Download to read offline

![@@WestcourtConslt westcourt.com.au

Beginning of the end – Proactive tax

[ Tips and Tricks for a pain free EOFY]](https://image.slidesharecdn.com/backtothefutureseminar2017-170525015349/85/Back-to-the-future-seminar-2017-Family-Business-Accountants-Westcourt-1-320.jpg)

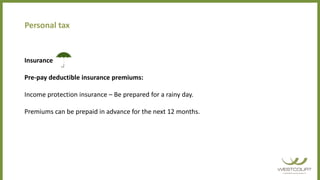

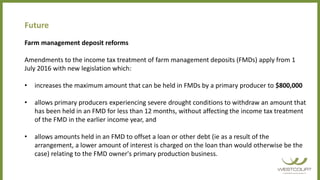

![AGES CONCESSIONAL [PREV. NON-CONCESSIONAL

UNDEDUCTED] [UNDEDUCTED]

Under age 49 $30,000 $180,000 OR

$540,000 Bring forward

option

50-64 $35,000 $180,000 OR

$540,000 Bring forward

option

65 and over $35,000 $180,000

No bring forward option

Superannuation Limits – Current (up to 30 June 2017)

Future](https://image.slidesharecdn.com/backtothefutureseminar2017-170525015349/85/Back-to-the-future-seminar-2017-Family-Business-Accountants-Westcourt-27-320.jpg)

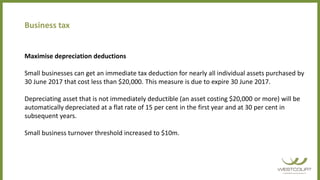

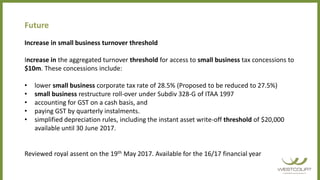

![$100,000

[from 1 July 2017}

AGES CONCESSIONAL [PREV. NON-CONCESSIONAL

UNDEDUCTED] [UNDEDUCTED]

Up to 74 $25,000 [from 1 July 2017]

Rolling 5 year cap

75 and over Compulsory super Not eligible to make

guarantee only contributions.

Future

Superannuation Limits – Future (from 1 July 2017)](https://image.slidesharecdn.com/backtothefutureseminar2017-170525015349/85/Back-to-the-future-seminar-2017-Family-Business-Accountants-Westcourt-28-320.jpg)

The document provides tips and strategies for individuals and businesses to minimize tax before the end of the financial year on June 30th, as well as changes coming into effect in future years. It discusses opportunities to make superannuation and other contributions, claims deductions for expenses, and manages capital gains and losses. It also outlines reforms increasing small business tax concessions and farm management deposit limits.