Accounting Information Systems Controls Processes 3rd Edition Turner Test Bank

Accounting Information Systems Controls Processes 3rd Edition Turner Test Bank

Accounting Information Systems Controls Processes 3rd Edition Turner Test Bank

Accounting Information Systems Controls Processes 3rd Edition Turner Test Bank

Accounting Information Systems Controls Processes 3rd Edition Turner Test Bank

1.

Accounting Information SystemsControls

Processes 3rd Edition Turner Test Bank pdf

download

https://testbankdeal.com/product/accounting-information-systems-

controls-processes-3rd-edition-turner-test-bank/

Download more testbank from https://testbankdeal.com

2.

Instant digital products(PDF, ePub, MOBI) available

Download now and explore formats that suit you...

Accounting Information Systems Controls Processes 3rd

Edition Turner Solutions Manual

https://testbankdeal.com/product/accounting-information-systems-

controls-processes-3rd-edition-turner-solutions-manual/

testbankdeal.com

Accounting Information Systems The Processes Controls 2nd

Edition Turner Solutions Manual

https://testbankdeal.com/product/accounting-information-systems-the-

processes-controls-2nd-edition-turner-solutions-manual/

testbankdeal.com

Accounting Information Systems The Processes and Controls

2nd Edition Turner Test Bank

https://testbankdeal.com/product/accounting-information-systems-the-

processes-and-controls-2nd-edition-turner-test-bank/

testbankdeal.com

Intimate Relationships 7th Edition Miller Solutions Manual

https://testbankdeal.com/product/intimate-relationships-7th-edition-

miller-solutions-manual/

testbankdeal.com

3.

Business Statistics 2ndEdition Donnelly Solutions Manual

https://testbankdeal.com/product/business-statistics-2nd-edition-

donnelly-solutions-manual/

testbankdeal.com

Reinforced Concrete Mechanics And Design 7th Edition Wight

Solutions Manual

https://testbankdeal.com/product/reinforced-concrete-mechanics-and-

design-7th-edition-wight-solutions-manual/

testbankdeal.com

Bucks Step by Step Medical Coding 2019 Edition 1st Edition

Elsevier Test Bank

https://testbankdeal.com/product/bucks-step-by-step-medical-

coding-2019-edition-1st-edition-elsevier-test-bank/

testbankdeal.com

Inquiry into Physics 8th Edition Ostdiek Solutions Manual

https://testbankdeal.com/product/inquiry-into-physics-8th-edition-

ostdiek-solutions-manual/

testbankdeal.com

Compact Literature Reading Reacting Writing 8th Edition

Kirszner Test Bank

https://testbankdeal.com/product/compact-literature-reading-reacting-

writing-8th-edition-kirszner-test-bank/

testbankdeal.com

Ch 7 Testbank – 3e Page 1 of 32

ACCOUNTING INFORMATION SYSTEMS/3e

TURNER / WEICKGENANNT/COPELAND

Test Bank: CHAPTER 7: Auditing Information Technology – Bases Processes

NOTE: All new or adjusted questions are in red. New questions are identified by the letter A as part of

the question number; adjusted questions are identified by the letter X as part of the question number.

End of Chapter Questions:

1. Which of the following types of audits is most likely to be conducted for the purpose of

identifying areas for cost savings?

A. Financial Statement Audits

B. Operational Audits

C. Regulatory Audits

D. Compliance Audits

2. Financial statement audits are required to be performed by:

A. Governmental Auditors

B. CPAs

C. Internal Auditors

D. IT Auditors

3. Which of the following is not considered a cause for information risk?

A. Management’s geographic location is far from the source of the information needed to

make effective decisions.

B. The information is collected and prepared by persons who use the information for very

different purposes.

C. The information relates to business activities that are not well understood by those who

collect and summarize the information for decision makers.

D. The information has been tested by internal auditors and a CPA firm.

4. Which of the following is not a part of general accepted auditing standards?

A. General Standards

B. Standards of Fieldwork

C. Standards of Information Systems

D. Standards of Reporting

5. Which of the following best describes what is meant by the term “generally accepted auditing

standards”?

A. Procedures used to gather evidence to support the accuracy of a client’s financial

statements.

B. Measures of the quality of an auditor’s conduct carrying out professional responsibilities.

C. Professional pronouncements issued by the Auditing Standards Board.

D. Rules acknowledged by the accounting profession because of their widespread application.

6.

Ch 7 Testbank – 3e Page 2 of 32

6. In an audit of financial statement in accordance with generally accepted auditing standards, an

auditor is required to:

A. Document the auditor’s understanding of the client company’s internal controls.

B. Search for weaknesses in the operation of the client company’s internal controls.

C. Perform tests of controls to evaluate the effectiveness of the client company’s internal

controls.

D. Determine whether controls are appropriately operating to prevent or detect material

misstatements.

7. Auditors should develop a written audit program so that:

A. All material transactions will be included in substantive testing.

B. Substantive testing performed prior to year end will be minimized.

C. The procedures will achieve specific audit objectives related to specific management

assertions.

D. Each account balance will be tested under either a substantive test or a test of controls.

8. Which of the following audit objectives relates to the management assertion of existence?

A. A transaction is recorded in the proper period.

B. A transaction actually occurred (i.e., it is real)

C. A transaction is properly presented in the financial statements.

D. A transaction is supported by detailed evidence.

9. Which of the following statements regarding an audit program is true?

A. An audit program should be standardized so that it may be used on any client engagement.

B. The audit program should be completed by the client company before the audit planning

stage begins.

C. An audit program should be developed by the internal auditor during the audit’s

completion/reporting phase.

D. An audit program establishes responsibility for each audit test by requiring the signature

or initials of the auditor who performed the test.

10. Risk assessment is a process designed to:

A. Identify possible circumstances and events that may affect the business.

B. Establish policies and procedures to carry out internal controls.

C. Identify and capture information in a timely manner.

D. Review the quality of internal controls throughout the year.

11. Which of the following audit procedures is most likely to be performed during the planning

phase of the audit?

A. Obtain an understanding of the client’s risk assessment process.

B. Identify specific internal control activities that are designed to prevent fraud.

C. Evaluate the reasonableness of the client’s accounting estimates.

D. Test the timely cutoff of cash payments and collections.

7.

Ch 7 Testbank – 3e Page 3 of 32

12. Which of the following is the most significant disadvantage of auditing around the computer

rather than through the computer?

A. The time involved in testing processing controls is significant.

B. The cost involved in testing processing controls is significant.

C. A portion of the audit trail is not tested.

D. The technical expertise required to test processing controls is extensive.

13. The primary objective of compliance testing in a financial statement audit is to determine

whether:

A. Procedures have been updated regularly.

B. Financial statement amounts are accurately stated.

C. Internal controls are functioning as designed.

D. Collusion is taking place.

14. Which of the following computer assisted auditing techniques processes actual client input data

(or a copy of the real data) on a controlled program under the auditor’s control to periodically

test controls in the client’s computer system?

A. Test data method

B. Embedded audit module

C. Integrated test facility

D. Parallel simulation

15. Which of the following computer assisted auditing techniques allows fictitious and real

transactions to be processed together without client personnel being aware of the testing

process?

A. Test data method

B. Embedded audit module

C. Integrated test facility

D. Parallel simulation

16. Which of the following is a general control to test for external access to a client’s computerized

systems?

A. Penetration tests

B. Hash totals

C. Field checks

D. Program tracing

17. Suppose that during the planning phase of an audit, the auditor determines that weaknesses

exist in the client’s computerized systems. These weaknesses make the client company

susceptible to the risk of an unauthorized break-in. Which type of audit procedures should be

emphasized in the remaining phases of this audit?

A. Tests of controls

B. Penetration tests

C. Substantive tests

D. Rounding errors tests

8.

Ch 7 Testbank – 3e Page 4 of 32

18. Generalized audit software can be used to:

A. Examine the consistency of data maintained on computer files.

B. Perform audit tests of multiple computer files concurrently.

C. Verify the processing logic of operating system software.

D. Process test data against master files that contain both real and fictitious data.

19. Independent auditors are generally actively involved in each of the following tasks except:

A. Preparation of a client’s financial statements and accompanying notes.

B. Advising client management as to the applicability of a new accounting standard.

C. Proposing adjustments to a client’s financial statements.

D. Advising client management about the presentation of the financial statements.

20. Which of the following is most likely to be an attribute unique to the financial statement audit

work of CPAs, compared with work performed by attorneys or practitioners of other business

professions?

A. Due professional care

B. Competence

C. Independence

D. A complex underlying body of professional knowledge

21. Which of the following terms in not associated with a financial statement auditor’s requirement

to maintain independence?

A. Objectivity

B. Neutrality

C. Professional Skepticism

D. Competence

TEST BANK - CHAPTER 7 - MULTIPLE CHOICE

1. Accounting services that improve the quality of information provided to the decision maker, an

audit being the most common type of this service, is called:

A. Compliance Services

B. Assurance Services

C. Substantive Services

D. Operational Services

2. A type of assurance services that involves accumulating and analyzing support for the

information provided by management is called an:

A. Audit

B. Investigation

C. Financial Statement Examination

D. Control Test

3. The main purpose of an audit is to assure users of the financial information about the:

A. Effectiveness of the internal controls of the company.

B. Selection of the proper GAAP when preparing financial statements.

C. Proper application of GAAS during the examination.

D. Accuracy and completeness of the information.

9.

Ch 7 Testbank – 3e Page 5 of 32

4. Which of the following is not one of the three primary types of audits?

A. Compliance Audits

B. Financial Statement Audits

C. IT Audits

D. Operational Audits

5. This type of audit is completed in order to determine whether a company has adhered to the

regulations and policies established by contractual agreements, governmental agencies, or some

other high authority.

