7.1 Types ofestimates and their specific uses

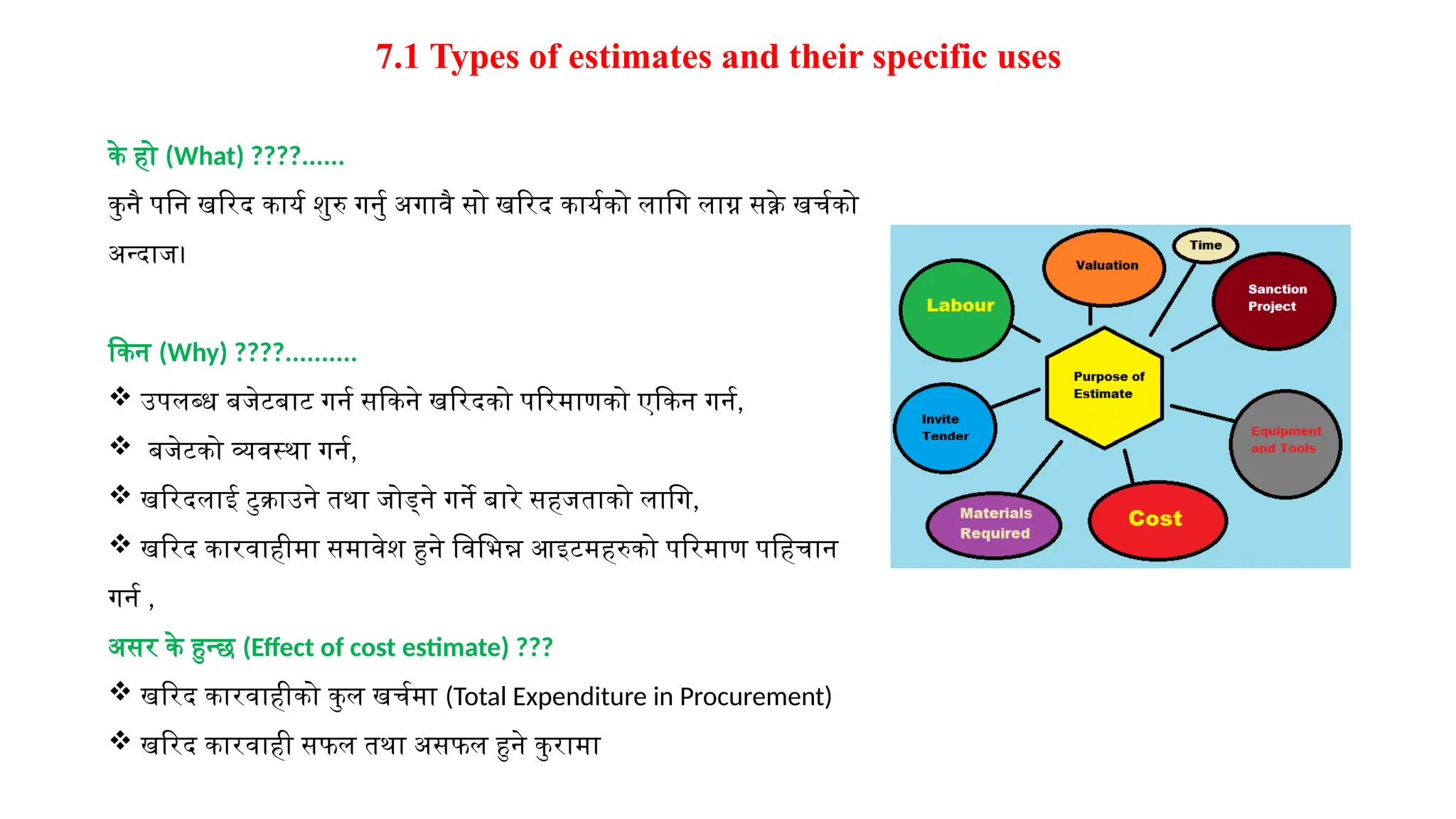

के हो (What) ????......

कुनै पनि खरिद कार्य शुरु गर्नु अगावै सो खरिद कार्यको लागि लाग्न सक्ने खर्चको

अन्दाज।

किन (Why) ????..........

उपलब्ध बजेटबाट गर्न सकिने खरिदको परिमाणको एकिन गर्न,

बजेटको व्यवस्था गर्न,

खरिदलाई टुक्राउने तथा जोड्ने गर्ने बारे सहजताको लागि,

खरिद कारवाहीमा समावेश हुने विभिन्न आइटमहरुको परिमाण पहिचान

गर्न ,

असर के हुन्छ (Effect of cost estimate) ???

खरिद कारवाहीको कुल खर्चमा (Total Expenditure in Procurement)

खरिद कारवाही सफल तथा असफल हुने कुरामा

5.

7.1 Types ofestimates and their specific uses

Estimate

It is the calculation of quantities of various items of work and expenses likely to be incurred there on of a

particular work/project.

सार्वजनिक खरिद ऐन, २०६३ को दफा ५ अनुसार सार्वजनिक निकायले कुनै पनि खरिदको लागि लागत अनुमान तयार गर्नु पर्ने

व्यवस्था रहेको

निर्माण कार्यको हकमा बाहेक एक लाख रुपैयाँसम्मको खरिद गर्न लागत अनुमान गर्नु नपर्ने।

लागत अनुमान तयार पार्नुको उद्देश्य

उपलब्ध बजेटबाट गर्न सकिने खरिदको परिमाणको एकिन गर्न।

खरिद विधि चयन गर्न।

खरिदको Slicing तथा Packaging गर्ने बारे सहजताको लागि।

खरिद कारवाहीमा समावेश हुने विभिन्न Item हरुको परिमाण पहिचान गर्न।

6.

7.1 Types ofestimates and their specific uses

Estimate Purposes

To give concise idea of cost of project/work

Estimation of various types and quantities of materials requirement

Estimation of various types and members of labours

Estimation various types of tools and plants

Estimation of time of completion

Estimation of value of project

Facilitate for invitation of tender and preparation of bills payment

Preparation of work schedule

Determination of financial viability (BCR,IRR,PBP)/Feasibility study

7.

7.1 Types ofestimates and their specific uses

Data Requirement for Estimating

• Drawings: A fully dimensioned working drawing is essential for estimation.

• Norms for Rate analysis/Schedules of rates: Government approved Norms/rates is essential.

• Specification: General and detailed specification

• Method of Measurement: Nepal Standard-389-2054

8.

7.1 Types ofestimates and their specific uses

Principle of Units of Measurement

Mass, voluminous and thick works shall be taken in Cum (m3) like Earth work and brick work.

Thin, shallow and surface works shall be taken in Sqm (m2) like DPC, Plaster, shutters etc.

Long and thin works shall be taken in Running Meter (Rm) like road, skirting, handrail etc.

Piece work or job work shall be taken in number like wash basin, tube light etc.

Dimension shall be measured to nearest 0.01m except thickness of slab or R.C slab shall be measured to

nearest 0.005m, woodwork to nearest 0.002m, steelwork to nearest 0.001m & reinforcement to nearest 0.005m

Area shall be measured to nearest 0.01 sqm

Volume shall be measured to nearest 0.01cum except wood work is measured to nearest 0.001cum.

Weight shall be measured to nearest 1kg.

9.

