❖ Accounts payableis the amount owed by an

entity to its vendors/suppliers for the goods

and services received.

❖ Amount owed by a business for purchases

made on credit

❖ Accounts Payable is a liability due to a

creditor

❖ It Include purchase related to BAU, FA, Raw

Material, Services, Utility

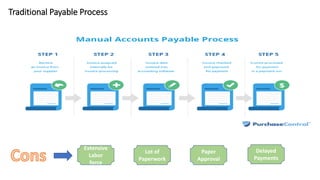

❖ Accounts payable and its management is a critical business process through which

an entity manages its payable obligations effectively.

❖ As the accounts payable process is vital for every organization, a lot of time needs

to be invested for its successful implementation. In order to have efficient

accounts, payable process automation becomes necessary. This will minimize the

time and cost of invoice processing, employee headcount and much more

3.

Characteristic of AP

•Timely - Major value of payable process is timely payment to vendor

/ supplier within due dates or payment terms

• Accuracy – Ensuring processing and payment is accurate as per the

invoice and terms

• Controls – Ensuring all process controls been check and verified

before invoice is ready for payments

• SOD / Approvals – Proper controls and segregation of duties is

exercised while invoices been processed and paid

• Processes – Best practice and processes been followed from

processing to payments

4.

Inclusion In AP

•An invoice is a document given to the buyer by the seller to collect payment. It includes the

cost of the products purchased or services rendered to the buyer. Invoices can also serve as

legal records, if they contain the names of the seller and client, description and price of

goods or services, and the terms of payment.

• PO is a commercial document and first official offer issued by a buyer to a seller indicating

types, quantities, and agreed prices for products or services.

• GL, CC & WBS – GL represents the record-keeping system for a company's financial data

with debit and credit account records validated by a trial balance. The GL provides a record

of each financial transaction that takes place during the life of an operating company

• ERP – ERP stands for Enterprise Resource Planning and refers to software and systems used

to plan and manage all the core supply chain, manufacturing, services, financial and other

processes of an organization

• Bank – Banks act as payment agents by conducting current account for customers,

paying cheques drawn by customers in the bank, and collecting cheques deposited to

customers' current accounts. Banks also enable customer payments via other payment

methods such as Automated Clearing House (ACH), Wire transfers or telegraphic

transfer, EFTPOS and automated teller machines (ATMs).

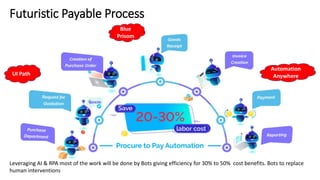

Futuristic Payable Process

LeveragingAI & RPA most of the work will be done by Bots giving efficiency for 30% to 50% cost benefits. Bots to replace

human interventions

UI Path

Automation

Anywhere

Blue

Prisom

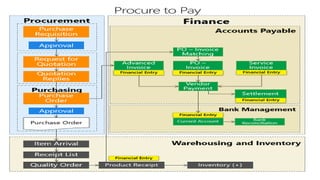

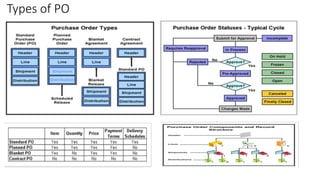

Types of PurchaseOrder

Standard Purchase Order - A standard purchase order

is typically used for irregular, infrequent or one-off

procurement. As mentioned above, it contains a

complete specification of the purchase, setting out the

price, quantity and timeframes for payment and

delivery.

A planned purchase order requires full details of the

goods and services to be purchased and their costs.

Dates for payment and delivery are also included in a

planned purchase order, but these are treated as

tentative dates. Issuing a release against the planned

purchase order places individual orders.

A blanket purchase order involves a purchaser agreeing

to purchase goods or services from a specific vendor,

but not at any specific quantity. Pricing may or may not

be confirmed in a blanket purchase order. This type of

order is typically used for repetitive procurement of a

specific set of items from a supplier such as basic

materials and supplies.

A contract purchase order sets out the vendor’s details

and potentially also payment and delivery terms. The

products to be purchased are not specified. A contract

purchase order is used to create an agreement and

terms of supply between a purchaser and vendor as

the basis for an ongoing commercial relationship. To

order a product, the purchaser may refer to the

contract purchase order when raising a standard

purchase order.