A. Compliance Audit

B. Operational Audit

C. Information Audit

D. Financial Statement Audit

6. This type of audit is completed to assess the operating policies and procedures of a client for

efficiency and effectiveness.

A. Efficiency Audit

B. Effectiveness Audit

C. Compliance Audit

D. Operational Audit

7. This type of audit is completed to determine whether or not the client has prepared and

presented its financial statements fairly, in accordance with established financial accounting

criteria.

A. GAAP Audit

B. Financial Statement Audit

C. Compliance Audit

D. Fair Application Audit

8. Financial statement audits are performed by _________ who have extensive knowledge of

generally accepted accounting principles (GAAP) in the US and/or International Financial

Reporting Standards (IFRS).

A. Public Auditors

B. Governmental Auditors

C. Certified Public Accountants

D. Internal Auditors

9. This type of auditor is an employee of the company he / she audits.

A. IT Auditor

B. Government Auditor

C. Certified Public Accountant

D. Internal Auditor

10.

Ch 7 Testbank – 3e Page 6 of 32

10. This type of auditor specializes in the information systems assurance, control, and security.

They may work for CPA firms, government agencies, or with the internal audit group.

A. IT Auditor

B. Government Auditor

C. Certified Public Accountant

D. Internal Auditor

11. This type of auditor conducts audits of government agencies or income tax returns.

A. IT Auditor

B. Government Auditor

C. Certified Public Accountant

D. Internal Auditor

12. An important requirement of CPA firms is that they must be ________ with regard to the

company being audited. The requirement allows CPA firms to provide a completely unbiased

opinion on the information it audits.

A. Neutral

B. Well-informed

C. Materially invested

D. All of the above

13. This type of audit is performed by independent auditors who are objective and neutral with

respect to the company and the information being audited.

A. Compliance Audit

B. Operational Audit

C. Internal Audit

D. External Audit

14. Which of the following scenarios does NOT impair the independence of a CPA firm from its

client?

A. The lead audit partner is the sister-in-law of the client’s VP of Accounting

B. One of the auditors owns stock in a competitor of the client

C. One of the auditors is the golf partner of the client’s CEO

D. The lead audit partner owns stock in the client

15. The independence of a CPA could be impaired by:

A. Having no knowledge of the company or the company management

B. By owning stock of a similar company

C. Having the ability to influence the client’s decisions

D. Being married to a stockbroker

11.

Ch 7 Testbank – 3e Page 7 of 32

16. Decision makers are typically forced to rely on others for information. When the source of the

information is removed from the decision maker, the information stands a greater chance of

being misstated. A decision maker may become detached from the source of information due

to geography, organizational layers, or other factors. This describes which cause of information

risk?

A. The lack of CPA independence

B. The volume and complexity of underlying data

C. The motive of the preparer

D. The remoteness of information

17. The IT environment plays a key role in how auditors conduct their work in all but which of the

following areas:

A. Consideration of Risk

B. Consideration of Information Fairness

C. Design and Performance of Audit Tests

D. Audit Procedures Used

18. The chance that information used by decision makers may be inaccurate is referred to as:

A. Sample Risk

B. Data Risk

C. Audit Trail Risk

D. Information Risk

19. Which of the following is not one of the identified causes of information risk?

A. Audited information

B. Remote information

C. Complexity of data

D. Preparer motive

20. The main reasons that it is necessary to study information-based processing and the related

audit function include:

A. Information users often do not have the time or ability to verify information themselves.

B. It may be difficult for decision makers to verify information contained in a computerized

accounting system.

C. Both of the above.

D. Neither of the above.

21. The existence of IT-based business processes often result in details of transactions being

entered directly into the computer system, results in a lack of physical evidence to visibly view.

This situation is referred to as:

A. Physical Evidence Risk

B. Loss of Audit Trail Visibility

C. Transaction Summary Chart

D. Lack of Evidence View

12.

Ch 7 Testbank – 3e Page 8 of 32

22. The existence of IT-based business processes, that result in the details of the transactions being

entered directly into the computer system, increases the likelihood of the loss or alternation of

data due to all of the following, except:

A. System Failure

B. Database Destruction

C. Programmer Incompetence

D. Environmental Damage

23. The advantages of using IT-based accounting systems, where the details of transactions are

entered directly into the computer include:

A. Computer controls can compensate for the lack of manual controls

B. Loss of audit trail view

C. Increased internal controls risks

D. Fewer opportunities to authorize and review transactions

24. The ten standards that provide broad guidelines for an auditor’s professional responsibilities are

referred to as:

A. Generally accepted accounting standards

B. General accounting and auditing practices

C. Generally accepted auditing practices

D. Generally accepted auditing standards

25. The generally accepted auditing standards are divided into three groups. Which of the following

is not one of those groups?

A. General Standards

B. Basic Standards

C. Standards of Fieldwork

D. Standards of Reporting

26. GAAS, generally accepted auditing standards, provide a general framework for conducting

quality audits, but the specific standards - or detailed guidance - are provided by all of the

following groups, except:

A. Public Company Accounting Oversight Board

B. Auditing Standards Board

C. Certified Fraud Examiners

D. International Auditing and Assurance Standards Board

27. This organization, established by the Sarbanes-Oxley Act, was organized in 2003 for the purpose

of establishing auditing standards for public companies.

A. Auditing Standards Board

B. Public Company Accounting Oversight Board

C. International Audit Practices Committee

D. Information Systems Audit and Control Association

13.

Ch 7 Testbank – 3e Page 9 of 32

28. This organization is part of the AICPA and was the group responsible for issuing Statements on

Auditing Standards which were historically widely used in practice.

A. Auditing Standards Board

B. Public Company Accounting Oversight Board

C. International Audit Practices Committee

D. Information Systems Audit and Control Association

29. This organization was established by the IFAC to set International Standards on Auditing (ISAs)

that contribute to the uniform application of auditing practices on a worldwide basis.

A. International Systems Audit and Control Association

B. Auditing Standards Board

C. Public Company Accounting Oversight Board

D. International Auditing and Assurance Standards Board (IAASB)

30. This organization issues guidelines for conducting the IT audit. The standards issued address

practices related to control and security of the IT system.

A. Auditing Standards Board

B. Public Company Accounting Oversight Board

C. International Audit Practices Committee

D. Information Systems Audit and Control Association

31. The audit is to be performed by a person or persons having adequate technical training and

proficiency as an auditor. This is one of the generally accepted auditing standards that is part of

the:

A. General Standards

B. Operating Standards

C. Fieldwork Standards

D. Reporting Standards

32. Independence in mental attitude is to be maintained in all matters related to the audit

engagement. This is one of the generally accepted auditing standards that is part of the:

A. General Standards

B. Operating Standards

C. Fieldwork Standards

D. Reporting Standards

33. The general guidelines, known as the generally accepted auditing standards, which include the

concepts of adequate planning and supervision, internal control, and evidence relate to the:

A. General Standards

B. Operating Standards

C. Fieldwork Standards

D. Reporting Standards

14.

Ch 7 Testbank – 3e Page 10 of 32

34. The general guidelines, known as the generally accepted auditing standards, which include the

concepts of presentation in accordance with the established criteria, the consistent application

of established principles, adequate disclosure, and the expression of an opinion, relate to the:

A. General Standards

B. Operating Standards

C. Fieldwork Standards

D. Reporting Standards

35. The role of the auditors is to analyze the underlying facts to decide whether information

provided by management is fairly presented. Auditors design ____1_____ to analyze

information in order to determine whether ____2_____ is/are valid.

A. 1=audit objectives; 2=management’s assertions

B. 1=audit tests; 2=audit objectives

C. 1=audit tests; 2=audit evidence

D. 1=audit tests; 2=management’s assertions

36. Although there are a number of organizations that provide detailed guidance, it is still necessary

for auditors to rely on other direction regarding the types of audit tests to use and the manner

in which the conclusions are drawn. These sources of information include:

A. Industry Guidelines

B. PCAOB

C. ASB

D. ASACA

37. Claims regarding the condition of the business organization and in terms of its operations,

financial results, and compliance with laws and regulations, are referred to as:

A. Financial Statements

B. Management Assertions

C. External Audit

D. Presentation and Disclosure

38. Which management assertion determines that transactions and related asset accounts balances

are actually owned and that liability account balances represent actual obligations?

A. Valuation and Allocation

B. Existence

C. Rights and Obligations

D. Classification and Presentation

39. Audit tests developed for an audit client are documented in a(n):

A. Audit Program

B. Audit Objective

C. Management Assertion

D. General Objectives

15.

Ch 7 Testbank – 3e Page 11 of 32

40. The management assertion related to valuation of transactions and account balances would

include all of the following, except:

A. Accurate in terms of dollar amounts and quantities

B. Supported by detailed evidence

C. Real

D. Correctly summarized

41. There are four primary phases of the IT audit. Which of the following is not one of those phases?

A. Planning

B. Evidence Audit

C. Tests of Controls

D. Substantive Tests

42. The main difference between substantive testing and controls testing is:

A. Substantive testing verifies whether information is correct, whereas control tests

determine whether the information is managed under a system that promotes

correctness.

B. Substantive testing determines whether the information is managed under a system that

promotes correctness, whereas Control testing verifies whether information is correct.

C. Substantive testing goes further in depth into the internal controls of a company, whereas

controls testing just identifies which controls need further review.

D. Substantive testing identifies which controls need further review, whereas controls testing

goes further in depth into the internal controls of a company.

43. During substantive testing, if material misstatements have been found to exist, which of the

following actions should be taken next?