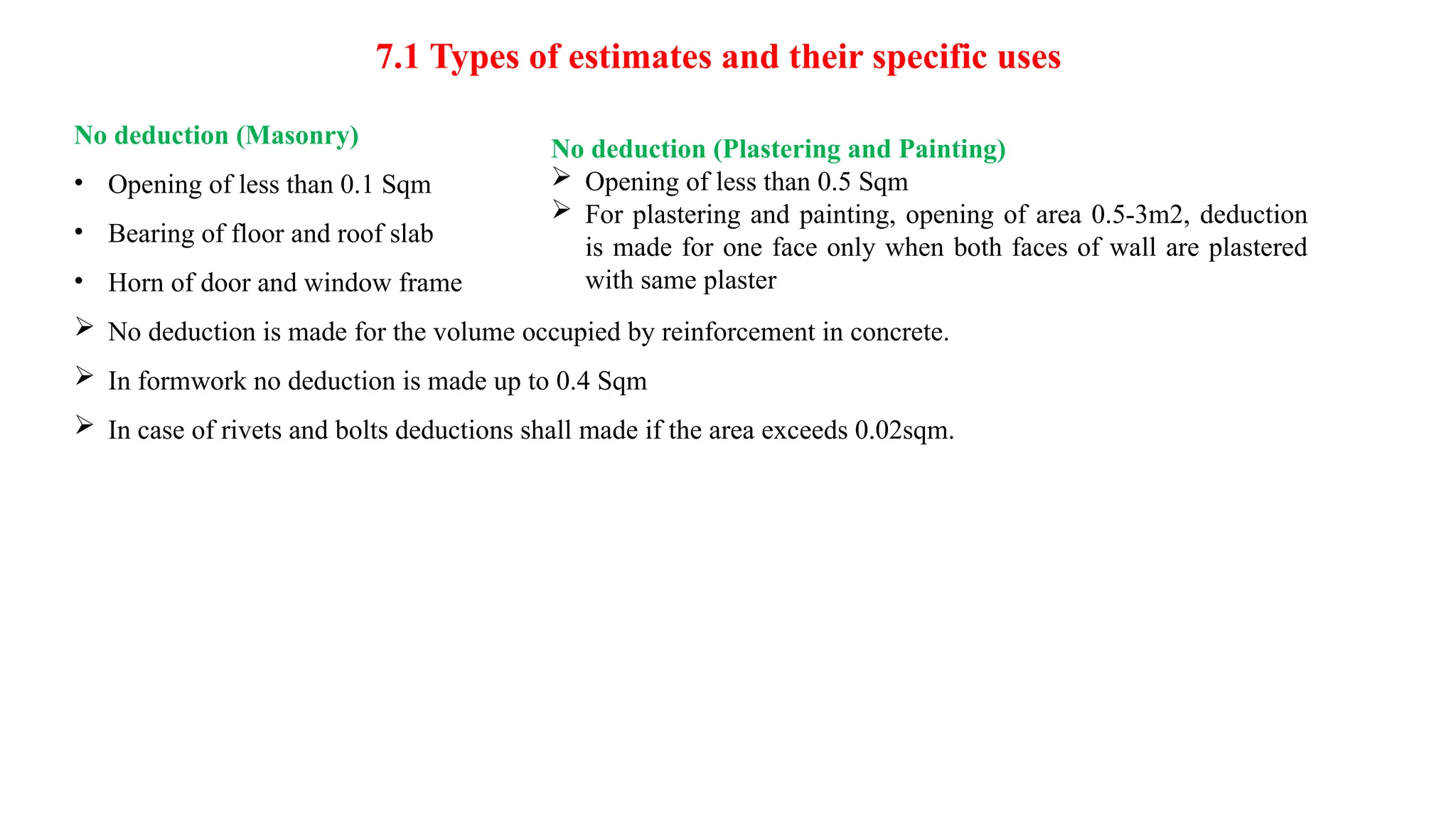

7.1 Types ofestimates and their specific uses

No deduction (Masonry)

• Opening of less than 0.1 Sqm

• Bearing of floor and roof slab

• Horn of door and window frame

No deduction is made for the volume occupied by reinforcement in concrete.

In formwork no deduction is made up to 0.4 Sqm

In case of rivets and bolts deductions shall made if the area exceeds 0.02sqm.

No deduction (Plastering and Painting)

Opening of less than 0.5 Sqm

For plastering and painting, opening of area 0.5-3m2, deduction

is made for one face only when both faces of wall are plastered

with same plaster

10.

Types of estimatesand their specific uses

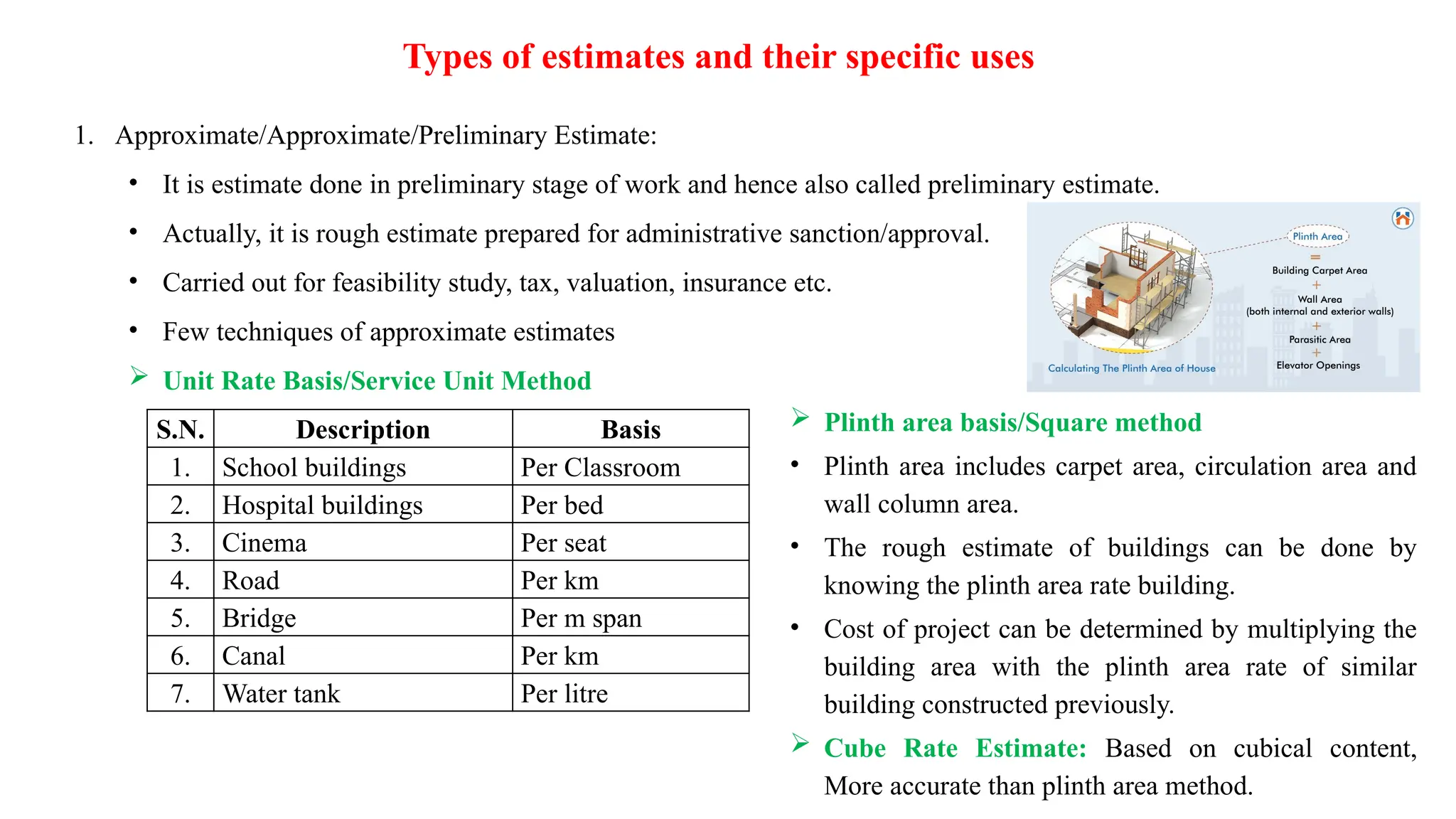

1. Approximate/Approximate/Preliminary Estimate:

• It is estimate done in preliminary stage of work and hence also called preliminary estimate.

• Actually, it is rough estimate prepared for administrative sanction/approval.

• Carried out for feasibility study, tax, valuation, insurance etc.

• Few techniques of approximate estimates

Unit Rate Basis/Service Unit Method

S.N. Description Basis

1. School buildings Per Classroom

2. Hospital buildings Per bed

3. Cinema Per seat

4. Road Per km

5. Bridge Per m span

6. Canal Per km

7. Water tank Per litre

Plinth area basis/Square method

• Plinth area includes carpet area, circulation area and

wall column area.

• The rough estimate of buildings can be done by

knowing the plinth area rate building.

• Cost of project can be determined by multiplying the

building area with the plinth area rate of similar

building constructed previously.

Cube Rate Estimate: Based on cubical content,

More accurate than plinth area method.

11.