12.

❖ 2-way matchingverifies that invoice information matches the corresponding purchase order

❖ 3-way matching verifies that invoice information matches both the purchase order and the goods receipt

❖ 4-way matching adds another criterion to verify that the invoice details also match the acceptance or

inspection document in the case this step is part of the purchasing process

Types of Different PO / Invoice Match

The definition of invoice matching is the process of comparing information on the invoice with supporting

documents such as a purchase order, goods receipt, and contract. The invoice matching process aims to

ensure accurate vendor payments, correct accounting of costs and compliance to purchasing contracts as well

as to detect potential fraudulent invoices.

Invoice matching is used when a vendor invoice is preceded by a purchase order (PO) from the buying

organization. This means the buyer has created a purchase requisition stating the goods or services needed,

quantity, vendor and contracted price. Once the appropriate approvers within the organization have approved

the purchase requisition, a purchase order is generated and sent to the vendor. Upon delivery of the goods or

services, the buyer often needs to register a goods receipt in the ERP or procurement system.

Invoice & Types

•StandardInvoice: This is the most common form of invoice that small businesses create, and the format is flexible enough to fit most

industries and billing cycles.

•Commercial Invoice: Commercial invoices include details of the sale that are needed to determine customs duties for cross-border sales.

•Timesheet: A timesheet is an invoice used when a business or employee is billing based on the hours they work and their standard rate

of pay. Timesheets are used by contract employees who are paid hourly by their employer

•Recurring Invoice: Recurring invoices are useful for businesses that charge clients the same amount periodically for their services.

Recurring invoices are common among IT businesses, who charge their clients the same amount each month for a package IT service.

•Pro-Forma Invoice: A pro forma invoice is an estimated invoice that a business sends to a client before providing their services. A pro

forma invoice provides the client with an estimated cost of the work to be completed.

•Debit Memo: A debit invoice, also called a debit memo, is issued by a business that needs to increase the amount a client owes to the

business. Debit invoices can be useful to small businesses and freelancers when they need to make a slight adjustment to an existing bill.

An invoice, bill or tab is a commercial document issued by a seller to a buyer, relating to a sale transaction

and indicating the products, quantities, and agreed prices for products or services the seller had provided

the buyer.

16.

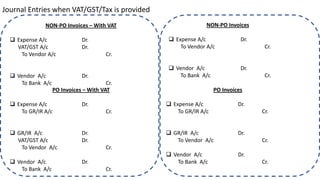

Journal Entries whenVAT/GST/Tax is provided

NON-PO Invoices – With VAT

❑ Expense A/c Dr.

VAT/GST A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

PO Invoices – With VAT

❑ Expense A/c Dr.

To GR/IR A/c Cr.

❑ GR/IR A/c Dr.

VAT/GST A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

NON-PO Invoices

❑ Expense A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

PO Invoices

❑ Expense A/c Dr.

To GR/IR A/c Cr.

❑ GR/IR A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

17.

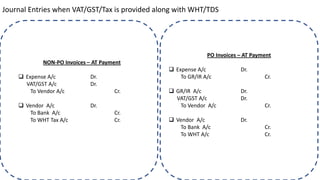

Journal Entries whenVAT/GST/Tax is provided along with WHT/TDS

NON-PO Invoices – AT Payment

❑ Expense A/c Dr.

VAT/GST A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

To WHT Tax A/c Cr.

PO Invoices – AT Payment

❑ Expense A/c Dr.

To GR/IR A/c Cr.

❑ GR/IR A/c Dr.

VAT/GST A/c Dr.

To Vendor A/c Cr.

❑ Vendor A/c Dr.

To Bank A/c Cr.

To WHT A/c Cr.

18.

Reasons –

Unable to

ProcessPO

Invoices

• Goods receipt Note not completed in PO

• Purchase Order Not Approved / Released

• Price Variance

• Quantity Variance

• Incorrect Vendor & Vendor not approved

• Incorrect Currency

• Bank Details Mismatch

• Final Invoice not ticket for milestone invoices

• GR Based not checked in purchase order

• Vendor blocked for invoice posting

19.

