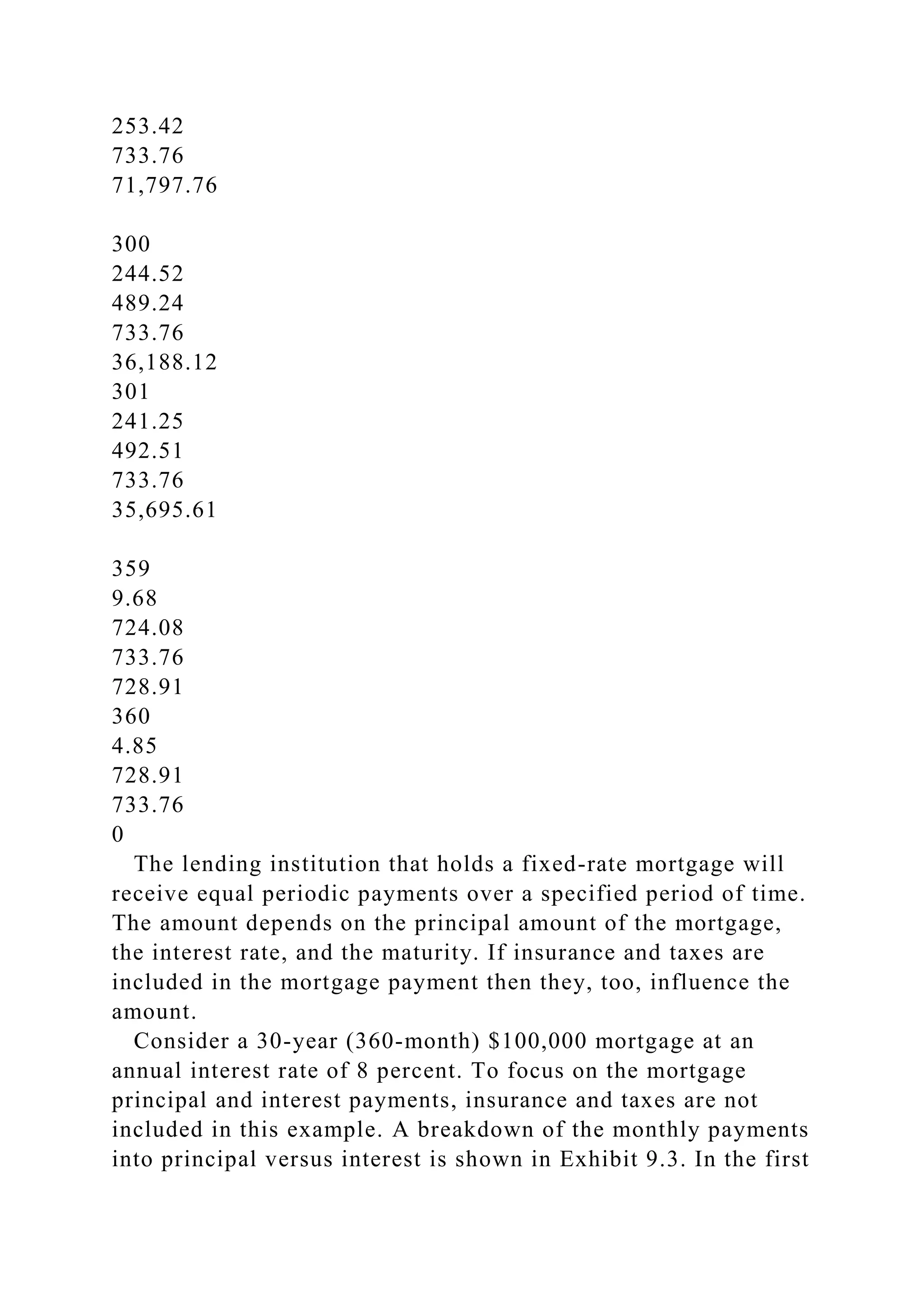

The document provides a comprehensive overview of mortgage markets, detailing the types of residential mortgages, the role of financial institutions, and the criteria for assessing borrower creditworthiness. It explains various mortgage classifications, including prime versus subprime, and insured versus conventional mortgages, as well as the functions of adjustable-rate, fixed-rate, and other specialized mortgage types. Additionally, the document discusses the relationship between mortgage valuation and market risks, especially in the context of the 2008-2009 credit crisis.

![recent issue of the Wall Street Journal to determine the

Treasury bond yield. How do these rates compare to the Fannie

Mae yield quoted in the Journal's “Borrowing Benchmarks”

section? Why do you think there is a difference between the

Fannie Mae rate and Treasury bond yields?

ONLINE ARTICLES WITH REAL-WORLD EXAMPLES

Find a recent practical article available online that describes a

real-world example regarding a specific financial institution or

financial market that reinforces one or more concepts covered in

this chapter.

If your class has an online component, your professor may ask

you to post your summary of the article there and provide a link

to the article so that other students can access it. If your class is

live, your professor may ask you to summarize your application

of the article in class. Your professor may assign specific

students to complete this assignment or may allow any students

to do the assignment on a volunteer basis.

For recent online articles and real-world examples related to

this chapter, consider using the following search terms (be sure

to include the prevailing year as a search term to ensure that the

online articles are recent):

· 1. subprime mortgages AND risk

· 2. adjustable-rate mortgage AND risk

· 3. balloon-payment mortgage AND risk

· 4. mortgage AND credit risk

· 5. mortgage AND prepayment risk

· 6. [name of a specific financial institution] AND mortgage

· 7. credit crisis AND mortgage

· 8. mortgage-backed securities AND default

· 9. credit crisis AND Fannie Mae

· 10. credit crisis AND Freddie Mac

PART 3 INTEGRATIVE PROBLEM: Asset Allocation

This problem requires an understanding of how economic

conditions influence interest rates and security prices (Chapters

6, 7, 8, and 9).