Types of estimatesand their specific uses

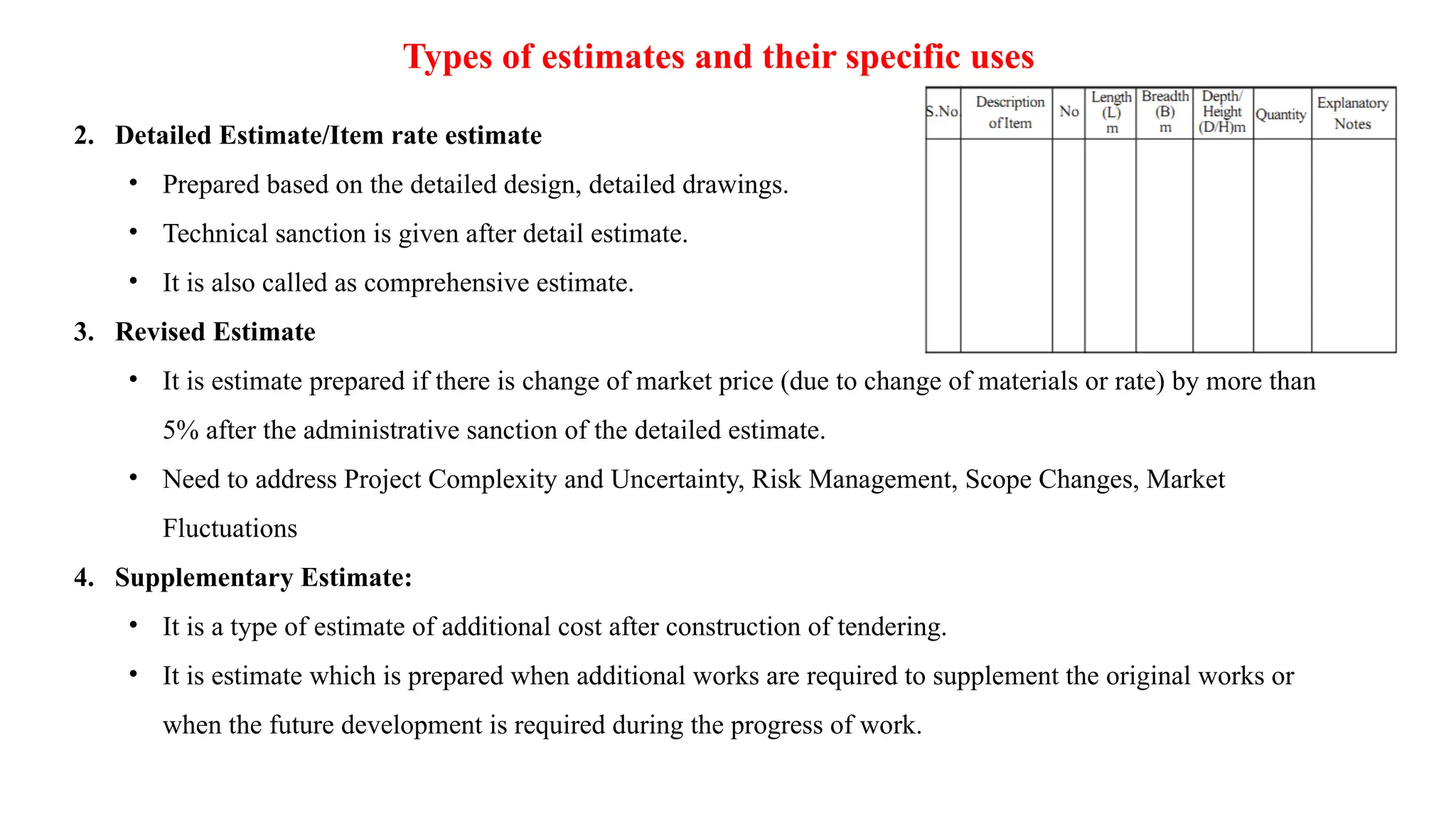

2. Detailed Estimate/Item rate estimate

• Prepared based on the detailed design, detailed drawings.

• Technical sanction is given after detail estimate.

• It is also called as comprehensive estimate.

3. Revised Estimate

• It is estimate prepared if there is change of market price (due to change of materials or rate) by more than

5% after the administrative sanction of the detailed estimate.

• Need to address Project Complexity and Uncertainty, Risk Management, Scope Changes, Market

Fluctuations

4. Supplementary Estimate:

• It is a type of estimate of additional cost after construction of tendering.

• It is estimate which is prepared when additional works are required to supplement the original works or

when the future development is required during the progress of work.

12.

Types of estimatesand their specific uses

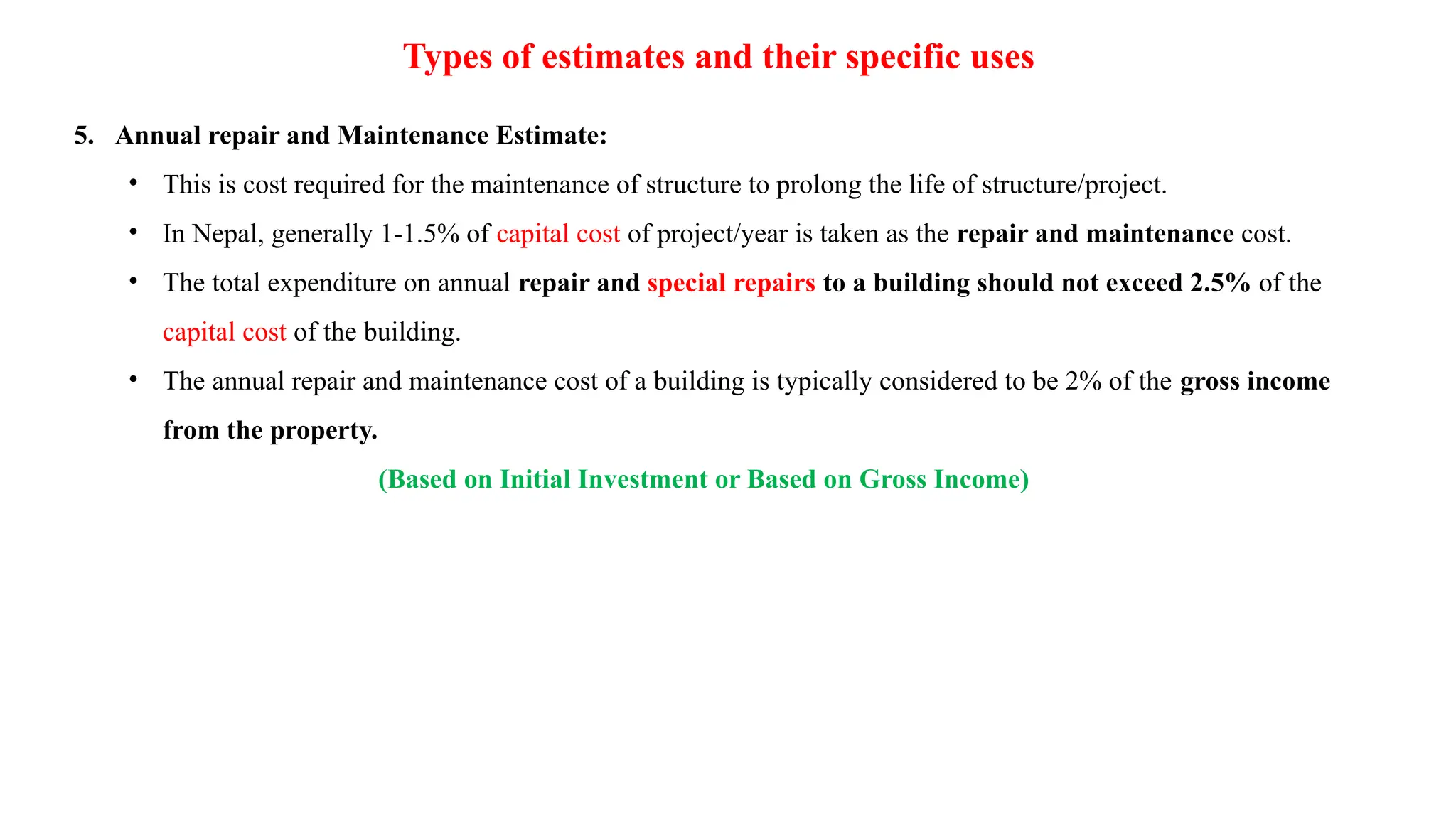

5. Annual repair and Maintenance Estimate:

• This is cost required for the maintenance of structure to prolong the life of structure/project.

• In Nepal, generally 1-1.5% of capital cost of project/year is taken as the repair and maintenance cost.

• The total expenditure on annual repair and special repairs to a building should not exceed 2.5% of the

capital cost of the building.

• The annual repair and maintenance cost of a building is typically considered to be 2% of the gross income

from the property.

(Based on Initial Investment or Based on Gross Income)

13.

