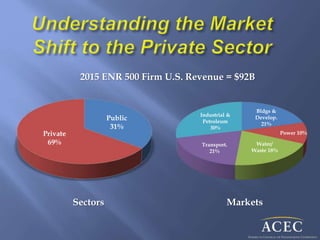

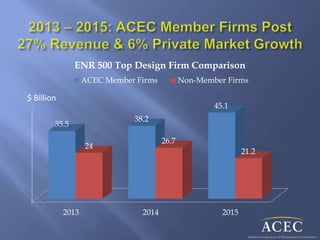

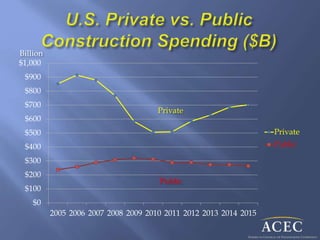

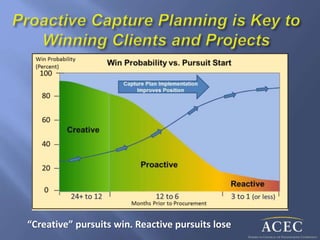

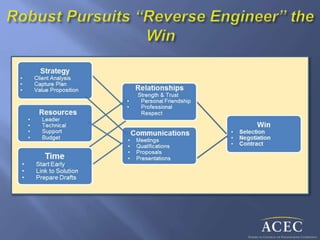

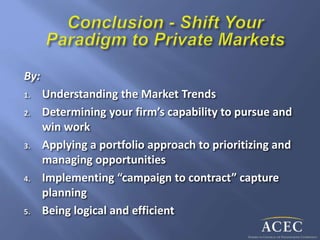

This document provides guidance on winning private sector opportunities in architecture, engineering, and construction (A/E/C) markets. It discusses understanding market trends, determining a firm's match to private client needs, and providing a toolbox to win work efficiently and effectively. Private sector construction spending exceeds $700 billion annually in the U.S. The webinar will help participants apply a portfolio approach to prioritizing opportunities and implement "campaign to contract" capture planning to logically and efficiently win private work.