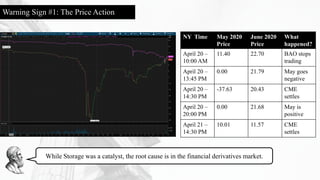

1) The document analyzes the extreme price drop in the May 2020 WTI oil futures contract in mid-April 2020, where the price went negative for the first time.

2) It suggests the root cause was a lack of liquidity as big financial players had exited before expiry due to risk policies, leaving retail investors and a gap without real buyers or sellers.

3) It raises concerns that some Chinese retail oil contracts may have been designed in a way that allowed the banks to retroactively force close positions if prices moved against clients, potentially profiting from the move.