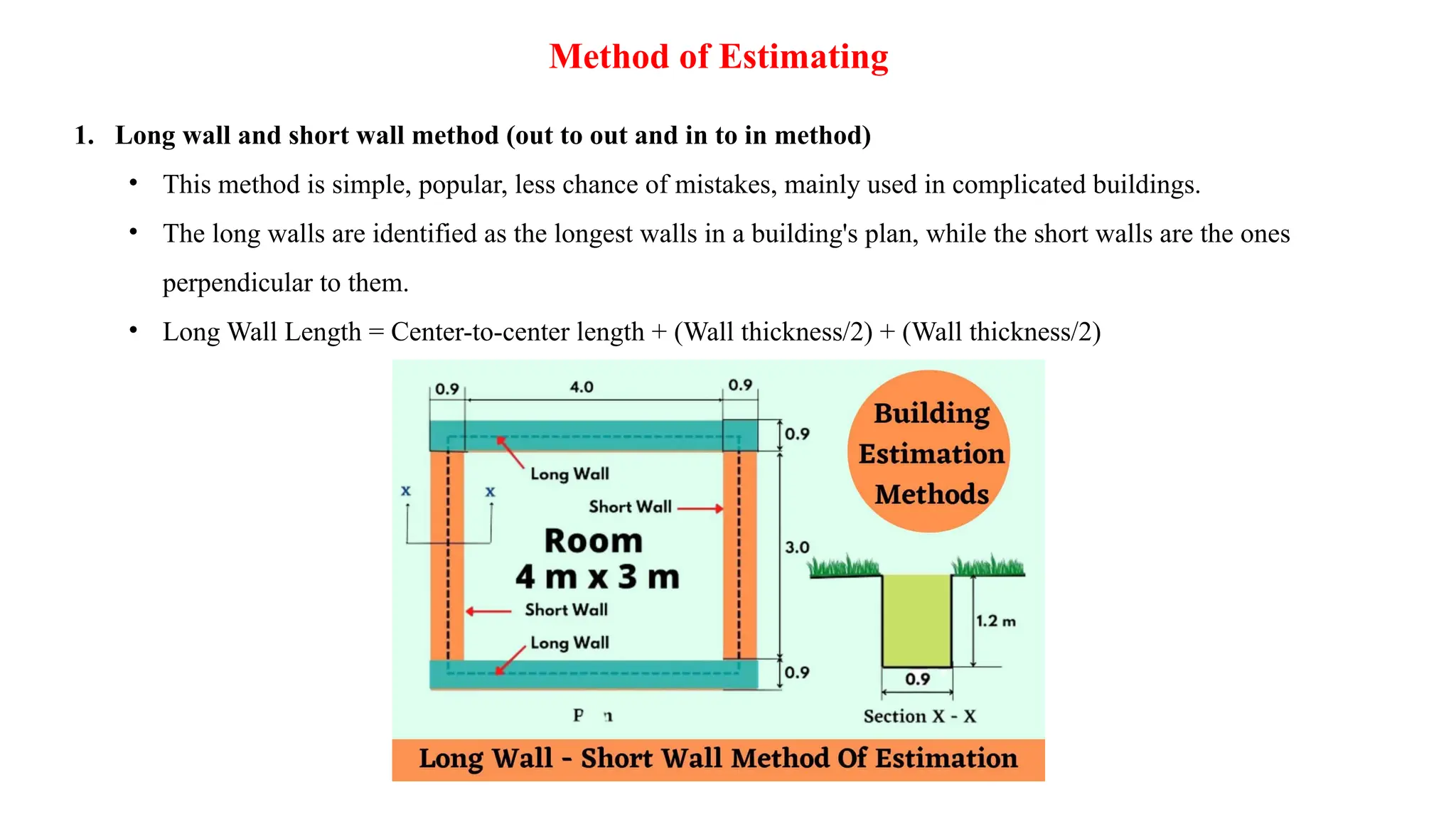

Method of Estimating

1.Long wall and short wall method (out to out and in to in method)

• This method is simple, popular, less chance of mistakes, mainly used in complicated buildings.

• The long walls are identified as the longest walls in a building's plan, while the short walls are the ones

perpendicular to them.

• Long Wall Length = Center-to-center length + (Wall thickness/2) + (Wall thickness/2)

14.

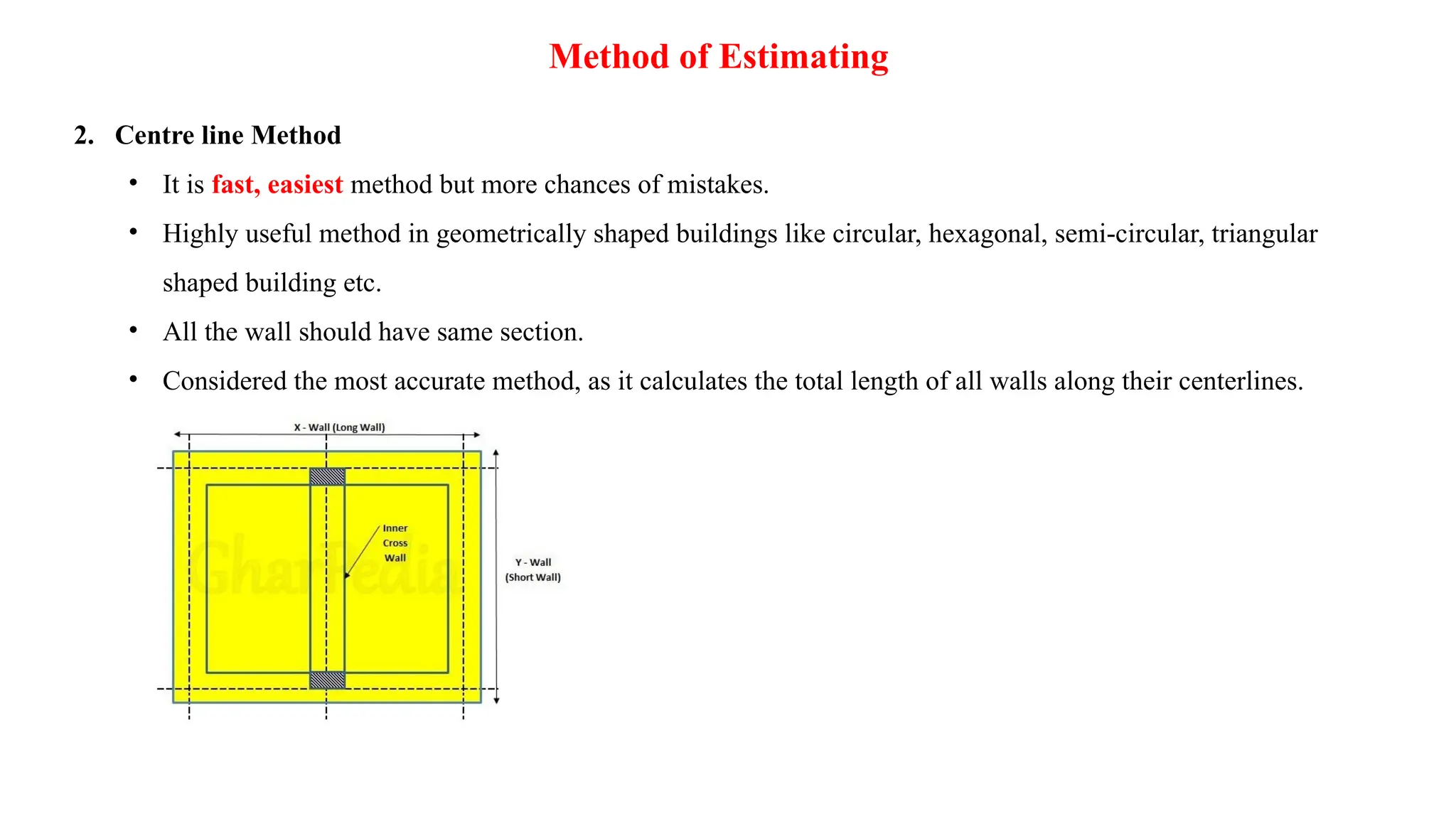

Method of Estimating

2.Centre line Method

• It is fast, easiest method but more chances of mistakes.

• Highly useful method in geometrically shaped buildings like circular, hexagonal, semi-circular, triangular

shaped building etc.

• All the wall should have same section.

• Considered the most accurate method, as it calculates the total length of all walls along their centerlines.

15.

Method of Estimating

3.Crossing Method

• This method is applicable if offsets are more or less symmetrical.

• The centerline method calculates the total length of all walls by adding their centerlines, with adjustments

for junctions, while the crossing method is a combination that uses the centerline method for external

walls and the long wall-short wall method for internal walls.

4. Bay method

• This method is suitable if the building has number of bays.

• The quantities for single bay is calculated and total quantity is calculated by multiplying with number of

bays

16.