A. Proceed to the audit completion in the reporting phase

B. Re-evaluate the audit risk in the planning phase

C. Re-perform detailed tests of balances

D. Re-perform an internal controls systems analysis

44. The proof of the fairness of the financial information is:

A. Tests of Controls

B. Substantive Tests

C. Audit Completion

D. Audit Evidence

45. Techniques used for gathering evidence include all of the following, except:

A. Physical examination of assets or supporting documentation

B. Observing activities

C. Adequate planning and supervision

D. Analyzing financial relationships

16.

Ch 7 Testbank – 3e Page 12 of 32

46. During this phase of the audit, the auditor must gain a thorough understanding of the client’s

business and financial reporting systems. When completing this phase, the auditors review and

assess the risks and controls related to the business.

A. Tests of Controls

B. Substantive Tests

C. Audit Completion / Reporting

D. Audit Planning

47. During the planning phase of the audit, auditors estimate the monetary amounts that are large

enough to make a difference in decision making. This amount is referred to as:

A. Risk

B. Materiality

C. Substantive

D. Sampling

48. The likelihood that errors or fraud may occur is referred to as:

A. Risk

B. Materiality

C. Control Tests

D. Sampling

49. A large part of the work performed by an auditor in the audit planning process is the gathering

of evidence about the company’s internal controls. This can be completed in any of the

following ways, except:

A. Interviewing key members of the accounting and IT staff.

B. Observing policies and procedures

C. Review IT user manuals and systems

D. Preparing memos to summarize their findings

50. Auditing standards address the importance of understanding both the automated and manual

procedures that make up an organization’s internal controls and consider how misstatements

may occur, including all of the following, except:

A. How transactions are entered into the computer

B. How financial statement are printed from the computer

C. How nonstandard journal entries and adjusting entries are initiated, recorded, and

processed.

D. How standard journal entries are initiated, recorded, and processed.

51. IT auditors may need to be called in to:

A. Consider the effects of computer processing on the audit.

B. To assist in testing the automated processes.

C. Both of the above.

D. None of the above.

17.

Ch 7 Testbank – 3e Page 13 of 32

52. Many companies design their IT system so that all documents and reports can be retrieved from

the system in readable form. Auditors can then compare the documents used to input the data

into the system with reports generated from the system, without gaining any extensive

knowledge of the computer system and does not require the evaluation of computer controls.

This process is referred to as:

A. Auditing through the system

B. Auditing around the system

C. Computer assisted audit techniques

D. Auditing with the computer

53. The audit practice of “auditing around the computer” is also referred to as:

A. The white box approach

B. The black box approach

C. Computer-assisted audit techniques (CAATs)

D. The gray box approach

54. Which of the following is the most effective way of auditing the internal controls of an IT

system?

A. Auditing with the Computer

B. Auditing through the computer

C. Auditing around the computer

D. Auditing in the computer

55. This approach, referred to as the whitebox approach, requires auditors to evaluate IT controls

and processing so that they can determine whether the information generated from the system

is reliable.

A. Auditing through the system

B. Auditing around the system

C. Computer assisted audit techniques

D. Auditing with the computer

56. The IT auditing approach referred to as “Auditing through the system” is necessary under which

of the following conditions?

A. Supporting documents are available in both electronic and paper form.

B. The auditor does not require evaluation of computer controls.

C. The auditor wants to test computer controls as a basis for evaluating risk and reducing the

amount of substantive audit testing required.

D. The use of the IT system has a low impact on the conduct of the audit.

57. Audit procedures designed to evaluate both general controls and application controls are

referred to as:

A. Substantive Tests

B. Audit Planning

C. IT Auditing

D. Test of Controls

18.

Ch 7 Testbank – 3e Page 14 of 32

58. The automated controls that affect all computer applications are referred to as:

A. General Controls

B. Specific Controls

C. Input Controls

D. Application Controls

59. Which of the following describes a mathematical sum of data that is meaningless to the financial

statements but useful for controlling the data and detecting possible missing items?

A. Hash Total

B. Batch Total

C. Validation Check

D. Sequence Verification total

60. The two broad categories of general controls that relate to IT systems include which of the

following:

A. IT systems documentation

B. IT administration and the related operating systems development and maintenance

processes

C. Authenticity table

D. Computer security and virus protection

61. Related audit tests to review the existence and communication of company policies regarding

important aspects of IT administrative control include all of the following, except:

A. Personal accountability and segregation of incompatible responsibilities

B. Job description and clear lines of authority

C. Prevention of unauthorized access

D. IT systems documentation

62. Auditors may send text messages through a company’s system to find out whether encryption

of private information is occurring properly. In addition, special software programs are available

to help auditors identify weak points in a company’s security measures. These are examples of:

A. Penetration tests

B. Authenticity tests

C. Vulnerability assessments

D. Access log reviews

63. Controls meant to prevent the destruction of information as the result of unauthorized access to

the IT system are referred to as:

A. IT administration

B. System controls

C. Information administration

D. Security controls

19.

Ch 7 Testbank – 3e Page 15 of 32

64. In addition to testing system documentation, auditors should test the three main functions of

computer applications. Which of the following is not one of these functions?

A. Output

B. Input

C. Processing

D. Data Storage

65. All of the following are examples of security controls except for?

A. Biometric access controls

B. Swipe Key access controls

C. Online firewall protection controls

D. All of the Above are examples of security controls

66. Auditors should perform this type of test to determine the valid use of the company’s computer

system, according to the authority tables.

A. Authenticity tests

B. Penetration tests

C. Vulnerability assessments

D. IT systems documentation

67. These tests of the security controls involve various methods of entering the company’s system

to determine whether controls are working as intended.

A. Authenticity tests

B. Penetration tests

C. Vulnerability assessments

D. IT systems documentation

68. These tests of security controls analyze a company’s control environment for possible

weaknesses. Special software programs are available to help auditors identify weak points in

their company’s security measures.

A. Authenticity tests

B. Penetration tests

C. Vulnerability assessments

D. IT systems documentation

69. One of the most effective ways a client can protect its computer system is to place physical

controls in the computer center. Physical controls include all of the following, except:

A. Proper temperature control

B. Locks

C. Security guards

D. Cameras

70. One of the most effective ways a client can protect its computer system is to place

environmental controls in the computer center. Environmental controls include:

A. Card keys

B. Emergency power supply

C. Alarms

D. Security guards

20.

Ch 7 Testbank – 3e Page 16 of 32

71. This type of application control is performed to verify the correctness of information entered

into software programs. Auditors are concerned about whether errors are being prevented and

detected during this stage of data processing.

A. Security controls

B. Processing controls

C. Input controls

D. Output controls

72. IT audit procedures typically include a combination of data accuracy tests where the data

processed by computer applications are reviewed for correct dollar amounts or other numerical

values. These procedures are referred to as:

A. Security controls

B. Processing controls

C. Input controls

D. Output controls

73. This type of processing control test involves a comparison of different items that are expected

to have the same values, such as comparing two batches or comparing actual data against a

predetermined control total.

A. Validation Checks

B. Batch Totals

C. Run-to-Run Totals

D. Balancing Tests

74. This law, also known as the first-digit law, was named after a physicist who discovered a specific,

but non-uniform pattern in the frequency of digits occurring as the first number in a list of

numbers:

A. Number-up Law

B. Benford’s Law

C. Adams’ Digit Law

D. Jackson First Digit Law

75. This is one of the computer-assisted audit techniques related to processing controls that

involves processing company data through a controlled program designed to resemble the

company’s application. This test is run to find out whether the same results are achieved under

different systems.

A. Integrated Test Facility

B. Embedded Audit Module

C. Parallel Simulation

D. Test Data Method

76. Regardless of whether the results are printed or retained electronically, auditors may perform

all of the following procedures to test application outputs, except:

A. Integrated Tests

B. Reasonableness Tests

C. Audit Trail Tests

D. Rounding Errors Tests

21.

Ch 7 Testbank – 3e Page 17 of 32

77. The auditor’s test of the accuracy of monetary amounts of transactions and account balances is

known as:

A. Testing of controls

B. Substantive tests

C. Compliance tests

D. Application tests

78. A process of constant evidence gathering and analysis to provide assurance on the information

as soon as it occurs, or shortly thereafter, is referred to as:

A. Real-time auditing

B. Virtual auditing

C. E-auditing

D. Continuous auditing

79. This phase of auditing occurs when the auditors evaluate all the evidence that has been

accumulated and makes a conclusion based on that evidence.

A. Tests of Controls

B. Audit Planning

C. Audit Completion / Reporting

D. Substantive Testing

80. This piece of audit evidence is often considered to be the most important because it is a signed

acknowledgment of management’s responsibility for the fair presentation of the financial

statements and a declaration that they have provided complete and accurate information to the

auditors during all phases of the audit.

A. Letter of Representation

B. Audit Report

C. Encounter Statement

D. Auditors Contract

81. Which of the following is a proper description of an auditor report?

A. Unqualified opinion - identifies certain exceptions to the clean opinion.

B. Adverse opinion - notes that there are material misstatements presented.

C. Qualified opinion - states that the auditors believe the financial statements are fairly and

consistently presented in accordance with GAAP.

D. Unqualified opinion - states that the auditors were not able to reach a conclusion.

82. When PCs are used for accounting instead of mainframes or client-server system, they face a

greater risk of loss due to which of the following:

A. Authorized access

B. Segregation of duties

C. Lack of backup control

D. All of the above

22.

Ch 7 Testbank – 3e Page 18 of 32

83. When companies rely on external, independent computer service centers to handle all or part of

their IT needs it is referred to as:

A. External Processing

B. WAN Processing

C. Database Management System

D. IT Outsourcing

84. Because it is not possible to test all transactions and balances, auditors rely on this to choose

and test a limited number of items and transactions and then make conclusions about the

balance as a whole.

