Lundin Gold April 2024 Corporate Presentation v4.pdf

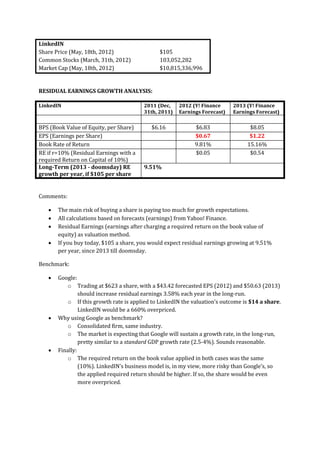

LinkedIN

1. LinkedIN

Share Price (May, 18th, 2012) $105

Common Stocks (March, 31th, 2012) 103,052,282

Market Cap (May, 18th, 2012) $10,815,336,996

RESIDUAL EARNINGS GROWTH ANALYSIS:

LinkedIN 2011 (Dec, 2012 (Y! Finance 2013 (Y! Finance

31th, 2011) Earnings Forecast) Earnings Forecast)

BPS (Book Value of Equity, per Share) $6.16 $6.83 $8.05

EPS (Earnings per Share) $0.67 $1.22

Book Rate of Return 9.81% 15.16%

RE if r=10% (Residual Earnings with a $0.05 $0.54

required Return on Capital of 10%)

Long-Term (2013 - doomsday) RE 9.51%

growth per year, if $105 per share

Comments:

The main risk of buying a share is paying too much for growth expectations.

All calculations based on forecasts (earnings) from Yahoo! Finance.

Residual Earnings (earnings after charging a required return on the book value of

equity) as valuation method.

If you buy today, $105 a share, you would expect residual earnings growing at 9.51%

per year, since 2013 till doomsday.

Benchmark:

Google:

o Trading at $623 a share, with a $43.42 forecasted EPS (2012) and $50.63 (2013)

should increase residual earnings 3.58% each year in the long-run.

o If this growth rate is applied to LinkedIN the valuation’s outcome is $14 a share.

LinkedIN would be a 660% overpriced.

Why using Google as benchmark?

o Consolidated firm, same industry.

o The market is expecting that Google will sustain a growth rate, in the long-run,

pretty similar to a standard GDP growth rate (2.5-4%). Sounds reasonable.

Finally:

o The required return on the book value applied in both cases was the same

(10%). LinkedIN’s business model is, in my view, more risky than Google’s, so

the applied required return should be higher. If so, the share would be even

more overpriced.