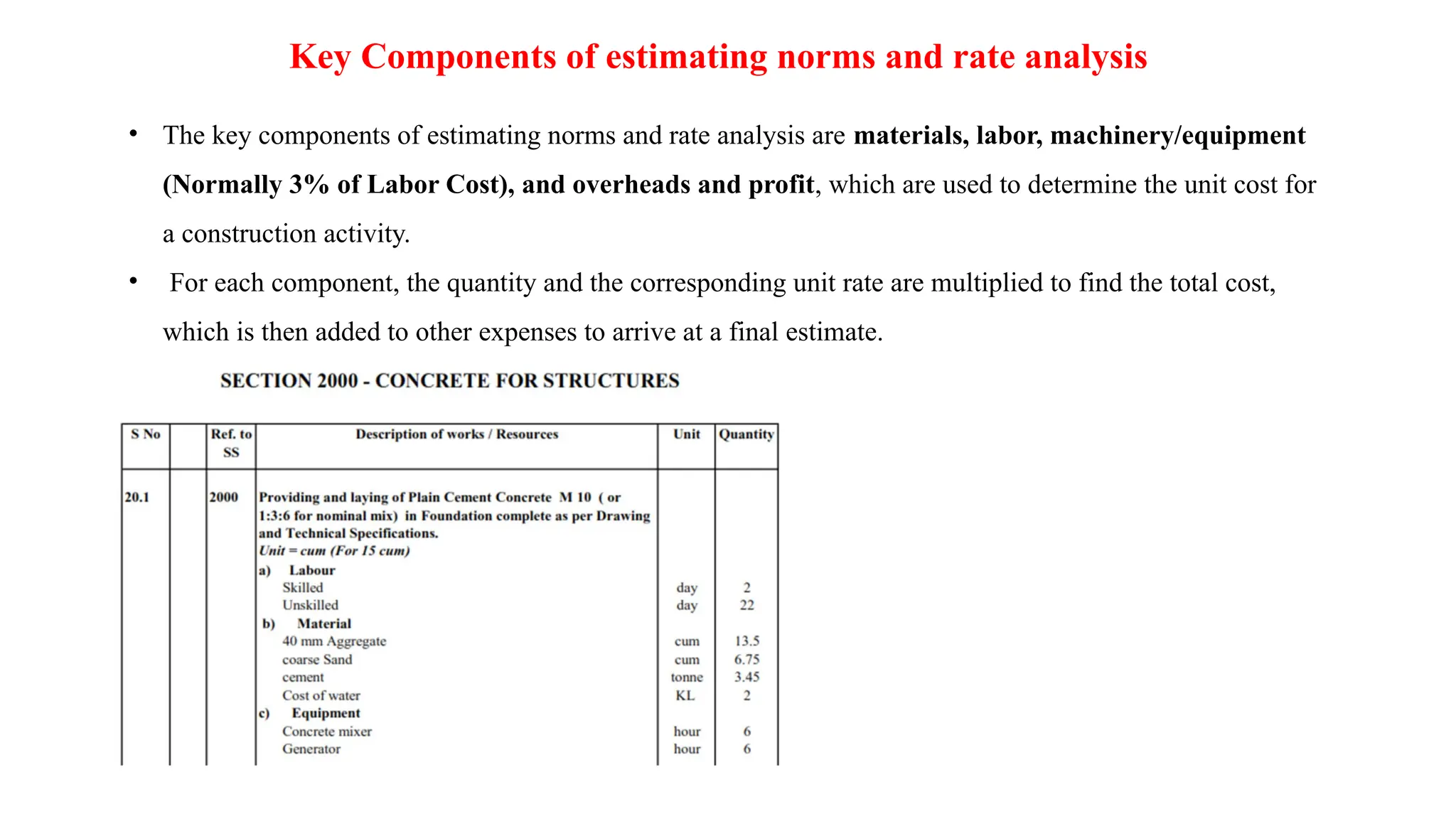

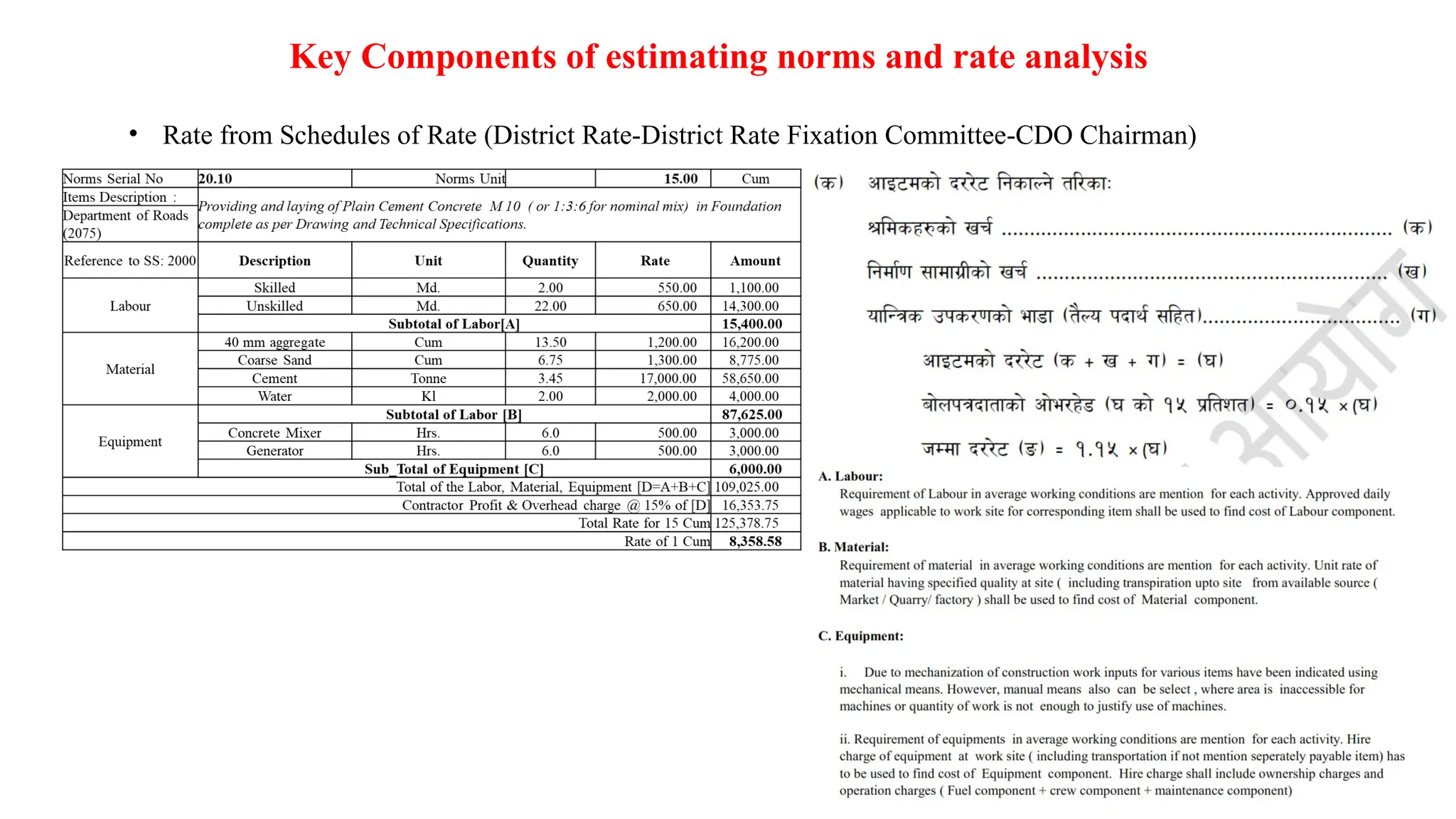

Key Components ofestimating norms and rate analysis

• The key components of estimating norms and rate analysis are materials, labor, machinery/equipment

(Normally 3% of Labor Cost), and overheads and profit, which are used to determine the unit cost for

a construction activity.

• For each component, the quantity and the corresponding unit rate are multiplied to find the total cost,

which is then added to other expenses to arrive at a final estimate.

17.

Key Components ofestimating norms and rate analysis

• Rate from Schedules of Rate (District Rate-District Rate Fixation Committee-CDO Chairman)

18.