A. Sampling

B. Materiality

C. Compliance

D. Substance

85. All types of auditors must follow guidelines promoting ethical conduct. For financial statement

auditors, the PCAOB/AICPA has established a Code of Professional Conduct, commonly called

the Code of Ethics, which consists of two sections. Which of the following correctly states the

two sections?

A. Integrity and responsibility

B. Principles and rules

C. Objectivity and independence

D. Scope and nature

86. The rule in the PCAOB/AICPA Code of Professional Conduct that is referred to as Responsibilities,

can be stated as:

A. CPAs should act in a way that will serve the public interest, honor the public trust, and

demonstrate commitment to professionalism.

B. To maintain and broaden public confidence, CPAs should perform their professional duties

with the highest sense of integrity.

C. In carrying out their professional duties, CPAs should exercise sensitive professional and

moral judgments in all their activities.

D. CPAs in public practice should observe the principles of the Code of Professional Conduct in

determining the scope and nature of services to be provided.

87. This concept means that the auditors should not automatically assume that their clients are

honest, but that they (the auditors) must have a questioning mind and a persistent approach to

evaluating evidence for possible misstatements.

A. Independence

B. Integrity

C. Due Care

D. Professional Skepticism

23.

Ch 7 Testbank – 3e Page 19 of 32

TEST BANK - CHAPTER 7 - TRUE / FALSE

1. All users of financial data - business managers, investors, creditors, and government agencies -

have an enormous amount of data to use to make decisions. Due to the use of IT systems, it is

easy to verify the accuracy and completeness of the information.

FALSE

2. In order to properly carry out an audit, accountants collect and evaluate proof of procedures,

transactions, and / or account balances, and compare the information with established

criteria.

TRUE

3. The only person who can perform a financial statement audit of a publicly traded company is a

government auditor who has extensive knowledge of generally accepted accounting

principles.

FALSE

4. Any professionally trained accountant is able to perform an operational audit.

TRUE

5. An important requirement for CPA firms is that they must be personally involved with the

management of the firm that is being audited.

FALSE

6. The most common type of audit service is the operating audit performed by internal auditors.

FALSE

7. All types of auditors should have knowledge about technology-based systems so that they can

properly audit IT systems.

TRUE

8. A financial statement audit is part of the IT audit.

FALSE

9. Auditors do not need to be experts on the intricacies of computer systems but they do need to

understand the impact of IT on their clients’ accounting systems and internal controls.

TRUE

10. An internal auditor is not allowed to assist in the performance of a financial statement audit.

FALSE

11. A financial statement audit is conducted in order for an opinion to be expressed on the fair

presentation of financial statements. This goal is affected by the presence or absence of IT

accounting systems.

FALSE

24.

Ch 7 Testbank – 3e Page 20 of 32

12. Information risk is the chance that information used by decision makers may be inaccurate.

TRUE

13. As a business grows, the volume and complexity of its transactions increase. At the same timed,

there is a decrease in the chance that misstated information may exist undetected.

FALSE

14. The remoteness of information, one of the causes of information risk, can relate to geographic

distance or organizational layers.

TRUE

15. The most common method for decision makers to reduce information risk is to rely on

information that has been audited by an independent party.

TRUE

16. Auditors have the primary responsibility to make sure that they comply with international

standards in all cases.

FALSE

17. There is not much room for professional judgement when performing audits, as a result of the

detailed guidance provided by organizations, such as the PCAOB.

FALSE

18. The responsibility for operations, compliance, and financial reporting lies with the auditors.

FALSE

19. The role of the auditor is to analyze the underlying facts to decide whether information

provided by management is fairly presented.

TRUE

20. Management assertions relate to the actual existence and proper valuation of transactions

and account balances.

TRUE

21. The same audit tests would test for completeness of a liability or an asset.

FALSE

22. Auditing testing for any single general auditing objective would involve the same testing

techniques even though there are different types of information collected to support different

accounts and transactions.

FALSE

23. Auditors must think about how the features of a company’s IT systems influence its

management assertions and the general audit objectives even though these matters have

little or no impact on the choice of audit methodologies used.

FALSE

24. Risk can be inherent in the company’s business, due to things such as the nature of

25.

Ch 7 Testbank – 3e Page 21 of 32

operations, or may be caused by weak internal controls.

TRUE

25. The audit planning process is unlikely to vary if the company has adopted IFRS, or is in the

process of convergence.

FALSE

26. Adapting to fair value measures in the preparation of IFRS-based financial statements will

likely cause auditors to evaluate supporting evidence differently than if US GAAP was used.

TRUE

27. IFRS does not allow as much use of judgment as is allowed under GAAP.

FALSE

28. Auditors do not need to concern themselves with risks unless there is an indication that there

is an internal control weakness.

FALSE

29. The auditor’s understanding of internal controls provides the basis for designing appropriate

audit tests to be used in the remaining phases of the audit.

TRUE

30. The process of evaluating internal controls and designing meaningful audit tests is more

complex for manual systems than for automated systems.

FALSE

31. Computer-assisted audit techniques are useful audit tools because they make it possible for

auditors to use computers to audit large amounts of evidence in less time.

TRUE

32. In order to enhance controls, reconciliations should be performed by company personnel who

are independent from the tasks of initiating or recording the transactions with the accounts

being reconciled.

TRUE

33. Substantive tests are also referred to as compliance tests.

FALSE

34. General controls relate to specific software and application controls relate to all aspects of the

IT environment.

FALSE

35. General controls must be tested before application controls.

TRUE

26.

Ch 7 Testbank – 3e Page 22 of 32

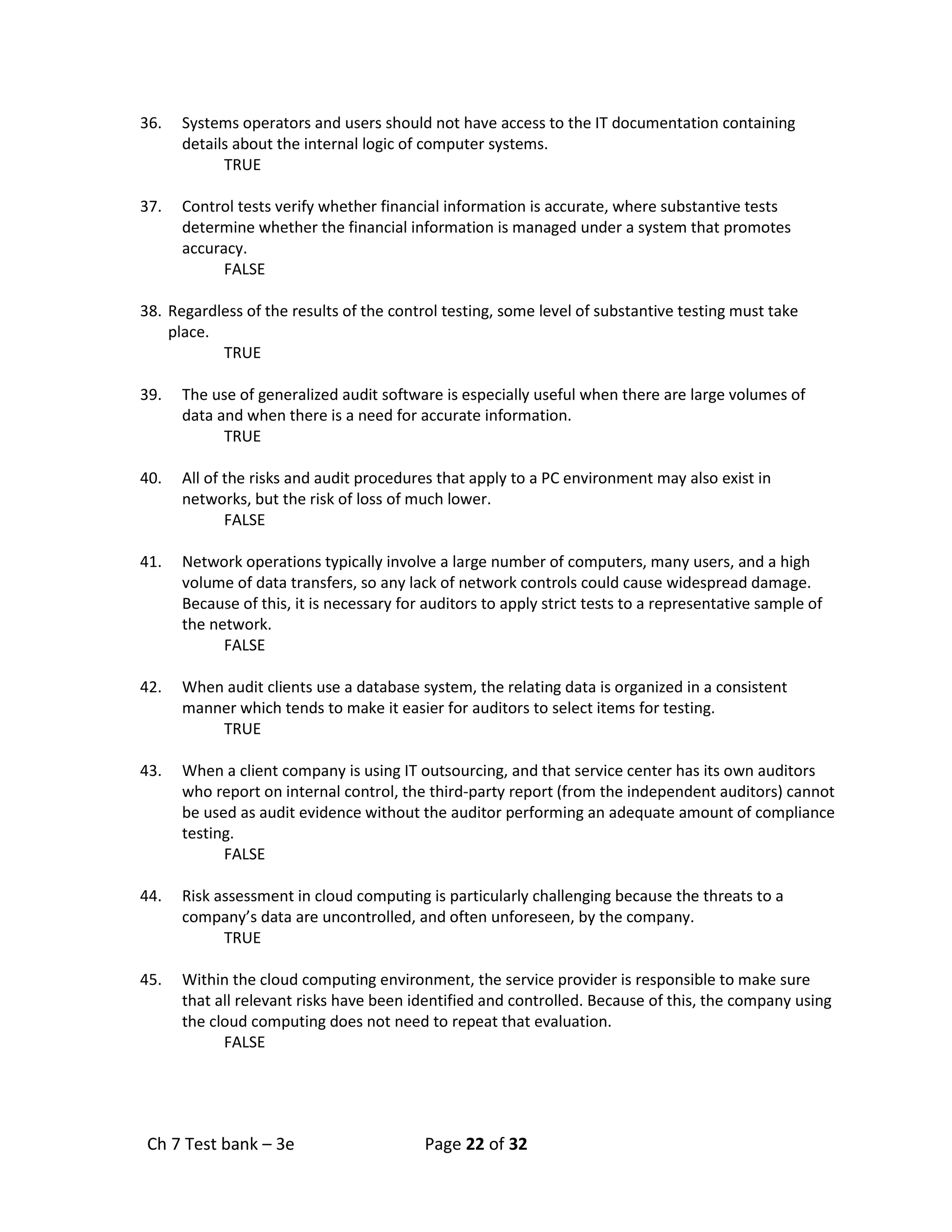

36. Systems operators and users should not have access to the IT documentation containing

details about the internal logic of computer systems.

TRUE

37. Control tests verify whether financial information is accurate, where substantive tests

determine whether the financial information is managed under a system that promotes

accuracy.

FALSE

38. Regardless of the results of the control testing, some level of substantive testing must take

place.

