Appeal format.depttl. appeals

•Download as PPT, PDF•

7 likes•16,673 views

The document discusses the process for filing an appeal before the Income Tax Appellate Tribunal (ITAT) and the Honorable High Court against an order of the Commissioner of Income Tax (Appeals). It provides details on the required forms and documents for filing an appeal to the ITAT, including the grounds of appeal. It also outlines the steps involved in filing an appeal before the High Court, such as obtaining approval from the Chief Commissioner of Income Tax and preparing relevant documents and authorization letters.

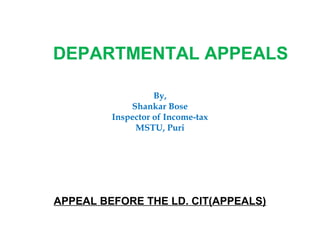

![FORM NO. 35

[ See rule 45 ]

Appeal to the Commissioner of Income-tax (Appeals)

Designation of the Commissioner (Appeals)

No…………… of ……………

Name and address of the appellant

Permanent Account Number

Assessment year in connection with which the appeal is

preferred

Assessing Officer/Valuation Officer passing the order appeal

against

Section and sub-section of the income-tax act, 1961, under

which the Assessing Officer/Valuation Officer passed the order

appealed against and the date of such order](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Appeal format.depttl. appeals

Similar to Appeal format.depttl. appeals (20)

More from Shankar Bose Sbose1958

More from Shankar Bose Sbose1958 (20)

Appeal format.depttl. appeals

- 1. DEPARTMENTAL APPEALS By, Shankar Bose Inspector of Income-tax MSTU, Puri APPEAL BEFORE THE LD. CIT(APPEALS)

- 2. FORM NO. 35 [ See rule 45 ] Appeal to the Commissioner of Income-tax (Appeals) Designation of the Commissioner (Appeals) No…………… of …………… Name and address of the appellant Permanent Account Number Assessment year in connection with which the appeal is preferred Assessing Officer/Valuation Officer passing the order appeal against Section and sub-section of the income-tax act, 1961, under which the Assessing Officer/Valuation Officer passed the order appealed against and the date of such order

- 3. Where the appeal relates to any tax deducted under section 195(1), the date of payment of the tax Where the appeal relates to any assessment or penalty, the date of service of the relevant notice of demand In any other case, the date of service of the intimation of the order appealed against Section and clause of the Income-tax Act, 1961, under which the appeal is preferred Where return has been filed by the appellant for the assessment year in connection with which the appeal is preferred, whether the tax due on the income returned has been paid in full ( if the answer is in affirmative, give details of date of payment and amount paid ) Where no return has been filed by the appellant for the assessment year in connection with which the appeal is preferred, whether an amount equal to the amount of advance tax payable by his during the financial year immediately preceding such assessment year has been paid ( if the answer is in affirmative, give details of date of payment and amount paid )

- 4. Relief claimed in appeal Whether an appeal in relation to any other assessment year is pending in the case of the appellant with any Commissioner (Appeals), give details as to the - (a) Commissioner (Appeals) with whom the appeal is pending (b) Assessment year in connection with which the appeal has been preferred (c) Assessing Officer passing the order appealed against (d) Section and sub-section of the Act, under which the Assessing Officer passed the order appealed against and the date of such order Address to which notices may be sent to the appellant ____________________ Signed ( Appellant)

- 5. STATEMENT OF FACTS GROUNDS OF APPEAL ____________________ Signed ( Appellant) Form of verification I, ___________________, the appellant, do hereby declare that what is stated above is true to the best of my information and belief. Place Signature Date : Status of appellant

- 6. APPEAL BEFORE APPELLATE TRIBUNAL

- 7. SCRUTINY REPORT 1. Name of the assessee 2. No. of appeal before CIT(A) and the date of appellate order 3. Date of receipt of the appellate order by the Assessing Officer 4. Assessment Year 5. Extent of reduction of tax liability 6. Whether notice of hearing of appeal ( including notice of adjournment was receipt by the assessing officer 7. Whether additional materials, evidences or information or documents were admitted or entertained by the Appellate authority 8. If additional materials, evidences or information or documents were admitted or entertained, the Assessing Officer’s comments on their admission by the appellate authority including particulars or opportunity given to the Assessing Officer to lead arguments or evidence in rebuttal