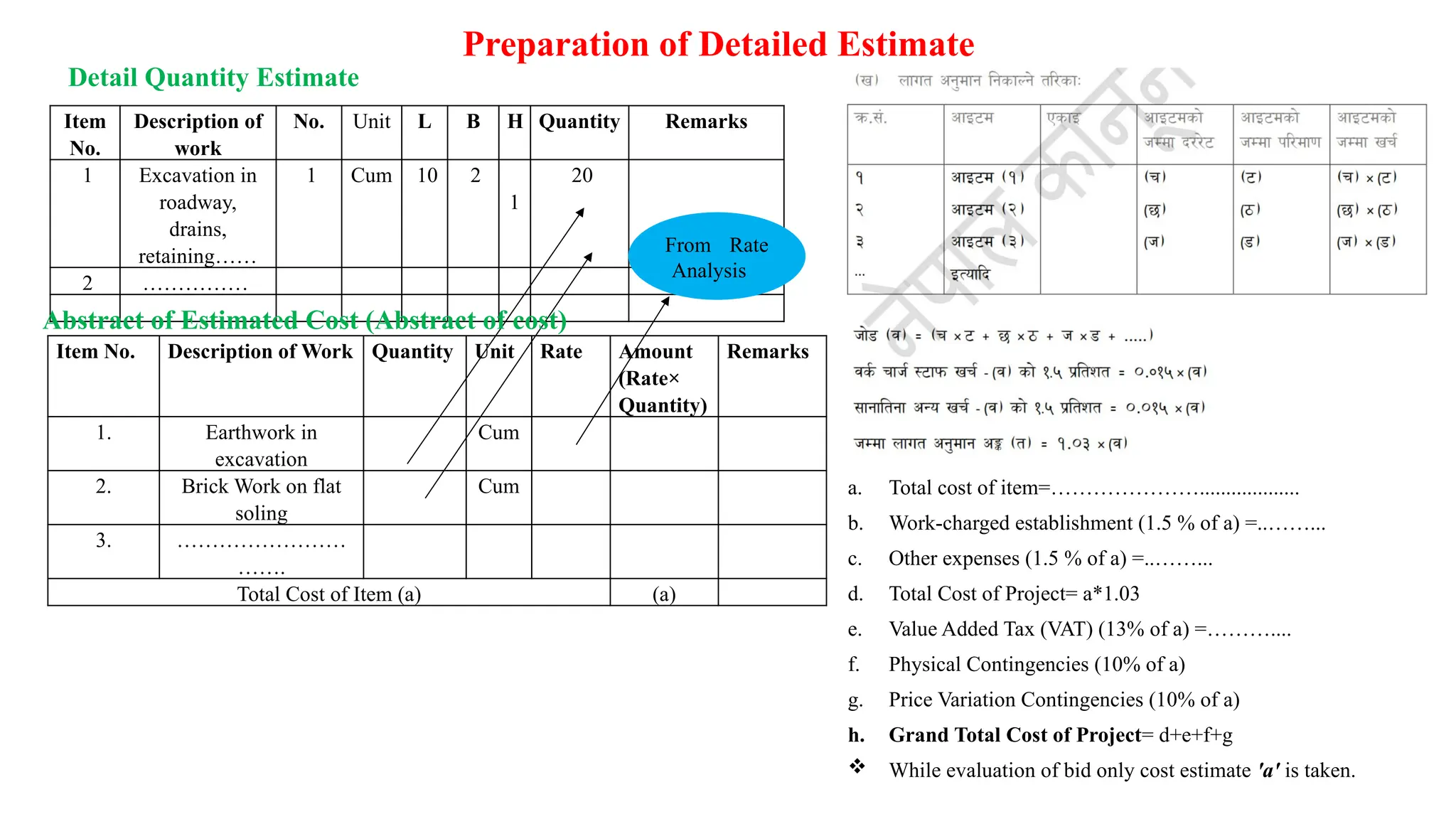

Preparation of DetailedEstimate

Item

No.

Description of

work

No. Unit L B H Quantity Remarks

1 Excavation in

roadway,

drains,

retaining……

1 Cum 10 2

1

20

2 ……………

Item No. Description of Work Quantity Unit Rate Amount

(Rate×

Quantity)

Remarks

1. Earthwork in

excavation

Cum

2. Brick Work on flat

soling

Cum

3. ……………………

…….

Total Cost of Item (a) (a)

From Rate

Analysis

a. Total cost of item=…………………...................

b. Work-charged establishment (1.5 % of a) =..……...

c. Other expenses (1.5 % of a) =..……...

d. Total Cost of Project= a*1.03

e. Value Added Tax (VAT) (13% of a) =………....

f. Physical Contingencies (10% of a)

g. Price Variation Contingencies (10% of a)

h. Grand Total Cost of Project= d+e+f+g

While evaluation of bid only cost estimate 'a' is taken.

Detail Quantity Estimate

Abstract of Estimated Cost (Abstract of cost)

19.

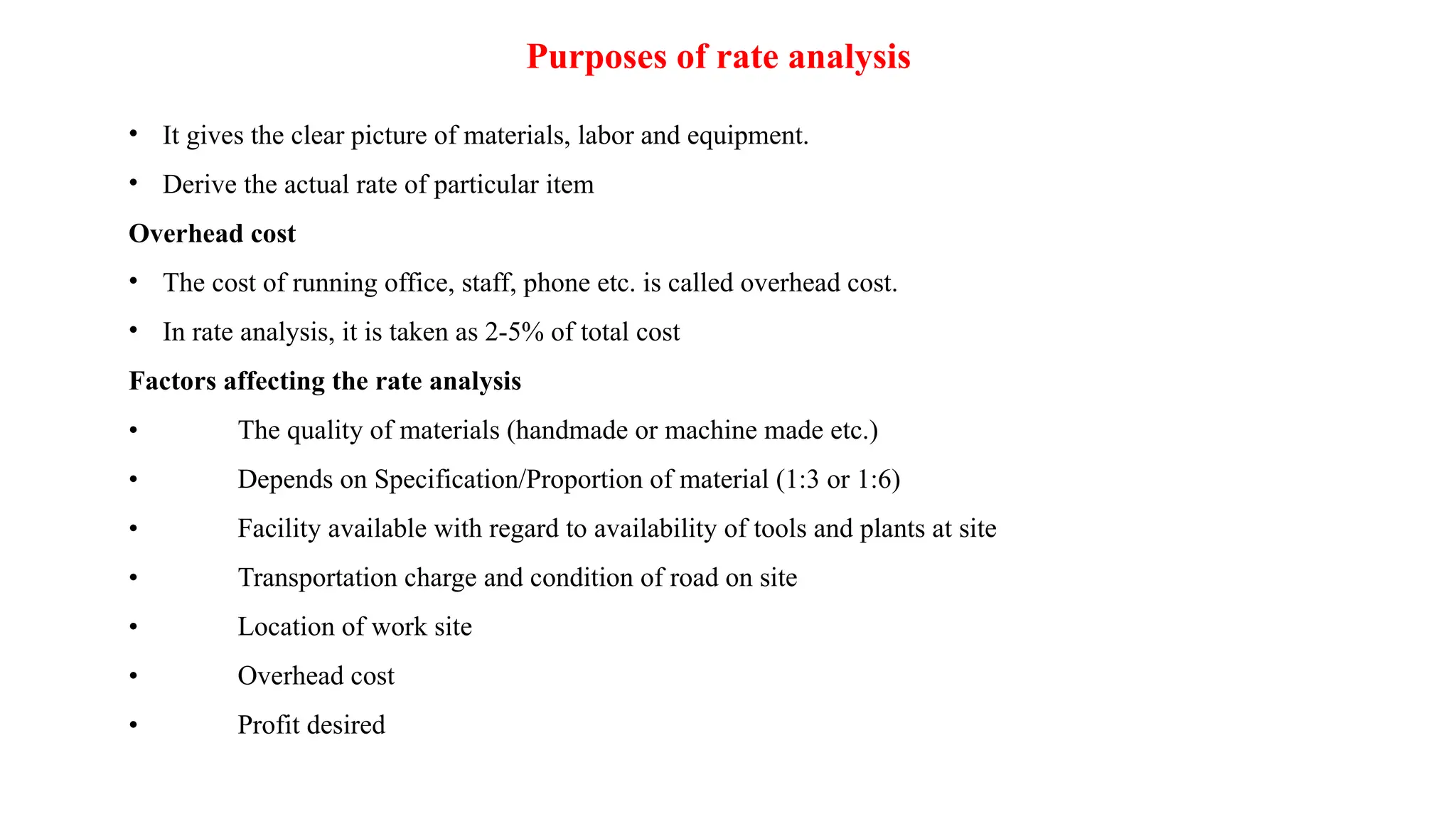

Purposes of rateanalysis

• It gives the clear picture of materials, labor and equipment.

• Derive the actual rate of particular item

Overhead cost

• The cost of running office, staff, phone etc. is called overhead cost.