TRUE

39. The use of generalized audit software is especially useful when there are large volumes of

data and when there is a need for accurate information.

TRUE

40. All of the risks and audit procedures that apply to a PC environment may also exist in

networks, but the risk of loss of much lower.

FALSE

41. Network operations typically involve a large number of computers, many users, and a high

volume of data transfers, so any lack of network controls could cause widespread damage.

Because of this, it is necessary for auditors to apply strict tests to a representative sample of

the network.

FALSE

42. When audit clients use a database system, the relating data is organized in a consistent

manner which tends to make it easier for auditors to select items for testing.

TRUE

43. When a client company is using IT outsourcing, and that service center has its own auditors

who report on internal control, the third-party report (from the independent auditors) cannot

be used as audit evidence without the auditor performing an adequate amount of compliance

testing.

FALSE

44. Risk assessment in cloud computing is particularly challenging because the threats to a

company’s data are uncontrolled, and often unforeseen, by the company.

TRUE

45. Within the cloud computing environment, the service provider is responsible to make sure

that all relevant risks have been identified and controlled. Because of this, the company using

the cloud computing does not need to repeat that evaluation.

FALSE

27.

Ch 7 Testbank – 3e Page 23 of 32

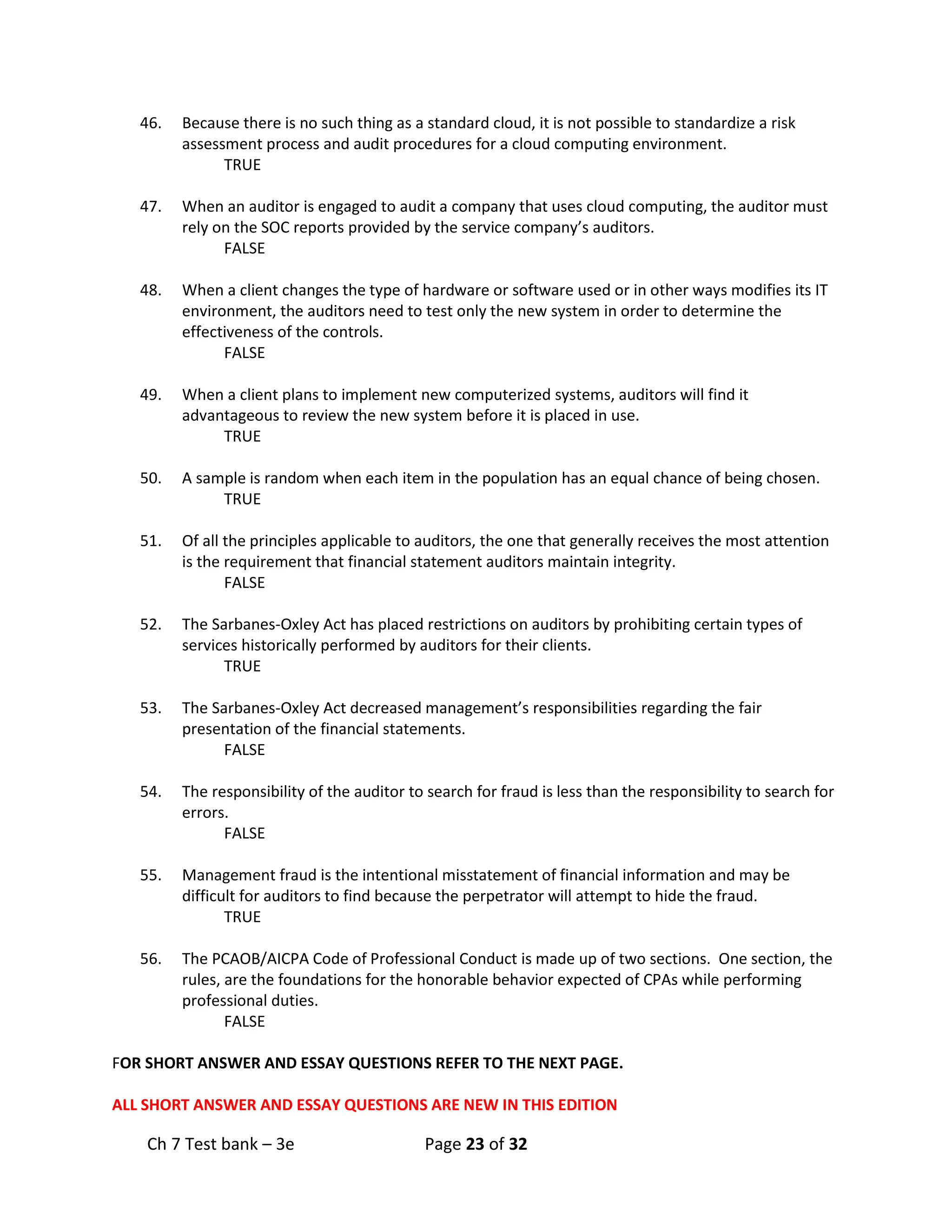

46. Because there is no such thing as a standard cloud, it is not possible to standardize a risk

assessment process and audit procedures for a cloud computing environment.

TRUE

47. When an auditor is engaged to audit a company that uses cloud computing, the auditor must

rely on the SOC reports provided by the service company’s auditors.

FALSE

48. When a client changes the type of hardware or software used or in other ways modifies its IT

environment, the auditors need to test only the new system in order to determine the

effectiveness of the controls.

FALSE

49. When a client plans to implement new computerized systems, auditors will find it

advantageous to review the new system before it is placed in use.

TRUE

50. A sample is random when each item in the population has an equal chance of being chosen.

TRUE

51. Of all the principles applicable to auditors, the one that generally receives the most attention

is the requirement that financial statement auditors maintain integrity.

FALSE

52. The Sarbanes-Oxley Act has placed restrictions on auditors by prohibiting certain types of

services historically performed by auditors for their clients.

TRUE

53. The Sarbanes-Oxley Act decreased management’s responsibilities regarding the fair

presentation of the financial statements.

FALSE

54. The responsibility of the auditor to search for fraud is less than the responsibility to search for

errors.

FALSE

55. Management fraud is the intentional misstatement of financial information and may be

difficult for auditors to find because the perpetrator will attempt to hide the fraud.

TRUE

56. The PCAOB/AICPA Code of Professional Conduct is made up of two sections. One section, the

rules, are the foundations for the honorable behavior expected of CPAs while performing

professional duties.

FALSE

FOR SHORT ANSWER AND ESSAY QUESTIONS REFER TO THE NEXT PAGE.

ALL SHORT ANSWER AND ESSAY QUESTIONS ARE NEW IN THIS EDITION

28.

Ch 7 Testbank – 3e Page 24 of 32

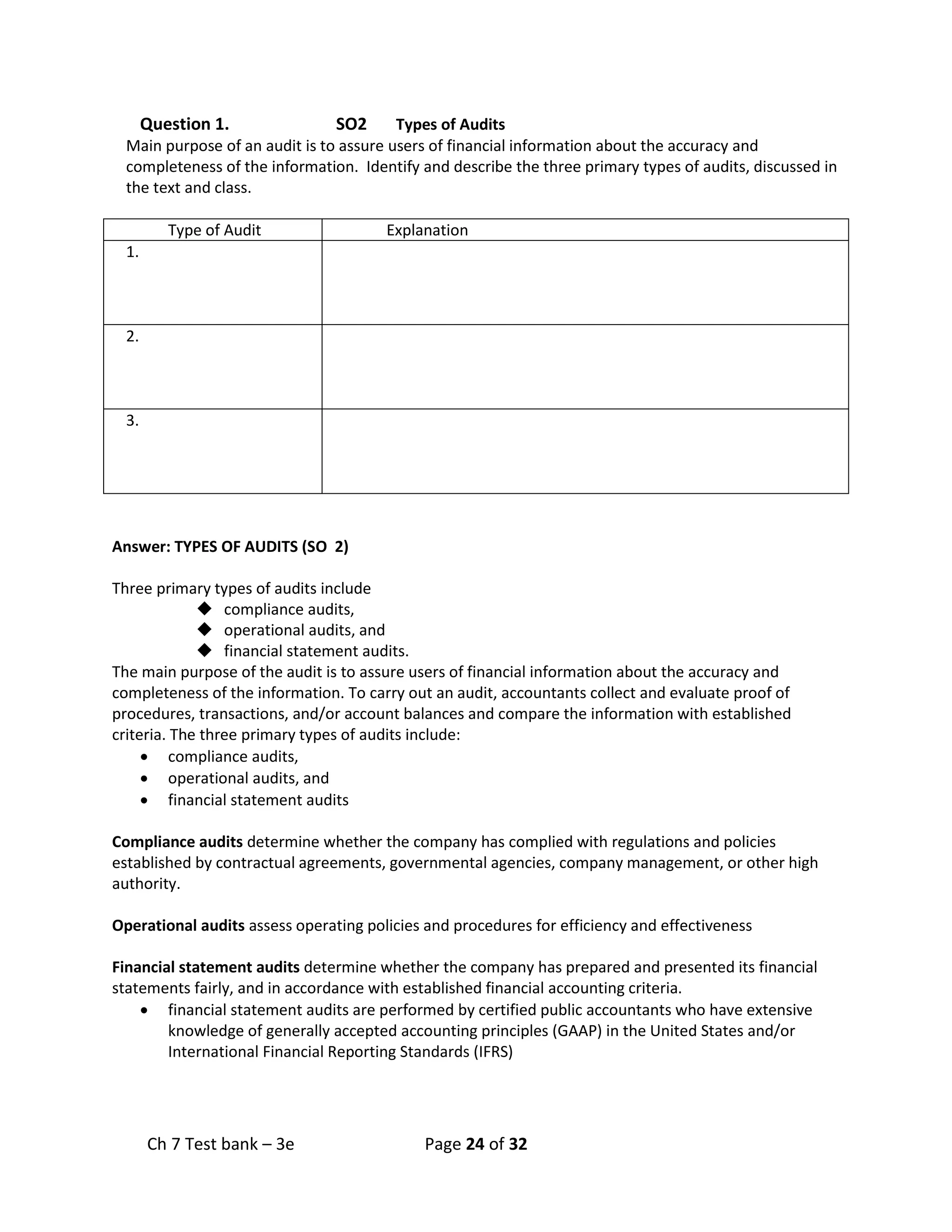

Question 1. SO2 Types of Audits

Main purpose of an audit is to assure users of financial information about the accuracy and

completeness of the information. Identify and describe the three primary types of audits, discussed in

the text and class.

