Download to read offline

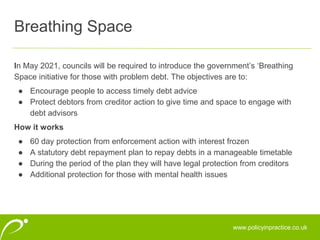

The document discusses the 'Breathing Space' initiative aimed at helping individuals with problem debt in the UK by providing a 60-day protection period from creditor action and encouraging access to professional debt advice. It highlights the detrimental impact of debt collection practices on vulnerable populations and emphasizes the need for more flexible and compassionate debt management policies among local authorities. Additionally, it reviews findings from research on council tax collection practices, the effectiveness of early interventions, and proposes recommendations for improving support for households facing financial difficulties.