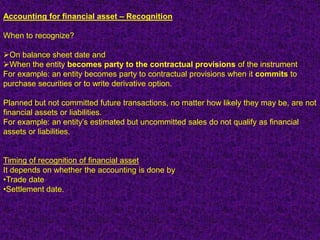

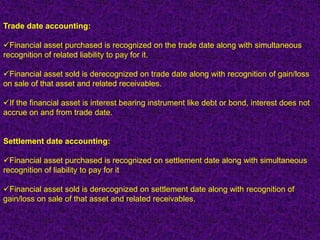

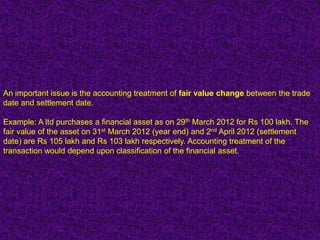

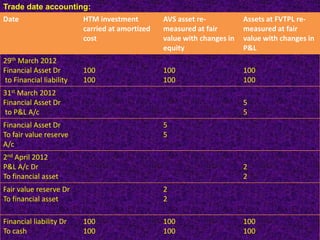

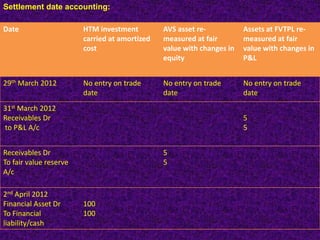

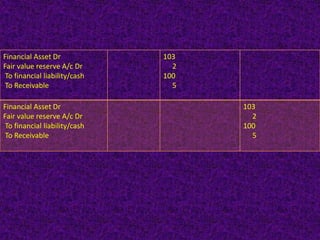

Financial assets must be recognized on the balance sheet date if the entity has become a party to the contractual provisions of the instrument. There are two approaches to recognition - trade date accounting and settlement date accounting. Trade date accounting recognizes assets and liabilities on the trade date, while settlement date accounting uses the settlement date. The appropriate accounting also depends on how the financial asset is classified and whether it is measured at amortized cost, fair value through other comprehensive income, or fair value through profit or loss.