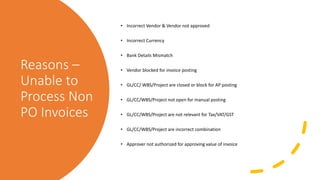

Reasons –

Unable to

ProcessNon

PO Invoices

• Incorrect Vendor & Vendor not approved

• Incorrect Currency

• Bank Details Mismatch

• Vendor blocked for invoice posting

• GL/CC/ WBS/Project are closed or block for AP posting

• GL/CC/WBS/Project not open for manual posting

• GL/CC/WBS/Project are not relevant for Tax/VAT/GST

• GL/CC/WBS/Project are incorrect combination

• Approver not authorized for approving value of invoice

20.

Controls – DuringInvoice Posting

VALID INVOICE AND BILLED TO

CORRECT ENTITY

ALL INVOICE ARE EITHER APPROVED

BY PO OR AUTHORIZED PERSON

THROUGH WORKFLOW OR MANUAL

DOA IS FOLLOWED FOR INVOICE

POSTING / AUDIT / PAYMENTS

PAYMENT PROCESS

Perform Duplicate

AuditCheck on

Invoices

Create Proposal &

Send to Business for

approval

Business –

Review &

Approve

Proposal

Complete Payment

with 2-3 days forward

as transfer date

Treasury to

maintain

adequate funding

in bank account

Review

Rejections

& Reset

Payments

Reconcile

Bank Vs

Payment

GL

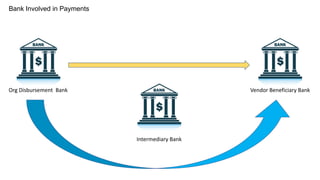

Bank Involved inPayments

Org Disbursement Bank Vendor Beneficiary Bank

Intermediary Bank

25.

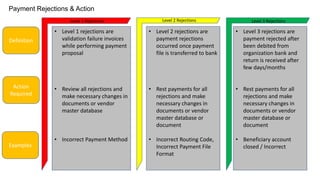

Payment Rejections &Action

• Level 1 rejections are

validation failure invoices

while performing payment

proposal

• Review all rejections and

make necessary changes in

documents or vendor

master database

• Incorrect Payment Method

• Level 3 rejections are

payment rejected after

been debited from

organization bank and

return is received after

few days/months

• Rest payments for all

rejections and make

necessary changes in

documents or vendor

master database or

document

• Beneficiary account

closed / Incorrect

• Level 2 rejections are

payment rejections

occurred once payment

file is transferred to bank

• Rest payments for all

rejections and make

necessary changes in

documents or vendor

master database or

document

• Incorrect Routing Code,

Incorrect Payment File

Format

Definition

Action

Required

Examples

Level 1 Rejections Level 2 Rejections Level 3 Rejections

26.

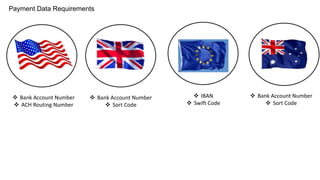

Payment Data Requirements

❖Bank Account Number

❖ ACH Routing Number

❖ Bank Account Number

❖ Sort Code

❖ IBAN

❖ Swift Code

❖ Bank Account Number

❖ Sort Code

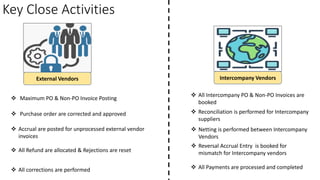

Key Close Activities

❖Maximum PO & Non-PO Invoice Posting

❖ All Payments are processed and completed

❖ All corrections are performed

❖ All Intercompany PO & Non-PO Invoices are

booked

❖ Accrual are posted for unprocessed external vendor

invoices

❖ Reconciliation is performed for Intercompany

suppliers

❖ Reversal Accrual Entry is booked for

mismatch for Intercompany vendors

❖ Netting is performed between Intercompany

Vendors

❖ All Refund are allocated & Rejections are reset

External Vendors Intercompany Vendors

❖ Purchase order are corrected and approved

29.

