure

UKDEVELOPMENTFUNDING-ISITAVAILBLE?

4 5

UKDEVELOPMENTFUNDING-ISITAVAILBLE?

Equity and debt have been scarce for development, but

rare pockets of funding are available for those who know

where to look and are prepared to be creative.

Banks have significantly reduced their loan book exposure

to development to pre-2007 levels, but are expected

to eventually stabilise at lower levels, establishing new

market norms (see Chart 1).

This can be considered as a new rebased equilibrium

where development debt constitutes an integral, but more

limited part of lending. Debt funds and new entrants are

expected to partially supplement these allocations, but

total availability is still expected to remain compressed.

Development is still a feature of traditional lenders’

origination, but commercial development accounts for

just 5% of new business (see Chart 2). Geographically,

London and the South-East dominate funding, but the

situation is slowly improving in the regions where lending

appetite is selectively returning for certain schemes.

Speculative developments typically struggle to secure

bank finance, unless strong banking relationships exist

or if the schemes are in the most attractive locations.

Alternative funders can be considered, but pricing and

leverage may be higher. Where debt cannot be sourced,

developers may resort to initially funding on an equity-

only basis, possibly with a third-party providing the capital

where the developer supplies the land and its skill. Whilst

this can be expensive, it can sometimes be the only option

available and the developer may hope to refinance with

traditional debt once pre-lettings are achieved during the

development phase.CHART 1: BANK LOAD BOOK ALLOCATIONS TO DEVELOPMENT FINANCE

£bn

£50.0

£45.0

£40.0

£35.0

£30.0

£25.0

£20.0

£15.0

£10.0

£5.0

£0.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013Est

Residential development (banks)

Fully pre-let commercial (banks)

Speculative development (banks)

CHART 2: TRADITIONAL LENDERS’ ALLOCATION OF NEW LENDING IN 2012

Source: DeMontford and CBRE

Investment

Commercial Development

Residential Development

Source: DeMontford

IS DEVELOPMENT

FUNDING AVAILABLE?

Banks have significantly reduced

exposure to development to

pre-2007 levels

Commercial development

accounts for just 5% of

new business

11. KIER group graduate brochure

33 Recruitment advertising

Using style guides and concept designs

from creative team at 33 set type and

produced layouts adhering to corporate

guidelines. Prepared approved version

for print.

INSITEALookintoCAREERSAT KIER

Should you need to contact us, please write to:

Recruitment and Training Administrator

The Training and Development Department

Kier Group

Tempsford Hall

Sandy

Bedfordshire

SG19 2BD

United Kingdom

Tel: 01767 640111

Fax: 01767 641729

When you’ve got everything you need at your fingertips, all that’s left to

do is make the right choice. We’re here to help at every stage. You can

find even more information on our website www.kier.co.uk/careers and

contact us at any time if you have a question.

Once you’ve made your decision, what next? Well, our selection process

consists of two stages. Initially we hold interviews at universities,

careers events and our offices during the year. Our second stage

interviews are conducted at our head office in the spring, consisting of

a series of interviews and group activities to assess how well you’ll fit

in and give you a chance to find out some more about us. After this, we

make our offers.

We look forward to hearing from you.

Visit www.kier.co.uk/careersto find out everything

you need to know about how, when and where to apply.

Withinyour

sights

12. KIER group graduate brochure

5kier.co.uk

many opportunities for the best of starts

Kier Group provides a complete range of construction services across

a diverse range of sectors, giving graduates the opportunity to work on

a broad range of projects. You could find yourself working on projects in

a variety of sectors, including health, education, commercial, industrial,

government, defence, pharmaceutical and retail – working in partnership

with consultants, designers and sub contractors.

our graduate training schemes

At Kier, we give you everything you need to develop your career,

right from the word go. Our graduate and management development

programmes will ensure that you attain the skills necessary to reach

senior management positions within the Group as soon as you are able.

These comprehensive programmes include on-the-job training,

mentoring, project-based learning and numerous training courses.

They are accredited by all of the main industry institutions, including

CIOB, ICE and RICS.

WHAT’s

involved?

construction management

The best construction management graduates join us to work towards

senior management. You’ll gain crucial technical expertise working on

site, carrying out site surveys and planning, and you’ll also spend time

in the office to gain a rounded picture of the industry in roles such as

estimating and surveying. We’ll offer you at least six days off-the-job

training every year and encourage you to seek membership of the

Chartered Institute of Building (CIOB) www.ciob.org.uk, and assign you

an assessor as your CIOB mentor.

civil engineering

We operate an approved registered training scheme leading to

membership of the Institution of Civil Engineers (ICE) www.ice.org.uk.

For those with a qualifying degree, election to corporate membership of

the Institution (MICE) as a chartered engineer is possible. We’ll

encourage you to seek membership as early as possible and support

your development throughout. You will gain experience in solving

complex engineering problems, designing ‘turnkey’ projects and

planning major contracts. Your development will be supported by your

supervising civil engineer, who will be assigned to you as a mentor.

quantity surveying

This is an ideal opportunity for graduates with a commercial bias who

can demonstrate a sound practical approach and wish to develop their

career with a contractor. You’ll work under the direct control of a senior

quantity surveyor, making a real contribution to Kier’s profitability from

the start. We’ll encourage you to become a corporate member of the

Royal Institution of Chartered Surveyors (RICS) www.rics.org.uk. You’ll

work initially from a regional office or on a major contract, measuring

on site or from drawings and preparing bills of quantities. Later you will

gain experience in other aspects of site quantity surveying.

other opportunities

We are also looking for professionals to join from other disciplines,

where you will find the challenges just as appealing. Training is tailored

to the needs of your professional body, with a mentor to oversee your

progress. These disciplines include: accountancy; architectural

technology; building services engineering; general management;

business development/marketing; facilities management; housing; IT;

land buying; surveying and planning. Visit www.kier.co.uk/careers to

find out more about all our graduate opportunities.