BRANCH ACCOUNTING

• B.Com– Accountancy

• An In-depth and Conceptual Study

• Prepared for Classroom Presentation

2.

INTRODUCTION

• In modernbusiness organisations, expansion is achieved through opening

branches.

• Branch accounting is the system that enables the head office to record, control and

evaluate the performance of these branches.

3.

MEANING OF BRANCH

•A branch is a unit of a business located at a place different from the head office.

• It performs business activities such as sales, customer service and collection of

money on behalf of the head office.

4.

DEFINITION OF BRANCHACCOUNTING

• Branch accounting refers to the accounting system under which the head office

maintains records of branch transactions in order to ascertain the profit or loss of

each branch separately.

5.

OBJECTIVES OF BRANCHACCOUNTING

• • To ascertain profit or loss of each branch

• • To exercise effective control over branch activities

• • To evaluate branch performance

• • To prevent frauds and errors

• • To assist management in decision-making

6.

NEED FOR BRANCHACCOUNTING

• As business expands geographically, direct supervision becomes difficult.

• Branch accounting ensures decentralised operations with centralised financial

control.

7.

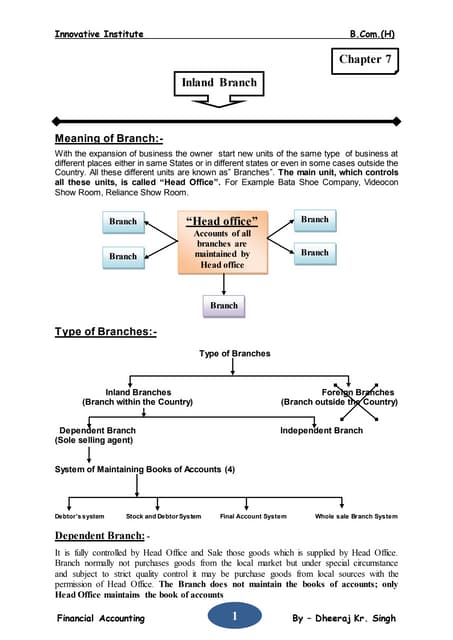

TYPES OF BRANCHES

•On the basis of accounting treatment, branches are classified into:

• 1. Dependent Branch

• 2. Independent Branch

8.

DEPENDENT BRANCH

• Adependent branch does not maintain its own books of accounts.

• All accounting records are maintained by the head office.

9.

FEATURES OF DEPENDENTBRANCH

• • No separate books of accounts

• • Goods supplied by head office

• • Expenses paid by head office

• • Cash collected is remitted to head office

10.

SYSTEMS FOR DEPENDENTBRANCH

• • Debtors System

• • Stock and Debtors System

• These systems help in ascertaining branch profit accurately.

11.

DEBTORS SYSTEM

• Usedwhen:

• • Branch sells goods only on credit

• • Branch does not maintain stock records

• Profit is ascertained through Branch Account.

12.

STOCK & DEBTORSSYSTEM

• Used when the branch maintains stock.

• Separate accounts are prepared for stock, debtors and expenses to ensure strict

control.

13.

GOODS SENT TOBRANCH

• Goods may be sent by head office:

• • At cost price

• • At invoice price (cost + profit margin)

14.

INVOICE PRICE

• Invoiceprice includes profit margin.

• It helps the head office to control stock and identify losses or pilferage.

15.

STOCK RESERVE

• Whengoods are invoiced above cost, closing stock contains unrealised profit.

• Stock reserve is created to show true profit.

16.

INDEPENDENT BRANCH

• Anindependent branch maintains its own books of accounts.

• It operates almost like a separate business unit.

17.

FEATURES OF INDEPENDENTBRANCH

• • Maintains separate books

• • Can purchase goods independently

• • Prepares its own final accounts

18.

ADVANTAGES OF BRANCHACCOUNTING

• • Better control over operations

• • Performance evaluation

• • Improved efficiency

• • Helpful in decision-making

19.

CONCLUSION

• Branch accountingis an essential tool for growing businesses.

• It ensures effective control, transparency and accurate measurement of branch

performance.