Downloaded 32 times

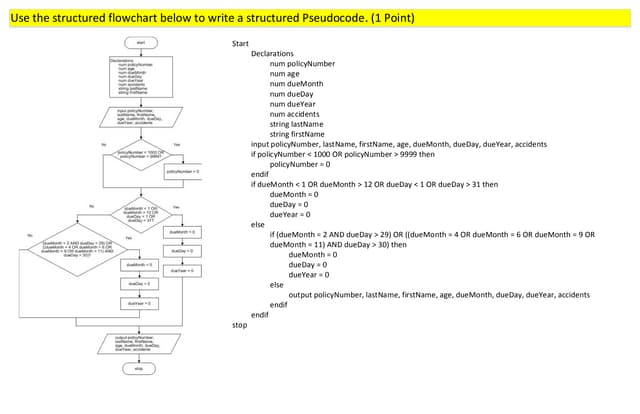

![How Much Does the Price ChangeThe amount the asset increases or decreases each time period can be shown to be an exponential function of “” , the risk measure or variance of the price movements of the asset, “r” the risk free interest rate, the life (“T”) of the option and the pricing periods (“m”) until exercise “u” is the % increase each period “d” is the % decrease each periodu = EXP[(r- 2/2)*(T/m) + (2(T/m))1/2]d = EXP[(r- 2/2)*(T/m) - (2(T/m))1/2]](https://image.slidesharecdn.com/binomialtree-12497541048736-phpapp01/85/Binomial-Tree-Option-Pricing-Theory-3-320.jpg)

This document describes the binomial tree method for pricing options. It explains how to construct a binomial tree based on the asset price, risk-free rate, and volatility. The value of the option is then solved for by working backwards through the tree. An example is provided where the asset price can move up 40% or down 29% at each time step. Working back from the expiration date, the number of asset units to purchase and amount to borrow is calculated to replicate the option payoff. Arbitrage ensures the option price equals this replicating portfolio value.