• In rate analysis, it is taken as 2-5% of total cost

Factors affecting the rate analysis

• The quality of materials (handmade or machine made etc.)

• Depends on Specification/Proportion of material (1:3 or 1:6)

• Facility available with regard to availability of tools and plants at site

• Transportation charge and condition of road on site

• Location of work site

• Overhead cost

• Profit desired

20.

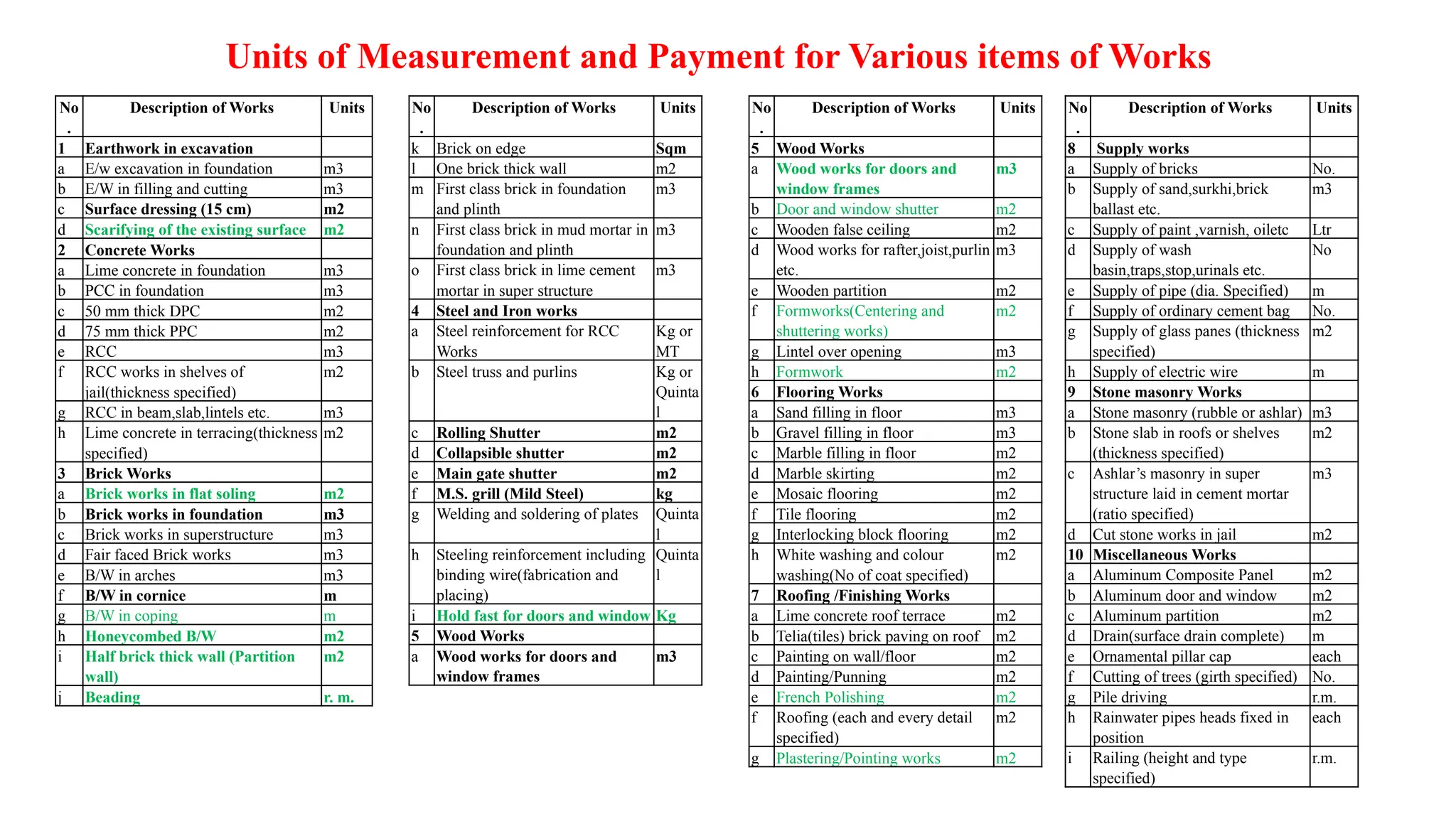

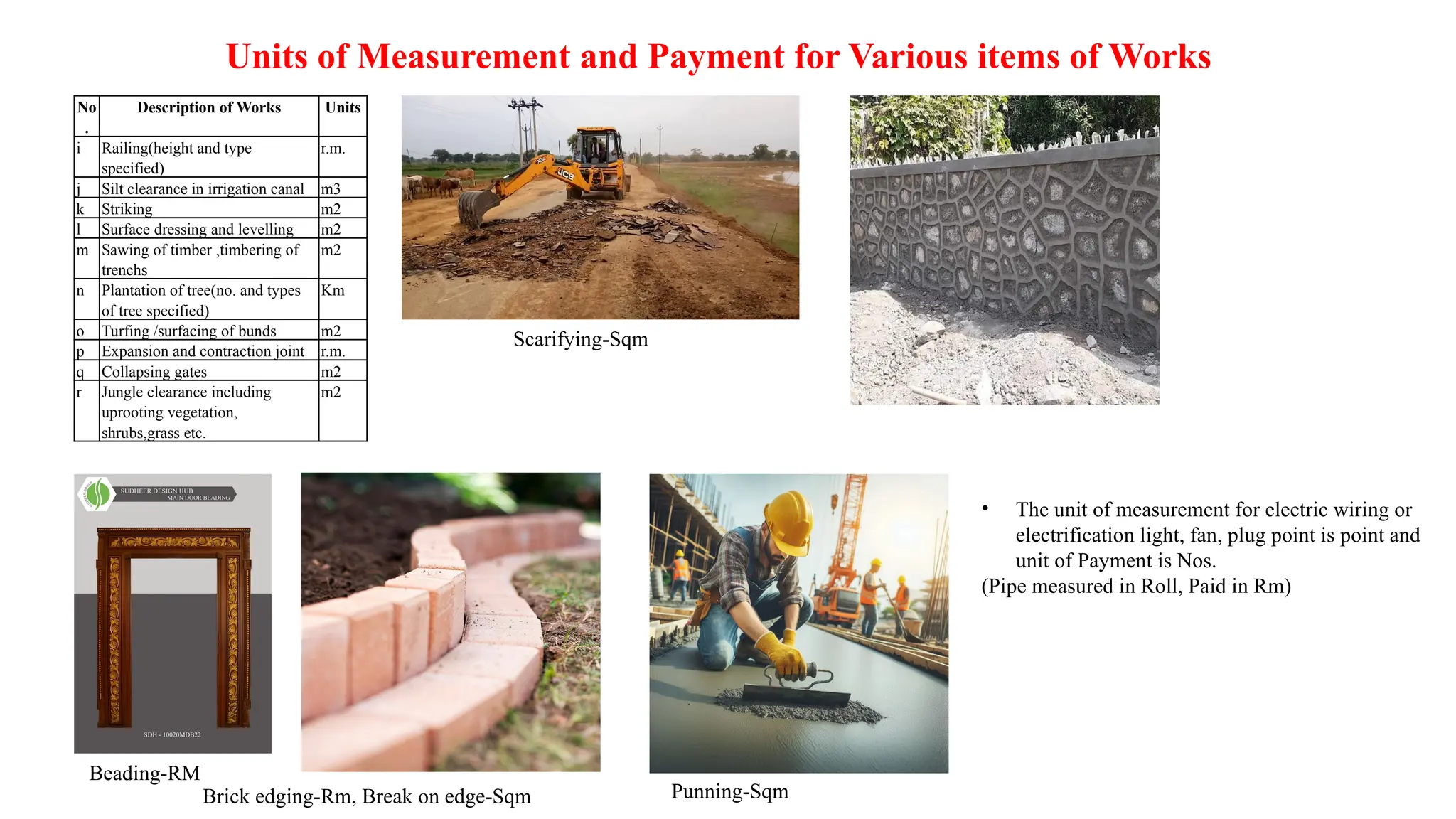

Units of Measurementand Payment for Various items of Works

No

.

