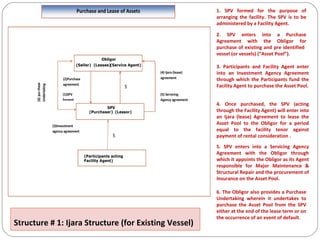

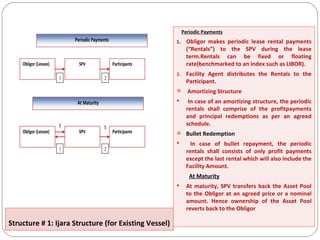

This document summarizes an Islamic finance presentation on emerging opportunities for Islamic ship financing. It outlines the concepts of Islamic finance, including a prohibition on interest (riba) and a focus on profit and loss sharing. It discusses the progress of Islamic banking, current market size, and recent deals in Islamic ship financing. Structures for Islamic ship financing include existing vessel financing using an ijara (lease) structure and newbuild vessel financing using an istisna'a (procurement contract) structure. Case studies of recent Islamic ship financing deals are also presented.