As a personal financial planner, one of your tasks is to prescribe](https://image.slidesharecdn.com/9mortgagemarketschapterobjectivesthespecificobjectivesof-221013163509-24118fb8/75/9-Mortgage-MarketsCHAPTER-OBJECTIVESThe-specific-objectives-of-docx-38-2048.jpg)

![example, the percentage change in price for Bond X for an

increase in yield of 0.2 percentage point would be

Thus, according to the modified duration estimate, if interest

rates rise by 0.2 percentage point then the price of Bond X will

drop 1.45 percent. Similarly, if interest rates decrease by 0.2

percentage point, the price of Bond X will increase by 1.45

percent.

Estimation Errors from Using Modified Duration If investors

rely strictly on modified duration to estimate the percentage

change in the price of a bond, they will tend to overestimate the

price decline associated with an increase in rates and to

underestimate the price increase associated with a decrease in

rates.

EXAMPLE

Consider a bond with a 10 percent coupon that pays interest

annually and has 20 years to maturity. If the required rate of

return is 10 percent (the same as the coupon rate), the value of

the bond is $1,000. Based on the formula provided earlier, this

bond's modified duration is 8.514 years. If investors anticipate

that bond yields will increase by 1 percentage point (to 11

percent), then they can estimate the percentage change in the

bond's price to be

If bond yields rise by 1 percentage point as expected, the

price (present value) of the bond would now be $920.37. (Verify

this new price by using the time value function on your

financial calculator.) The new price reflects a decline of 7.96

percent [calculated as ($920.37 − $1,000) ÷ $1,000]. The

decline in price is Less pronounced than was estimated in the

previous equation. The difference between the estimated

percentage change in price (8.514 percent) and the actual

percentage change in price (7.96 percent) is due to convexity.

Bond Convexity A more complete formula to estimate the

percentage change in price in response to a change in yield will

incorporate the property of convexity as well as modified](https://image.slidesharecdn.com/9mortgagemarketschapterobjectivesthespecificobjectivesof-221013163509-24118fb8/75/9-Mortgage-MarketsCHAPTER-OBJECTIVESThe-specific-objectives-of-docx-60-2048.jpg)

![bonds. Compare that premium to the premium that existed one

month ago. Did the premium increase or decrease? Offer an

explanation for the change. Is the change attributed to economic

conditions?

WSJ EXERCISE

Impact of Treasury Financing on Bond Prices

The Treasury periodically issues new bonds to finance the

deficit. Review recent issues of the Wall Street Journal or check

related online news to find a recent article on such financing.

Does the article suggest that financial markets are expecting

upward pressure on interest rates as a result of the Treasury

financing? What happened to prices of existing bonds when the

Treasury announced its intentions to issue new bonds?

ONLINE ARTICLES WITH REAL-WORLD EXAMPLES

Find a recent practical article available online that describes a

real-world example regarding a specific financial institution or

financial market that reinforces one or more concepts covered in

this chapter.

If your class has an online component, your professor may ask

you to post your summary of the article there and provide a link

to the article so that other students can access it. If your class is

live, your professor may ask you to summarize your application

of the article in class. Your professor may assign specific

students to complete this assignment or may allow any students

to do the assignment on a volunteer basis.

For recent online articles and real-world examples related to

this chapter, consider using the following search terms (be sure

to include the prevailing year as a search term to ensure that the

online articles are recent):

· 1. Treasury bond AND yield

· 2. Treasury bond AND return

· 3. bond AND federal agency

· 4. stripped Treasury bond

· 5. inflation-indexed Treasury bond

· 6. municipal bond AND risk

· 7. [name of a specific financial institution] AND bond](https://image.slidesharecdn.com/9mortgagemarketschapterobjectivesthespecificobjectivesof-221013163509-24118fb8/75/9-Mortgage-MarketsCHAPTER-OBJECTIVESThe-specific-objectives-of-docx-133-2048.jpg)

![Assessing Yield Differentials of Money Market Securities

Use the “Money Rates” section of the Wall Street Journal to

determine the 30-day yield (annualized) of commercial paper,

certificates of deposit, banker's acceptances, and T-bills. Which

of these securities has the highest yield? Why? Which of these

securities has the lowest yield? Why?

ONLINE ARTICLES WITH REAL-WORLD EXAMPLES

Find a recent practical article available online that describes a

real-world example regarding a specific financial institution or

financial market that reinforces one or more concepts covered in

this chapter. If your class has an online component, your

professor may ask you to post your summary of the article there

and provide a link to the article so that other students can

access it. If your class is live, your professor may ask you to

summarize your application of the article in class. Your

professor may assign specific students to complete this

assignment or may allow any students to do the assignment on a

volunteer basis.

For recent online articles and real-world examples related to

this chapter, consider using the following search terms (be sure

to include the prevailing year as a search term to ensure that the

online articles are recent):

· 1. Treasury bill auction

· 2. commercial paper AND offering

· 3. commercial paper AND rating

· 4. repurchase agreement AND financing

· 5. money market AND yield

· 6. commercial paper AND risk

· 7. institutional investors AND money market

· 8. banker's acceptance AND yield

· 9. [name of a specific financial institution] AND repurchase

agreement

· 10. [name of a specific financial institution] AND commercial

paper](https://image.slidesharecdn.com/9mortgagemarketschapterobjectivesthespecificobjectivesof-221013163509-24118fb8/75/9-Mortgage-MarketsCHAPTER-OBJECTIVESThe-specific-objectives-of-docx-175-2048.jpg)