- 8. 9. Points allowed in appeal by the appellate authority to be mentioned serially and briefly 10. Assessing Officers Comments with reference to each points specified in item 9 ( Assessing Officer ) 11. Joint Commissioner of Income-tax’s comments ( Joint CIT )

- 9. SCRUTINY REPORT 1. Name of the assessee T & I Engineers (P) Ltd 2. No. of appeal before CIT(A) and the date of appellate order Tez-39/06-07 Dt. 26/03/2007 3. Date of receipt of the appellate order by the Assessing 23/04/2007 Officer 4. Assessment Year 2004-05 5. Extent of reduction of tax liability Rs. 16,60,175/- 6. Whether notice of hearing of appeal ( including notice of No adjournment was receipt by the assessing officer 7. Whether additional materials, evidences or information or No documents were admitted or entertained by the Appellate authority 8. If additional materials, evidences or information or Not applicable documents were admitted or entertained, the Assessing Officer’s comments on their admission by the appellate authority including particulars or opportunity given to the Assessing Officer to lead arguments or evidence in rebuttal

- 10. 9. Points allowed in appeal by the appellate authority to be The Ld. CIT(A) has mentioned serially and briefly directed to allow deduction u/s 80IC claimed by the assessee as against disallowance made by the Assessing Officer 10. Assessing Officers Comments with reference to each As per separate sheet points specified in item 9 ( Assessing Officer ) 11. Joint Commissioner of Income-tax’s comments ( Joint CIT )

- 11. 10. ASSESSING OFFICER’S COMMENTS : In this case the assessee filed its return of income on 27/10/2007 together with Audit Report u/s 44AB and Form No. 29B. In his return of Income, the assessee claimed a deduction of Rs. 44,47,396/- u/s 80IC of the I.T. Act, 1961, but audit report in Form 10CCB as required u/s 80-IA(7) read with section 80-IC(7) was not accompanied along with the return of income. The audit report in Form 10CCB was filed only on 21/08/2006. Accordingly, the A.O. refused to give cognizance of the audit report filed after a long period of filling return and entire amount of deduction claimed u/s 80-IC of the I.T. Act was disallowed. The Ld. CIT(A) observed that the requirement that audit report should be filed along with the return as prescribed u/s 80-IC(7) read with section 80-IA(7) is not a mandatory condition but only a directory. An audit report filed after submission of return but before framing of assessment would thus constitute sufficient compliance to the requirements of the section and directed to allow deduction u/s 80-IC. The Ld. CIT(A) appears to be not correct in allowing the deduction since the sub section 7 of section 80-IA clearly says that “ the deduction under sub-section 1 from profit and gains derived from an undertaking shall not be admissible unless the accounts of the undertaking for the previous year relevant to the assessment year for which the deduction is claimed have been audited …………….. And the assessee furnishes, along with his return of income, the report of such audit in the prescribed form duly signed and verified by such accountant.” From the above it is apparent that all assessee claiming deduction u/s 80-IC(1), furnishing of audit report in Form No.10ccB along with return of income is mandatory. In view of the above, second appeal is recommended.

- 12. 9. Points allowed in appeal by the appellate authority to be The Ld. CIT(A) has mentioned serially and briefly directed to allow deduction u/s 80IC claimed by the assessee as against disallowance made by the Assessing Officer 10. Assessing Officers Comments with reference to each As per separate sheet points specified in item 9 ( Assessing Officer ) 11. Joint Commissioner of Income-tax’s comments ( Joint CIT )

- 13. FORM NO. 36 [ See rule 47(1) ] Form of appeal to the Appellate Tribunal In the Income-tax Appellate tribunal …………………………………………………. Appeal No…………… of …………… ………………….. Versus …………………… APPELLANT RESPONDENT 1. The State in which the assessment was made 2. Section under which the order appealed against was passed 3. Assessment year in connection with which the appeal is preferred 3A. Total income declared by the assessee for the assessment year referred to in item 3 3B. Total income as computed by the Assessing Officer for the assessment year referred to in item 3 4. The Assessing Officer passing the original order