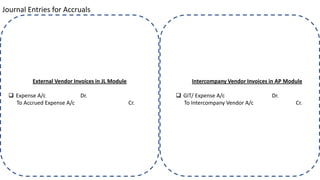

Journal Entries forAccruals

External Vendor Invoices in JL Module

❑ Expense A/c Dr.

To Accrued Expense A/c Cr.

Intercompany Vendor Invoices in AP Module

❑ GIT/ Expense A/c Dr.

To Intercompany Vendor A/c Cr.

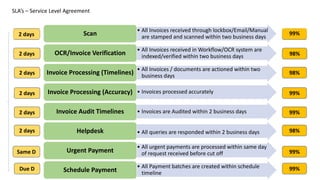

• All Invoicesreceived through lockbox/Email/Manual

are stamped and scanned within two business days

Scan

• All Invoices received in Workflow/OCR system are

indexed/verified within two business days

OCR/Invoice Verification

• All Invoices / documents are actioned within two

business days

Invoice Processing (Timelines)

• Invoices processed accurately

Invoice Processing (Accuracy)

• Invoices are Audited within 2 business days

Invoice Audit Timelines

• All queries are responded within 2 business days

Helpdesk

• All urgent payments are processed within same day

of request received before cut off

Urgent Payment

• All Payment batches are created within schedule

timeline

Schedule Payment

SLA’s – Service Level Agreement

2 days

2 days

2 days

2 days

2 days

Same D

Due D

2 days

98%

98%

99%

99%

98%

99%

99%

99%

32.

KPI – Key

Process

Indicator

•POT – Paid on Time

• Aged Creditor Trend Analysis

• Invoice Posted PO Penetration

• Invoice Posted Manually or EDI

• No of Reversals Processed

• No of Invoices Paid

• No of Invoices Paid by EFT, Wire, DD

• No of Invoices Processed Project Vs Non-Project Analysis

• FPY – First Pass Yield Trend Analysis

• Average days taken from Invoice Date to Payment Date

• Average days taken from Invoice receipt date to invoice posted date

• Payment Term Analysis Vs Vendor Category

• No of Payments Rejected

• No of Refunds Received

• No of reversal journals posted

• No of Invoices processed per FTE

• Average Cost per FTE

• No of queries received in helpdesk

• No of Down payment processed

• No of Refund Received

33.

Key Report

• OpenPurchase Order Report

• GR/IR Analysis Report

• Open Down Payment Report

• Open items report

• Cash Forecast

• Daily Production Report

• Dashboard Reporting

• Invoices on block Report

• FTE utilization report

• Inflow Analysis

• Spend Analysis – Based on Expense A/c and Vendor Category

• Predictive Analysis

• Tools Used for Automating Dashboards

• SPSS

• SQL

• PowerBI

• Tableau

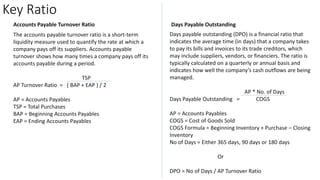

Key Ratio

Accounts PayableTurnover Ratio

The accounts payable turnover ratio is a short-term

liquidity measure used to quantify the rate at which a

company pays off its suppliers. Accounts payable

turnover shows how many times a company pays off its

accounts payable during a period.

TSP

AP Turnover Ratio = ( BAP + EAP ) / 2

AP = Accounts Payables

TSP = Total Purchases

BAP = Beginning Accounts Payables

EAP = Ending Accounts Payables

Days Payable Outstanding

Days payable outstanding (DPO) is a financial ratio that

indicates the average time (in days) that a company takes

to pay its bills and invoices to its trade creditors, which

may include suppliers, vendors, or financiers. The ratio is

typically calculated on a quarterly or annual basis and

indicates how well the company’s cash outflows are being

managed.

AP * No. of Days

Days Payable Outstanding = COGS

AP = Accounts Payables

COGS = Cost of Goods Sold

COGS Formula = Beginning Inventory + Purchase – Closing

Inventory

No of Days = Either 365 days, 90 days or 180 days

Or

DPO = No of Days / AP Turnover Ratio

](https://cdn.slidesharecdn.com/ss_thumbnails/ap1buytopay-120106210944-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)