Type of Audit Explanation

1.

2.

3.

Answer: TYPES OF AUDITS (SO 2)

Three primary types of audits include

◆ compliance audits,

◆ operational audits, and

◆ financial statement audits.

The main purpose of the audit is to assure users of financial information about the accuracy and

completeness of the information. To carry out an audit, accountants collect and evaluate proof of

procedures, transactions, and/or account balances and compare the information with established

criteria. The three primary types of audits include:

• compliance audits,

• operational audits, and

• financial statement audits

Compliance audits determine whether the company has complied with regulations and policies

established by contractual agreements, governmental agencies, company management, or other high

authority.

Operational audits assess operating policies and procedures for efficiency and effectiveness

Financial statement audits determine whether the company has prepared and presented its financial

statements fairly, and in accordance with established financial accounting criteria.

• financial statement audits are performed by certified public accountants who have extensive

knowledge of generally accepted accounting principles (GAAP) in the United States and/or

International Financial Reporting Standards (IFRS)

29.

Ch 7 Testbank – 3e Page 25 of 32

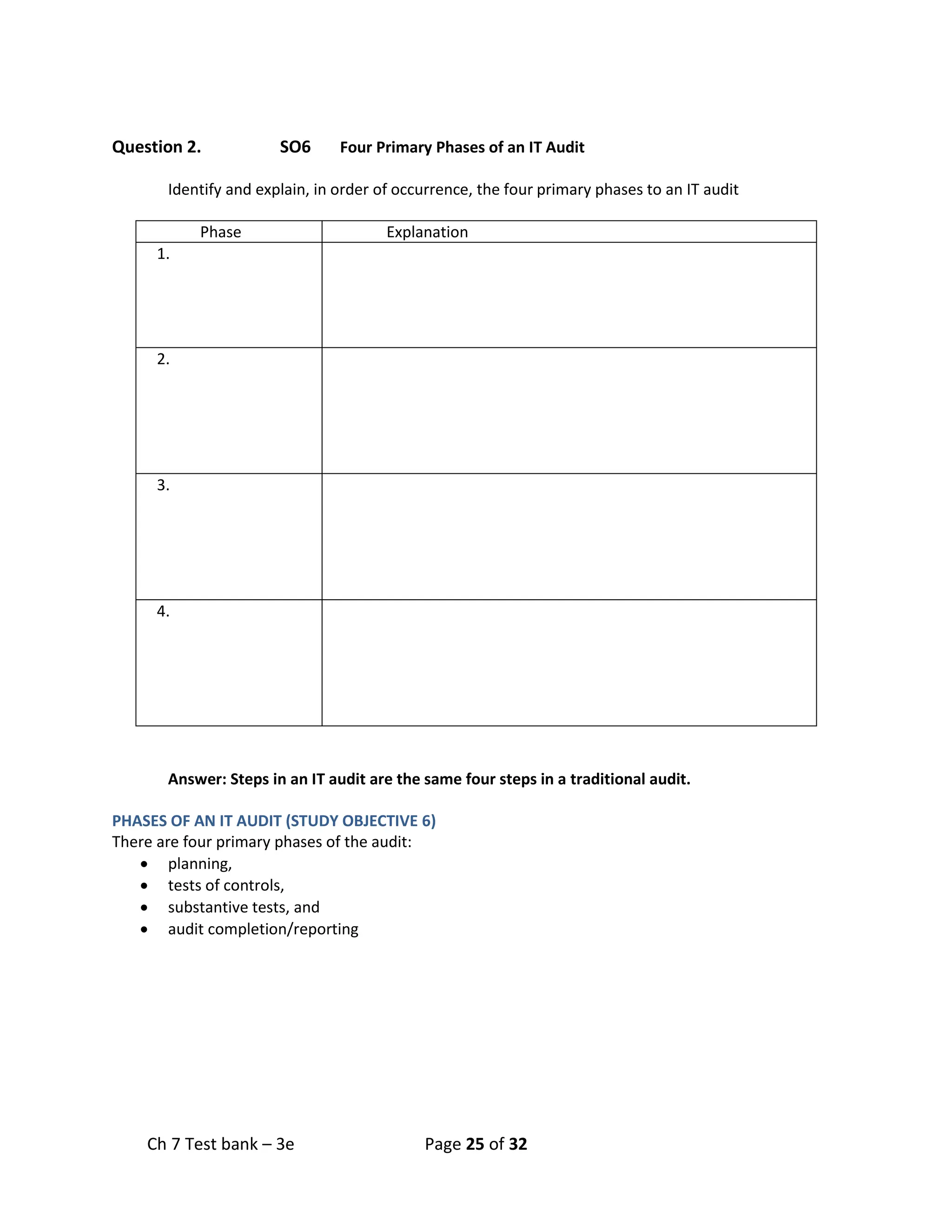

Question 2. SO6 Four Primary Phases of an IT Audit

Identify and explain, in order of occurrence, the four primary phases to an IT audit

Phase Explanation

1.

2.

3.

4.

Answer: Steps in an IT audit are the same four steps in a traditional audit.

PHASES OF AN IT AUDIT (STUDY OBJECTIVE 6)

There are four primary phases of the audit:

• planning,

• tests of controls,

• substantive tests, and

• audit completion/reporting

30.

Ch 7 Testbank – 3e Page 26 of 32

Through each phase of an audit, evidence is accumulated as a basis for supporting the conclusions

reached by the auditors. Audit evidence is proof of the fairness of financial information. The techniques

used for gathering evidence include the following:

• Physically examining or inspecting assets or supporting documentation

• Obtaining written confirmation from an independent source

• Reperforming tasks or recalculating information

• Observing the underlying activities

• Making inquiries of company personnel

• Analyzing financial relationships and making comparisons to determine reasonableness

During the planning phase of an audit, the auditor must gain a thorough under- standing of the

company’s business and financial reporting systems. In doing so, auditors review and assess the risks

and controls related to the business, establish materiality guidelines, and develop relevant tests

addressing the assertions and objectives

• tasks of assessing materiality and audit risk are very subjective and are therefore typically

performed by experienced auditors

• Determining materiality, auditors estimate the monetary amounts that are large enough to

make a difference in decision making

• Materiality estimates are then assigned to account balances so that auditors can decide how

much evidence is needed

• Below materiality limits are often considered insignificant

• Some accounts with immaterial balances may still be audited, though, especially if they are

considered areas of high risk

• Risk- refers to the likelihood that errors or fraud may occur

• Risk can be inherit or it may be caused by weak internal controls

A big part of the audit planning process is the gathering of evidence about the company’s internal

controls

• Auditors typically gain an understanding of internal controls by interviewing key members of

management and the IT staff

• They observe policies and procedures and review IT user manuals and system flowcharts

• They often prepare narratives or memos to summarize the results of their findings

• Company personnel generally complete a questionnaire about the company’s accounting

systems, including its IT implementation and operations, the types of hardware and software

used, and control of computer resources

• The understanding of internal controls provides the basis for designing appropriate audit tests

to be used in the remaining phases of the audit

TESTS OF CONTROLS (STUDY OBJECTIVE 8)

The tests of controls involve audit procedures designed to evaluate both general controls and

application controls. During audit planning, auditors must learn about the types of controls that exist

within their client’s IT environment. Then they may test those controls to determine whether they are

reliable as a means of reducing risk. Tests of controls are sometimes referred to as “compliance tests,”

because they are designed to determine whether the controls are functioning in compliance

with management’s intentions.

31.

Ch 7 Testbank – 3e Page 27 of 32

TESTS OF TRANSACTIONS AND TESTS OF BALANCES (STUDY OBJECTIVE 9)

Audit tests of the accuracy of monetary amounts of transactions and account balances are known as

substantive testing.

• Substantive tests verify whether information is correct, whereas control tests determine

whether the information is managed under a system that promotes correctness

• Some level of substantive testing is required regardless of the results of control testing.

• If weak internal controls exist or if important controls are missing, extensive substantive testing

will be required.

• If controls are found to be effective, the amount of substantive testing required is significantly

lower, because there is less chance of error in the underlying records

Most auditors use generalized audit software (GAS) or data analysis soft- ware (DAS) to perform audit

tests on electronic data files taken from commonly used database systems. These computerized auditing

tools make it possible for auditors to be much more efficient in performing routine audit tests such as

the following:

• Mathematical and statistical calculations

• Data queries

• Identification of missing items in a sequence

• Stratification and comparison of data items

• Selection of items of interest from the data files

• Summarization of testing results into a useful format for decision making

GAS and DAS are evolving to handle larger and more diverse data sets, which allow auditors to use more

types of unstructured data evidence and to perform more creative analytical procedures and predictive

analyses.