- 14. 5. Section of the Income-tax Act, 1961, under which Assessing Officer passed the order 6. The Deputy Commissioner (Appeals) in respect of orders passed before the 1st day of October, 1998/ Commissioner (Appeals) passing the order under section 154/250/271/271A/272A 7. The Deputy Commissioner or the Deputy Director in respect of orders passed before the 1st day of October, 1998, or the Joint Commissioner or the Joint Director passing the order under section 154/272A/274(2) 8. The Chief Commissioner or Director General or Director or Commissioner, passing the order under section 154(2)/250/263/271/271A/272A 9. Date of communication of the order appealed against 10. Address to which notices may be sent to the appellant 11. Address to which notices may be sent to the respondent 12. Relief claimed in appeal

- 15. GROUNDS OF APPEAL 1. 2. 3. 4. …................................. ………………………. Signed Signed ( Authorised representative, if any ) ( Appellant ) Verification I, ___________________, the appellant, do hereby declare that what is stated above is true to the best of my information and belief. Verified today the …………………… day of ……………. ……………. Signed

- 16. Notes : 1. The memorandum of appeal must be in triplicate and should be accompanied by two copies (at least one of which should be a certified copy) of the order appealed against, two copies of the relevant order of the Assessing Officer, two copies of the grounds of appeal before the first appellate authority, two copies of statement of facts, if any, filed before the said appellate authority, and also – (a) In the case of an appeal against an order levying penalty, two copies of the relevant assessment order, (b) In the case of an appeal against an order under section 143(3) read with section 144A, two copies of the direction of the Joint Commissioner under section 144A, (c) In the case of an appeal against an order under section 143(3) read with section 144B, two copies of the draft assessment order and two copies of the directions of the Joint Commissioner under section 144A, (d) In the case of an appeal against an order under section 143 read with section 147, two copies of the original assessment order, if any.

- 17. ACTION POINTS 1. Notes printed below the form are self explanatory and are required to be followed while preparing an appeal to the tribunal 2. Every appeal to the Tribunal is to be filed within 60days of the date of communication of the order to the assessee or the CCIT/CIT, as the case may be. 3. Jurisdiction of the Tribunal to which appeal may be filed is determined by an order under rule 4 of the Income-tax ( appellate Tribunal ) Act, 1963. 4. Normally the appeal is required to be presented to the Asstt. Registrar or, in his absence from office, to the Supeintendent/ Asstt Supeintendent/ Seniormost Head Clerk in the office during the office hours. 5. Where an appeal or application or cross-objection is filed which is connected with an appeal or application or cross-objection relating to the same party filed earlier, reference hereto should be made in the later appeal or application or cross-objection to facilitate their linking in the office of the Tribunal. 6. If an appeal or application or cross-objection is barred by time, an application for condonation of the delay supported by an affidavit and other documentary evidence for delay, should be made well in advance of the hearing.

- 18. FORM NO. 36 [ See rule 47(1) ] Form of appeal to the Appellate Tribunal In the Income-tax Appellate tribunal …………………………………………………. Appeal No…………… of …………… ………………….. Versus …………………… APPELLANT RESPONDENT 1. The State in which the assessment was made Assam 2. Section under which the order appealed against was U/s 250 passed 3. Assessment year in connection with which the appeal is 2004-05 preferred 3A. Total income declared by the assessee for the Nil assessment year referred to in item 3 3B. Total income as computed by the Assessing Officer for Rs. 45,98,560/- the assessment year referred to in item 3 4. The Assessing Officer passing the original order ACIT, Cir-Tezpur

- 19. 5. Section of the Income-tax Act, 1961, under which U/s 143(3)/115JB Assessing Officer passed the order 6. The Deputy Commissioner (Appeals) in respect of Not applicable orders passed before the 1st day of October, 1998/ Commissioner (Appeals) passing the order under section 154/250/271/271A/272A 7. The Deputy Commissioner or the Deputy Director in Not applicable respect of orders passed before the 1st day of October, 1998, or the Joint Commissioner or the Joint Director passing the order under section 154/272A/274(2) 8. The Chief Commissioner or Director General or Director CIT(A-1), Ghy or Commissioner, passing the order under section 154(2)/250/263/271/271A/272A 9. Date of communication of the order appealed against 23/04/2007 10. Address to which notices may be sent to the appellant ACIT, Cir-Tezpur, Aayakar Bhawan, Tez. 11. Address to which notices may be sent to the Kedarmal Smriti Bhawan, respondent Jenkins Rd. Tez. 12. Relief claimed in appeal As per grounds of appeal

- 20. GROUNDS OF APPEAL 1. As per separate sheet 2. 3. 4. …................................. ………………………. Signed Signed ( Authorised representative, if any ) ( Appellant )

- 21. Grounds of appeal 1. The Ld. CIT(A) has erred in law by observing that the audit report required to furnish along with return if income as prescribed u/s 80-IC read with section 80-IA is not a mandatory condition but only a directory. He is not justified in allowing deduction u/s 80- IC.

