1. A valuation on Facebook.

(Juan J. Romero, Sydney, Nov 2012)

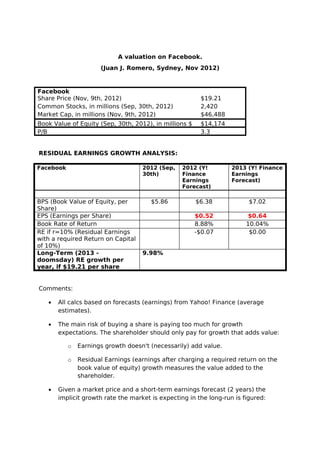

Facebook

Share Price (Nov, 9th, 2012) $19.21

Common Stocks, in millions (Sep, 30th, 2012) 2,420

Market Cap, in millions (Nov, 9th, 2012) $46,488

Book Value of Equity (Sep, 30th, 2012), in millions $ $14,174

P/B 3.3

RESIDUAL EARNINGS GROWTH ANALYSIS:

Facebook 2012 (Sep, 2012 (Y! 2013 (Y! Finance

30th) Finance Earnings

Earnings Forecast)

Forecast)

BPS (Book Value of Equity, per $5.86 $6.38 $7.02

Share)

EPS (Earnings per Share) $0.52 $0.64

Book Rate of Return 8.88% 10.04%

RE if r=10% (Residual Earnings -$0.07 $0.00

with a required Return on Capital

of 10%)

Long-Term (2013 - 9.98%

doomsday) RE growth per

year, if $19.21 per share

Comments:

• All calcs based on forecasts (earnings) from Yahoo! Finance (average

estimates).

• The main risk of buying a share is paying too much for growth

expectations. The shareholder should only pay for growth that adds value:

o Earnings growth doesn't (necessarily) add value.

o Residual Earnings (earnings after charging a required return on the

book value of equity) growth measures the value added to the

shareholder.

• Given a market price and a short-term earnings forecast (2 years) the

implicit growth rate the market is expecting in the long-run is figured:

2. o If you buy today, $19.21 a share, you would expect residual

earnings growing at 9.98% per year, since 2013 till doomsday.

o Is that growth rate “reasonable”? → Benchmark.

Benchmark:

• Google:

o Trading at $663 a share, with a $39.82 forecasted EPS (2012) and

$46.39 (2013) should increase residual earnings 5.51% each year in

the long-run.

o If this growth rate is applied to Facebook the valuation’s outcome is

$5.84 a share. Facebook would be a 230% overpriced using this

benchmark.

• Why using Google as benchmark?

o Consolidated firm, same industry.

o All competitive advantage yielding high growth rates will be eroded

by competitors over the years. Consolidated companies in the same

industry can be used as a “reference” for valuation purposes.

o The market is expecting that Google will sustain a growth rate, in

the long-run, pretty similar to a standard GDP growth rate (2.5-5%).

Sounds reasonable to me!

• Finally:

o The required return on the book value applied in both cases was the

same (10%). Google is a more diversified company than Facebook,

so its business risk is lower, and so its required return on the book

value. The applied required return on Facebook should be higher. If

so, the share would be even more overpriced.

o With Google's growth rate, Facebook's market capitalization would

be even less, today, than its book value of the Equity!