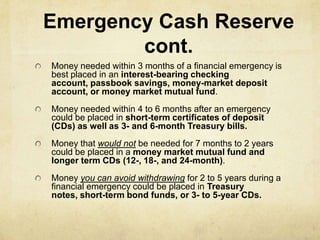

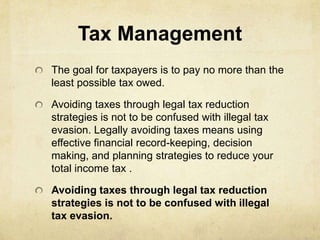

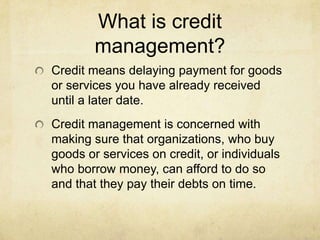

The document discusses various financial concepts related to investing, saving, and wealth management. It defines the differences between saving and investing, with saving focusing on short-term goals and emergencies while investing aims for long-term growth. It also covers risk management strategies like diversification and dollar cost averaging. Additional topics include cash management, tax planning, credit management, home ownership, retirement planning, and considerations for further education. The document provides information to help readers make informed financial decisions.

![Fundamentals of Investing[1]](https://cdn.slidesharecdn.com/ss_thumbnails/8af04f42-a488-45c7-a9db-b39152b2a985-150211040936-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)