AUDIT COMPLETION/REPORTING (STUDY OBJECTIVE 10)

After the tests of controls and substantive audit tests have been completed, auditors evaluate all the

evidence that has been accumulated and draw conclusions based on this evidence. This phase is the

audit completion/reporting phase.

The completion phase includes many tasks that are needed to wrap up the audit. For many types of

audits, the most important task is obtaining a letter of representations from company management.

The letter of representations is often considered the most significant single piece of audit evidence,

because it is a signed acknowledgment of management’s responsibility for the reported information. In

this letter, management must declare that it has provided complete and accurate information to its

auditors during all phases of the audit.

Four types of reports that are issued:

1. Unqualified opinion, which states that the auditors believe the financial statements are fairly

and consistently presented in accordance with GAAP or IFRS

2. Qualified opinion, which identifies certain exceptions to an unqualified opinion

3. Adverse opinion, which notes that there are material misstatements presented

4. Disclaimer of opinion, which states that the auditors are unable to reach a conclusion.

32.

Ch 7 Testbank – 3e Page 28 of 32

Question 3. SO Primary objectives of compliance testing

The primary objective of compliance testing in a financial statement audit of a company with an

automated AIS or ERP system is to determine whether

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

The purpose of compliance testing in a financial statement audit of a company with an automated AIS or

ERP system is to determine whether internal controls are in place and functioning as designed.

Question 4. SO7 Computers User in Audits

The text identifies three ways in which computers are used in audits.

IE Auditing __________ the computer. Identify, explain and provide examples of each of the ways in

which computers are used in audits.

Way in which

used

Explanation

Auditing

____________

the computer

Auditing

____________

the computer

Auditing

____________

the computer

33.

Ch 7 Testbank – 3e Page 29 of 32

ANSWER

➢ Use of Computers in Audits. The audit planning tasks of evaluating internal controls and designing

meaningful audit tests is more complex for automated accounting systems than for manual systems.

In recognition of the fact that accounting records and files often exists in both paper and electronic

form, auditing standards address the importance of understanding both the automated and manual

procedures that make up an organization’s internal control. Misstatements may occur through the

data entry and processing functions of the system. Auditors must consider the effects of such

computer processing on the audit. Three options may exist for the auditor in deciding upon a testing

approach for a client’s automated process, including auditing around the computer, auditing

through the computer, and auditing with the computer.

• Auditing around the computer is commonly known as the “black box” approach because

auditors are not required to gain detailed knowledge about the company’s computer

system; rather, documents used to input data into the system can be compared with reports

generated from the system. Computer controls are not considered.

• Auditing through the computer is commonly known as the “white box” approach because it

involves directly testing the internal controls within the IT system. It requires the auditors to

understand the computer system logic and related IT controls. Auditing through the

computer is necessary when the auditor wants to test computer controls as a basis for

reducing the amount of substantive testing required, when the auditor is required to report

on internal controls of a public company, and when supporting documents are available only

in electronic form.

• Auditing with the computer involves the auditors’ use of their own computer systems and

audit software to perform audit testing. A variety of computer assisted audit techniques

(CAATs) are available for auditing with the computer.

USE OF COMPUTERS IN AUDITS (STUDY OBJECTIVE 7)

If the use of IT systems does not have a great impact on the conduct of the audit, since the auditor can

perform audit testing in the same manner as would be done for a manual system the practice is referred

to as auditing around the computer because it does not require evaluation of computer controls.

• Auditing around the computer merely uses and tests output of the computer system in the

same manner as the audit would be conducted if the information had been generated manually

• Because this approach does not consider the effectiveness of computer controls, auditing

around the computer has limited usefulness.

Auditing through the computer involves directly testing the internal controls within the IT system,

whereas auditing around the computer does not

• sometimes referred to as “the white box approach,” because it requires auditors to understand

the computer system logic

• This approach requires auditors to evaluate IT controls and processing so that they can

determine whether the information generated from the system is reliable

• Auditing through the computer is necessary under the following conditions:

o The auditor wants to test computer controls as a basis for evaluating risk and reducing

the amount of substantive audit testing required.

o The author is required to report on internal controls in connection with a financial

statement audit of a public company.

o Supporting documents are available only in electronic form.

34.

Ch 7 Testbank – 3e Page 30 of 32

Auditors can use their own computer systems and audit software to help conduct the audit. This

approach is known as auditing with the computer.

• A variety of computer-assisted audit techniques (CAATs) are available for auditing with the

computer

• CAATs are useful audit tools because they make it possible for auditors to use computers to test

more evidence in less time.

Question 5. SO8 Compliance and Substantive Testing

Keperlsky and Bennuchi, and audit firm was auditing EDJ consulting. EDJ is a large consulting firm

that has consistently had very strong internal controls over IT functions at the company. The

company uses SAP, a sophisticated, Tier 1 ERP system that has not been customized. Keperlsky and

Bennuchi’s audit team has reviewed and tested the internal controls and concluded that the

controls are very effective (strong) and they can be relied upon. Mr Keperlsky, a partner, has said

that it is not necessary to complete substantive testing in this case, given the strength of the internal

controls and strong ERP system. Is Mr Keperlsky’s conclusion correct?

Answer: Yes No (Circle one)

Provide justification for your answer:

_____________________________________________________________________________________

____________________________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

____________________________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

____________________________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

____________________________________________________________________________________

_____________________________________________________________________________________

Answer: No

Mr Keperlsky is not correct. It is ALWAYS necessary to complete substantive testing. Compliance

testing tests if internal controls are in place and functioning. Substantive test verify the accuracy of

financial amounts. If controls are in place and functioning, su

35.

Ch 7 Testbank – 3e Page 31 of 32

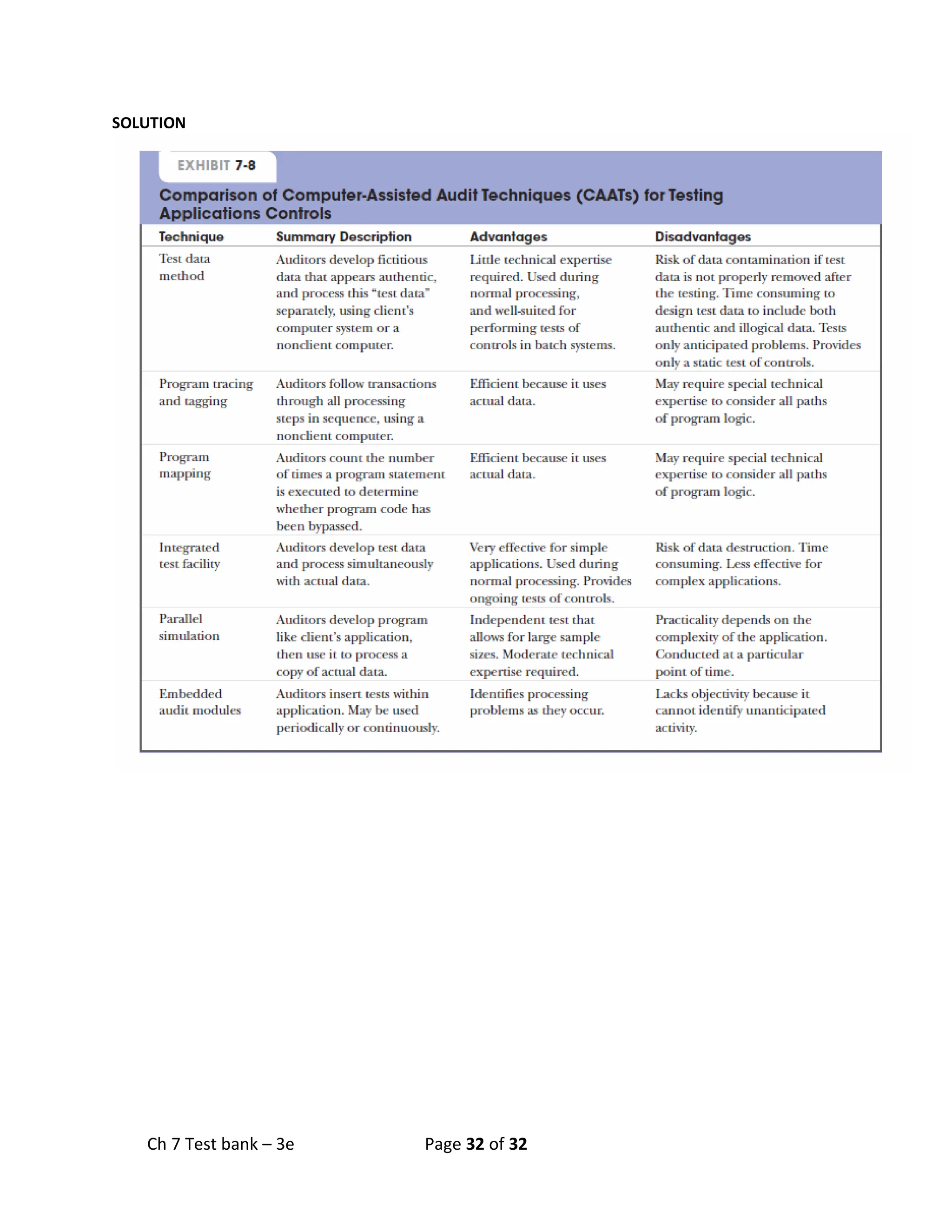

Question 6. SO7 Computer Assisted Audit Techniques (CAATs)

The text discusses several computer assisted audit techniques (CAAT’s). Lists 4 of the 5 CAAT’s and

describe the technique.

Technique Description of Computer Assisted Audit Technique

1.

2.

3.

4.

L.

