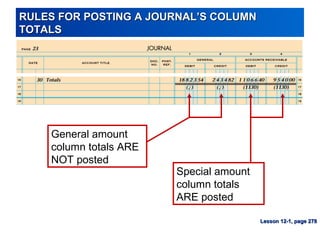

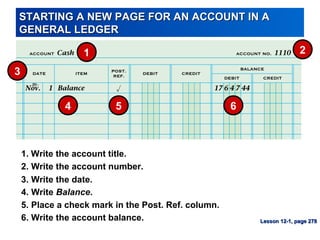

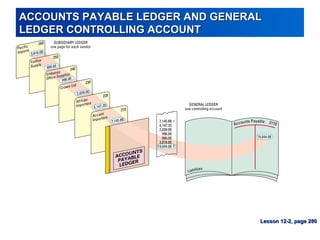

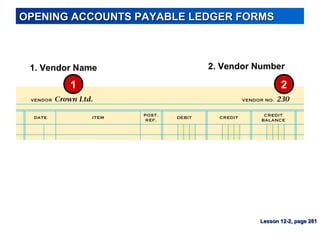

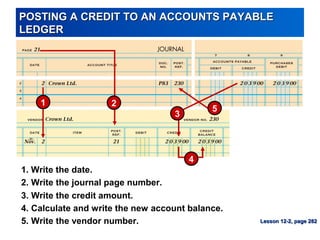

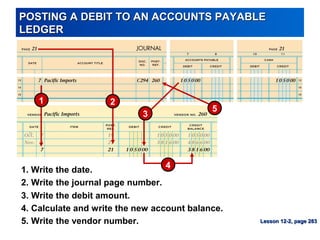

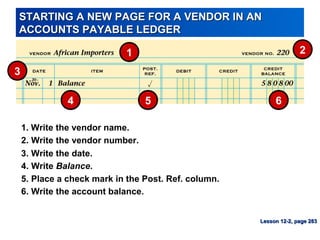

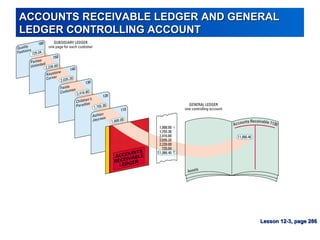

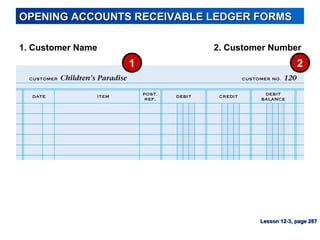

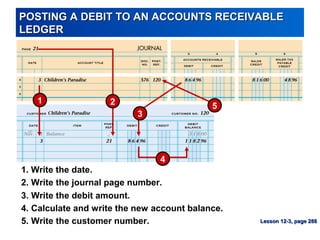

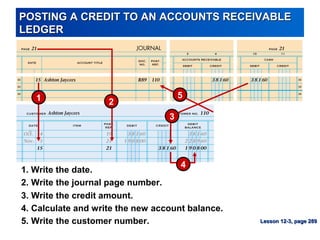

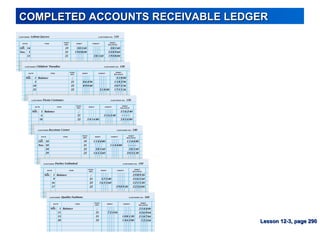

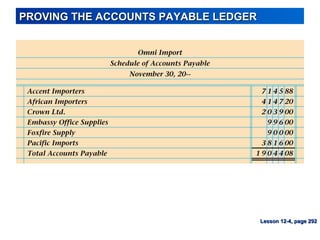

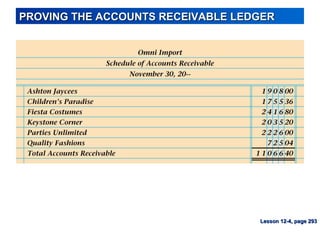

This document provides information and instructions about posting transactions from journals to general and subsidiary ledgers. It defines key terms like subsidiary ledger, accounts payable ledger, accounts receivable ledger, and controlling account. It also provides step-by-step instructions for posting debit and credit transactions to accounts payable and accounts receivable subsidiary ledgers, as well as starting new pages in general and subsidiary ledgers. The document explains how to prove the balances in subsidiary ledgers by creating schedules of accounts payable and accounts receivable.