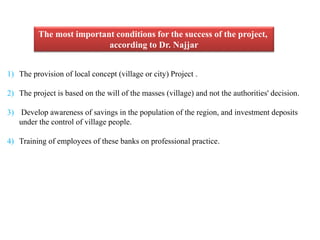

1) Pakistan was one of the first countries to implement Islamic banking in the 1960s and 1970s, with the founder of Pakistan calling for an Islamic banking system when establishing the State Bank of Pakistan in 1948.

2) Egypt started the first modern Islamic bank, called Mit Ghamr Savings Bank, in 1963 based on profit-sharing principles without interest. It succeeded in attracting many depositors and financing local projects until being shut down for political reasons in 1967.

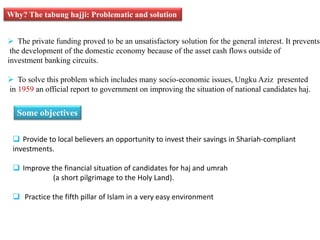

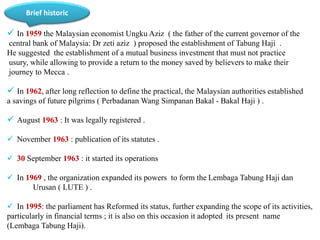

3) Malaysia established Tabung Haji in 1962 as the first Islamic bank in Asia to help Muslims save for the hajj pilgrimage, and it remains an important Islamic financial institution today.

![ The savings mitghamr boxes, and through its branches is the first Islamic bank in the world

(after the fall of the empire ottman) which adopted and encourage the participation of the Islamic

system [without riba].In order to expedite the movement of progress, economic growth

and social development.

Observation:

The local savings banks in Egypt is not a replica of the local savings banks in Germany,

because Germany has tried to apply this experience in Somalia and LatinAmerica, but it failed.

And the success of the Egyptian experience is mainly based on earning the trust of citizens.

And she has a point of similarity with the German savings banks in decentralization and

profit and individual savings](https://image.slidesharecdn.com/presentationo9mai-141201043734-conversion-gate01/85/Revisiting-the-modern-history-of-Islamic-finance-13-320.jpg)