Labor, division of,123 ; effect of

attempts by government to limit the

hours of, 362 Major Moody's new

philosophy of, and its refutation, 373 398

Laboring classes (the), their condition

in England and on the Continent, 178 ; in

the United States, 180

Labourdonnais, his talents, 202 ; his

treatment by the French government,

294

Laedaunon. See Sparta.

La Fontaine, allusion to, 393

Lalla Kookli, 485

Lally, Governor, his treatment by the

French government, 294

Lamb, Charles, his defence cf the

dramatists of the Restoration, 357 ; his

kind nature, 358

Lampoons, Pope's, 408

Lancaster, Dr., his patronage of

Addison, 326

Landscape gardening, 374 389

39.

Langton, Mr., hisfriendship with

Johnson, 204 219 ; his admiration of

Miss Burney, 271

Language, Drvden's command of, 367

; effect of its cultivation upon poetry, 337

338 Latin, its decadence, 55 ; its

characteristics, 55 Italian, Dante the first

to compose in, 56

Languedoc, description of it in the

twelfth century, 308 309 ; destruction of

its prosperity and literature by the

Normans, 310

Lansdowne, Lord, his friendship for

Hastings, 106

Latimer, Hugh, his popularity in

London, 423 428

Latin poems, excellence of Milton's,

211 Boileau's praise of, 342 343

Petrarch's, 96 ; language, its character

and literature, 347 349

Latinity, Croker's criticisms on, 381

Laud, Archbishop, his treatment by the

Parliament, 492 493 ; his

correspondence with Strafford, 492 ; his

character, 452 453 ; his diary, 453 ; his

impeachment and imprisonment, 468 ;

his rigor against the Puritans, and

tenderness towards the Catholics, 473

Lauderdale, Lord, 417

Laudohn, 235, 241

40.

Law, its administrationin the time of

James II., 520 ; its monstrous grievances

in India, 64 69

Lawrence, Major, his early notice of

Clive, 203, 241, ; his abilities, 203

Lawrence, Sir Thomas, 305

Laws, penal, of Elizabeth, 439 440

Lawsuit, imaginary, between the

parishes of St. Dennis and St. George-in-

the-water, 100, 111

Lawyers, their inconsistencies as

advocates and legislators, 414 415

Learning in Italy, revival of, 275 ;

causes of its decline, 278

Lebon, 483 484 503

Lee, Nathaniel, 361 362

Legerdemain, 353

Legge, Et. lion. H. B., 230 ; his return

to the Exchequer, 38 13 ; his dismissal,

28

Legislation, comparative views on, by

Plato and by Bacon, 456

Legitimacy, 237

Leibnitz, 324

Lemon, Mr., his discovery of Milton's

Treatise on Christian Doctrine, 202

41.

Lennox, Charlotte, 24

LeoX., his character, 324 ; nature of

the war between him and Luther, 327

328

Lessing, 341

Letters of Phalaris, controversy

between Sir William Temple and Christ

Church College and Bentley upon their

merits and genuineness, 108 112 114

119

Libels on the court of George III., in

Bute's time, 42

Libertinism in the time of Charles II.,

517

Liberty, public, Milton's support of, 246

; its rise and progress in Italy, 274 ; its

real nature, 395 397 ; characteristics of

English, 399 68 71 ; of the Seas,

Barrere's work upon, 512

Life, human, increase in the time of,

177

Lincoln Cathedral, painted window in,

428

Lingard, Dr., his account of the conduct

of James II. towards Lord Rochester, 307

; his ability as a historian, 41 ; his

strictures on the Triple Alliance, 42

Literary men more independent than

formerly, 190-192; their influence, 193

42.

194 ; abjectnessof their condition during

the reign of George IL, 400 401 ; their

importance to contending parties in the

reign of Queen Anne, 304 ;

encouragement afforded to, by the

Revolution, 336 ; see also Criticism,

literary.

Literature of the Roundheads, 234 ; of

the Royalists, 234 ; of the Elizabethan

age, 341 346 ; of Spain in the 16th

century, 80 ; splendid patronage of, at

the close of the 17th and beginning of

the 18th centuries, 98 ; discouragement

of, on the accession of the House of

Hanover, 98 ; importance of classical in

the 16th century, 350 Petrarch, its

votary, 86 ; what its history displays in all

languages 340 341 ; not benefited by the

French Academy, 23

Literature, German, little known in

England sixty or seventy years ago, 341

Literature, Greek, 349 353

Literature, Italian, unfavorable

influence of Petrarch upon, 59 60 ;

characteristics of, in the 14th century,

278 ; and generally, down to Alfieri, 60

Literature, Roman, 347 349

Literature, Royal Society of, 202, 9

"Little Dickey," a nickname for Norris,

the actor, 417

43.

Livy, Discourses on,by Machiavelli,

309 ; compared with Montesquieu's Spirit

of Laws, 313 314 ; his characteristics as

an historian, 402 403 ; meaning of the

expression lactece ubertus, as applied to

him, 403

Locke, 303 352

Logan, Mr., his ability in defending

Hastings, 139

Lollardism in England, 27

London, in the 17th century, 479 ;

devoted to the national cause, 480 481 ;

its public spirit, 18 ; its prosperity during

the ministry of Lord Chatham, 247 ;

conduct of, at the Restoration, 289 ;

effects of the Great Plague upon, 32 ; its

excitement on occasion of the tax on

cider proposed by Bute's ministry, 50

University of, see University.

Long Parliament (the), controversy on

its merits, 239 240 ; its first meeting,

457 ; ii.406; its early proceedings, 469

470 ; its conduct in reference to the civil

war, 471 ; its nineteen propositions, 486

; its faults, 490 494 ; censured by Mr.

Hallam, 491 ; its errors in the conduct of

the war, 494 ; treatment of it by the

army, 497 ; recapitulation of its acts, 408

; its attainder of Stratford defended, 471

; sent Hampden to Edinburgh to watch

the king, 479 ; refuses to surrender the

members ordered to be impeached, 477

44.

; openly deniesthe king, 489 ; its

conditions of reconciliation, 480

Longinus, 149 148

Lope, his distinction as a writer and a

soldier, 81

Lords, the House of, its position

previous to the Restoration, 287 ; its

condition as a debating assembly in 177

420

Lorenzo de Medici, state of Italy in his

time, 278

Lorenzo de Medici (the younger),

dedication of Machiavelli's Prince to him,

309

Loretto, plunder of, 346

Louis XI., his conduct in respect to the

Spanish succession, 80 99 ; his

acknowledgment, on the death of James

II., of the Prince of Wales as King of

England, and its consequences, 102 ;

sent an army into Spain to the assistance

of his grandson, 109 ; his proceedings in

support of his grandson Philip, 109 127 ;

his reverses in Germany, Italy, and the

Netherlands, 129 ; his policy, 309 ;

character of his government, 308 311 ;

his military exploits, 5 ; his projects and

affected moderation, 36 ; his ill-humor at

the Triple Alliance, 41 ; his conquest of

Franche Comte, 42 ; his treaty with

Charles, 53 ; the early part of his reign a

45.

time of license,364 ; his devotion, 339 ;

his late regret for his extravagance, 39 ;

his character and person, 576 ; his

injurious influence upon religion, 64

Louis XV., his government, 646 6 293

Louis XVI., 441 ; to: 449 455 150 67

Louis XVIII., restoration of, compared

with that of Charles II., 282 ; seq.

Louisburg, fall of, 244

L'Ouverture, Toussaint, 366 390 392

Love, superiority of the. Romans over

the Greeks in their delineations of, 83 ;

change in the nature of the passion of,

84 ; earned by the introduction of the

Northern element, 83

"Love for Love," by Congreve, 392 ; its

moral, 402

"Love in a Wood," when acted, 371

Loyola, his energy, 320 336

Lucan, Dryden's resemblance to, 355

Lucian, 387

Luther, his declaration against the

ancient philosophy, 446 ; sketch of the

contest which began with his preaching

against the Indulgences and terminated

with the treaty of Westphalia, 314 338 ;

was the product of his age, 323 ;

defence of, by Atterbury, 113

M.

Maebomey, original nameof the

Burney family, 250 Machiavelli, his

works, by Périer, 267 ; general

odiousness of his name and works, 268

269 ; suffered for public liberty, 269 ; his

elevated sentiments and just views, 270

; held in high estimation by his

contemporaries. 271 ; state of moral

feeling ill Italy in his time, 272 ; his

character as a man, 291 ; as a poet, 293

; as a dramatist, 296 ; as a statesman,

291 300 309 313 309 ; excellence of his

precepts, 311 ; his candor, 313 ;

comparison between him and

Montesquieu, 314 ; his style, 314 ; his

levity, 316 ; his historical works, 316 ;

lived to witness the last struggle for

Florentine liberty, 319 ; his works and

character misrepresented, 319 ; his

remains dishonored till long after his

death, 319 ; monument erected to his

memory by an English nobleman, 319

Mackenzie, Henry, his ridicule of the

Nabob class, 283

Mackenzie, Mr., his dismissal insisted

on by Grenville, 70

Mackintosh, Sir James, review of his

History of the Revolution in England, 251

48.

335 ; comparisonwith Fox's History of

James II., 252 ; character of his oratory,

253 ; his conversational powers, 256 ;

his qualities as an historian, 250 ; his

vindication from the imputations of the

editor, 262 270-278; change in his

opinions produced by the French

Revolution, 263 ; his moderation, 268

270 ; his historical justice, 277 278 ;

remembrance of him at Holland House,

425

Macleane, Colonel, agent in England

for Warren Hastings, 44 53

Macpherson, James, 77 331 210 ; a

favorite author with Napoleon, 515 ;

despised by Johnson, 116

Madras, description of it, 199 ; its

capitulation to the French, 202 ; restored

to the English, 203