Download as PDF, PPTX

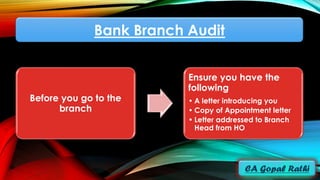

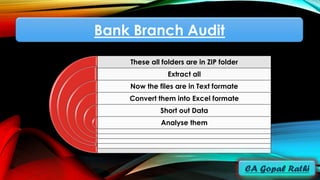

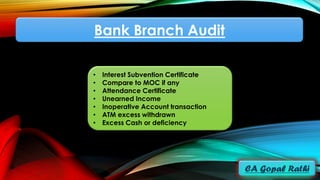

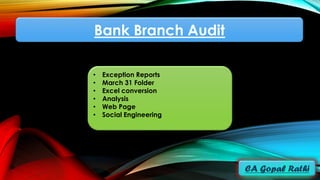

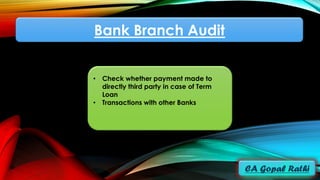

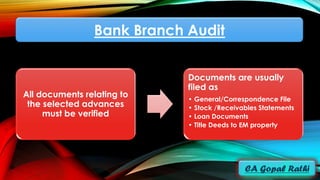

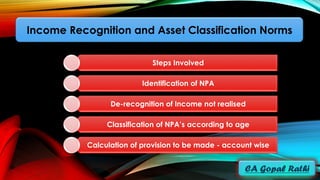

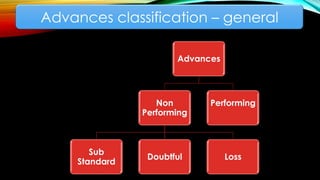

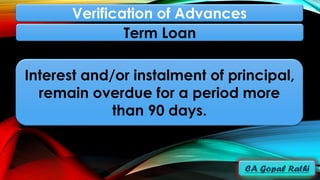

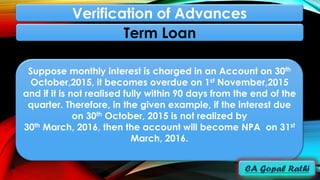

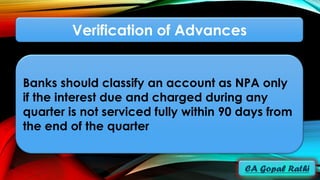

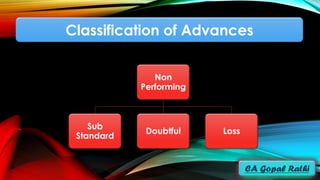

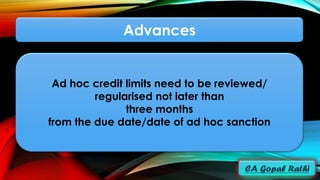

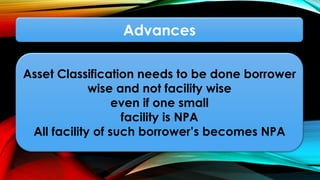

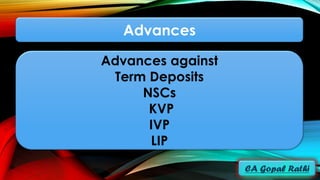

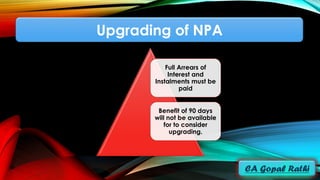

The document outlines a comprehensive audit procedure for bank branch audits, detailing the necessary documents to be collected and analyzed, including various financial reports and exception reports. It emphasizes the importance of verifying advances at different stages and classifying them according to their performance status based on specific criteria. Additionally, it provides insights into provisioning norms for different types of assets and the classification of non-performing assets (NPAs).