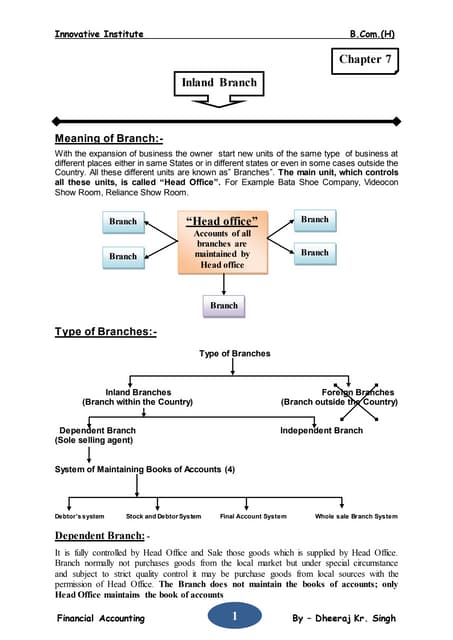

Branch accounting is a double-entry bookkeeping method used by businesses to manage separate accounts for each branch, enhancing transparency and financial analysis. It involves maintaining individual balance sheets and profit and loss statements for branches while consolidating them at the head office. Although it provides valuable insights into branch performance and cash flow, it can also lead to higher costs and potential mismanagement due to the required infrastructure.

![Introduction to Banking Instruments @@@ [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/introductiontobankinginstrumentsautosaved-251224005412-0855ddf1-thumbnail.jpg?width=640&height=640&fit=bounds)