- 22. GROUNDS OF APPEAL 1. As per separate sheet 2. 3. 4. …................................. ………………………. Signed Signed ( Authorised representative, if any ) ( Appellant ) Verification I, ___________________, the appellant, do hereby declare that what is stated above is true to the best of my information and belief. Verified today the …………………… day of ……………. ……………. Signed

- 23. APPEAL BEFORE HON’BLE HIGH COURT

- 24. 1. Appeal is preferred against the order of the ITAT 2. Appeal is be filed within 120 days from the receipt of the ITAT’s order 3. For filling appeal before Hon’ble High Court, tax effect should be more than Rs. 5 lakhs and there must be law point involved 4. CIT will decide whether appeallable or not ( before taking decision, CIT calls proforma report from the A.O. and comments from the Range JCIT) 5. If necessary, CIT may seek opinion of the Departmental Standing Counsel 6. Proposal for filling appeal before Hon’ble High Court is sent to the CCIT for his approval.

- 25. 7. On receipt of CCIT’s approval, CIT prepares the following appeal papers – (a) Fact of the case (b) Question of law (c) CIT’s comments (d) One authorisation letter authorising the A.O. to represent the case (e) Wakalatnama authorising the standing counsel to represent the case (f) Copy of Asstt. Order (g) Copy of CIT(A)’s order (h) ITAT’s order in original 8. The above papers along with wakalatnama is handed over to the Departmental Standing Counsel and he files the appeal before the Hon’ble High Court.

- 26. APPEAL SCRUTINY REPORT 1 Jt / Addl CIT Range : Range – II / Kolkata 2 a) Appellate Range : C I T (A) – 8 , Kolkata b) No of appellate order & Date : 8 / 2006-07 / 39 , Dt. 27.03.07 3 Ward/Circle : ACIT Cir – 4 , Kolkata 4 Assessee’s name & Address : Sanjay Jaiswal 5 PAN : AAACJ 5434 B 6 Status : Individual 7 Assessment year : 2004 - 05+ 8 Accounting year : 2003 - 04 9 Sources of income with details of Business / Dealer in Iron Pipes Business, profession, vocation, if any: & Sanitary Fittings 10 Total income assessed : Rs. 47.94.060 11 Total demand raised : Rs. 20.03.697 12 Reduced income as per appeal order : Rs. 40.91.135 13 Revised demand as per appeal order : Rs. 16.95.161 14 Reduction in demand : Rs. 3.08.536 15 Whether tax has been fully paid : No 16 Whether appeal effect has been given: Yes 17 Whether necessary entries have been : Yes made in R-IV in respect of item 15 above 18 Give the Sl No in R-IV in respect : Arr. +- 4 / 2005 - 06 of item No 17 19 Grounds on which reduction is based : As per Appellate Order 20 ITO’s Remark : As per separate sheet 21 Information in respect of para-3 of CBDT’s instruction No 1979 dated 27.03.2000

- 27. Para-3, Adverse judgments relating to the following should be contested irrespective of revenue effect. i) Whether revenue audit objection in the case : has been accepted by the Department. No ii) Whether Board’s order, notification, instruction or : circular is the subject matter of an adverse order No iii) Whether prosecution proceedings are contemplated : against the assessee. No iv) Whether the constitutional validity of the Act are : under challenge. No ( NAME OF AO ) ITO / AC / DC , Ward/Circle….

- 28. Name : PAN : A.Y. Revised Total Income : 40.91.135 Date of Order : Tax Liability Order u/s 251 / 143 (3) In pursuance of order of Ld. C.I.T.(A) – 8, Kolkata vide Appeal Order no. ________ dt. ____ the order dt. _______ u/s 143(3) is revised as follows :- Total Income as per Order u/s 143(3) dt. ________ : 47.94.060 Less : Relief given for 1. Rate of Gross Profit : 1.16.387 2. Unexplained Cash Credit : 5.41.538 THANKS