Description of Works Units

1 Earthwork in excavation

a E/w excavation in foundation m3

b E/W in filling and cutting m3

c Surface dressing (15 cm) m2

d Scarifying of the existing surface m2

2 Concrete Works

a Lime concrete in foundation m3

b PCC in foundation m3

c 50 mm thick DPC m2

d 75 mm thick PPC m2

e RCC m3

f RCC works in shelves of

jail(thickness specified)

m2

g RCC in beam,slab,lintels etc. m3

h Lime concrete in terracing(thickness

specified)

m2

3 Brick Works

a Brick works in flat soling m2

b Brick works in foundation m3

c Brick works in superstructure m3

d Fair faced Brick works m3

e B/W in arches m3

f B/W in cornice m

g B/W in coping m

h Honeycombed B/W m2

i Half brick thick wall (Partition

wall)

m2

j Beading r. m.

No

.

Description of Works Units

k Brick on edge Sqm

l One brick thick wall m2

m First class brick in foundation

and plinth

m3

n First class brick in mud mortar in

foundation and plinth

m3

o First class brick in lime cement

mortar in super structure

m3

4 Steel and Iron works

a Steel reinforcement for RCC

Works

Kg or

MT

b Steel truss and purlins Kg or

Quinta

l

c Rolling Shutter m2

d Collapsible shutter m2

e Main gate shutter m2

f M.S. grill (Mild Steel) kg

g Welding and soldering of plates Quinta

l

h Steeling reinforcement including

binding wire(fabrication and

placing)

Quinta

l

i Hold fast for doors and window Kg

5 Wood Works

a Wood works for doors and

window frames

m3

No

.

Description of Works Units

5 Wood Works

a Wood works for doors and

window frames

m3

b Door and window shutter m2

c Wooden false ceiling m2

d Wood works for rafter,joist,purlin

etc.

m3

e Wooden partition m2

f Formworks(Centering and

shuttering works)

m2

g Lintel over opening m3

h Formwork m2

6 Flooring Works

a Sand filling in floor m3

b Gravel filling in floor m3

c Marble filling in floor m2

d Marble skirting m2

e Mosaic flooring m2

f Tile flooring m2

g Interlocking block flooring m2

h White washing and colour

washing(No of coat specified)

m2

7 Roofing /Finishing Works

a Lime concrete roof terrace m2

b Telia(tiles) brick paving on roof m2

c Painting on wall/floor m2

d Painting/Punning m2

e French Polishing m2

f Roofing (each and every detail

specified)

m2

g Plastering/Pointing works m2

No

.

Description of Works Units

8 Supply works

a Supply of bricks No.

b Supply of sand,surkhi,brick

ballast etc.

m3

c Supply of paint ,varnish, oiletc Ltr

d Supply of wash

basin,traps,stop,urinals etc.

No

e Supply of pipe (dia. Specified) m

f Supply of ordinary cement bag No.

g Supply of glass panes (thickness

specified)

m2

h Supply of electric wire m

9 Stone masonry Works

a Stone masonry (rubble or ashlar) m3

b Stone slab in roofs or shelves

(thickness specified)

m2

c Ashlar’s masonry in super

structure laid in cement mortar

(ratio specified)

m3

d Cut stone works in jail m2

10 Miscellaneous Works

a Aluminum Composite Panel m2

b Aluminum door and window m2

c Aluminum partition m2

d Drain(surface drain complete) m

e Ornamental pillar cap each

f Cutting of trees (girth specified) No.

g Pile driving r.m.

h Rainwater pipes heads fixed in

position

each

i Railing (height and type

specified)

r.m.

21.

Units of Measurementand Payment for Various items of Works

No

.

Description of Works Units

i Railing(height and type

specified)

r.m.

j Silt clearance in irrigation canal m3

k Striking m2

l Surface dressing and levelling m2

m Sawing of timber ,timbering of

trenchs

m2

n Plantation of tree(no. and types

of tree specified)

Km

o Turfing /surfacing of bunds m2

p Expansion and contraction joint r.m.

q Collapsing gates m2

r Jungle clearance including

uprooting vegetation,

shrubs,grass etc.

m2

Scarifying-Sqm

Beading-RM

Brick edging-Rm, Break on edge-Sqm

• The unit of measurement for electric wiring or

electrification light, fan, plug point is point and

unit of Payment is Nos.

(Pipe measured in Roll, Paid in Rm)

Punning-Sqm

22.

Units of Measurementand Payment for Various items of Works

Bar reinforcement shall be measured in kg.

The steel work shall be measured in kg.

Weighted of cleats, brackets, packing pieces, bolts, nuts, washers, gussets shall be added to the weight of

respective items no separate measurement and payment.

Plane and barbed fencing shall be measured in running meter.

Pointing works shall be measured in square meter.

Scarifying of road surface shall be measured in square meter.

Site clearance shall be measured in square meter.

Cribbing/falsework shall be measured in square meter.

Scaffolding shall be measured in square meter.

Glazing shall be measured in square meter.

Blasting material is measured in Kg and quarrying of stone is measured in cubic meter.

Prime Coat/Tack Coat in Liter.

Premix Carpet, DBST in Sqm.

23.

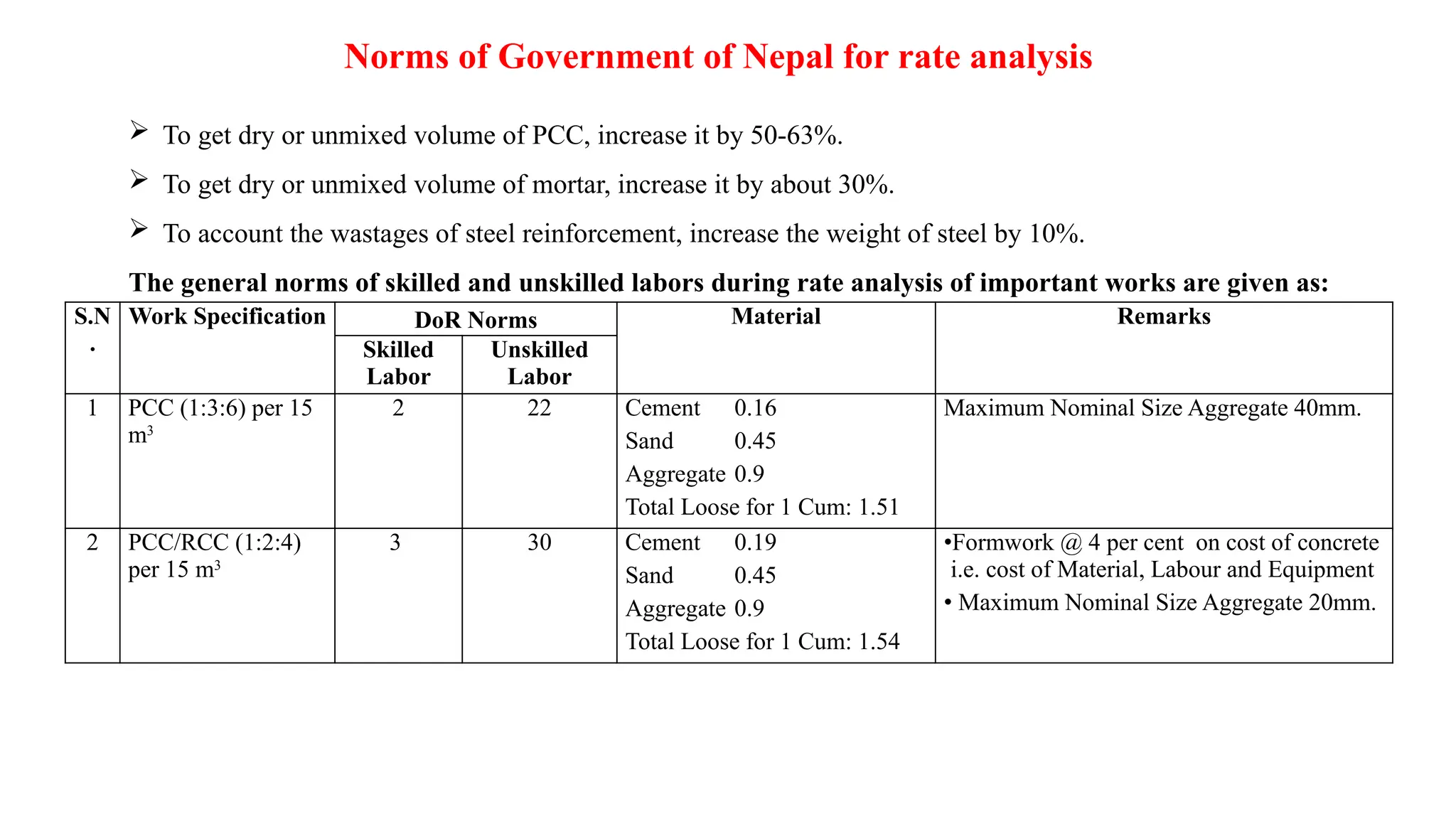

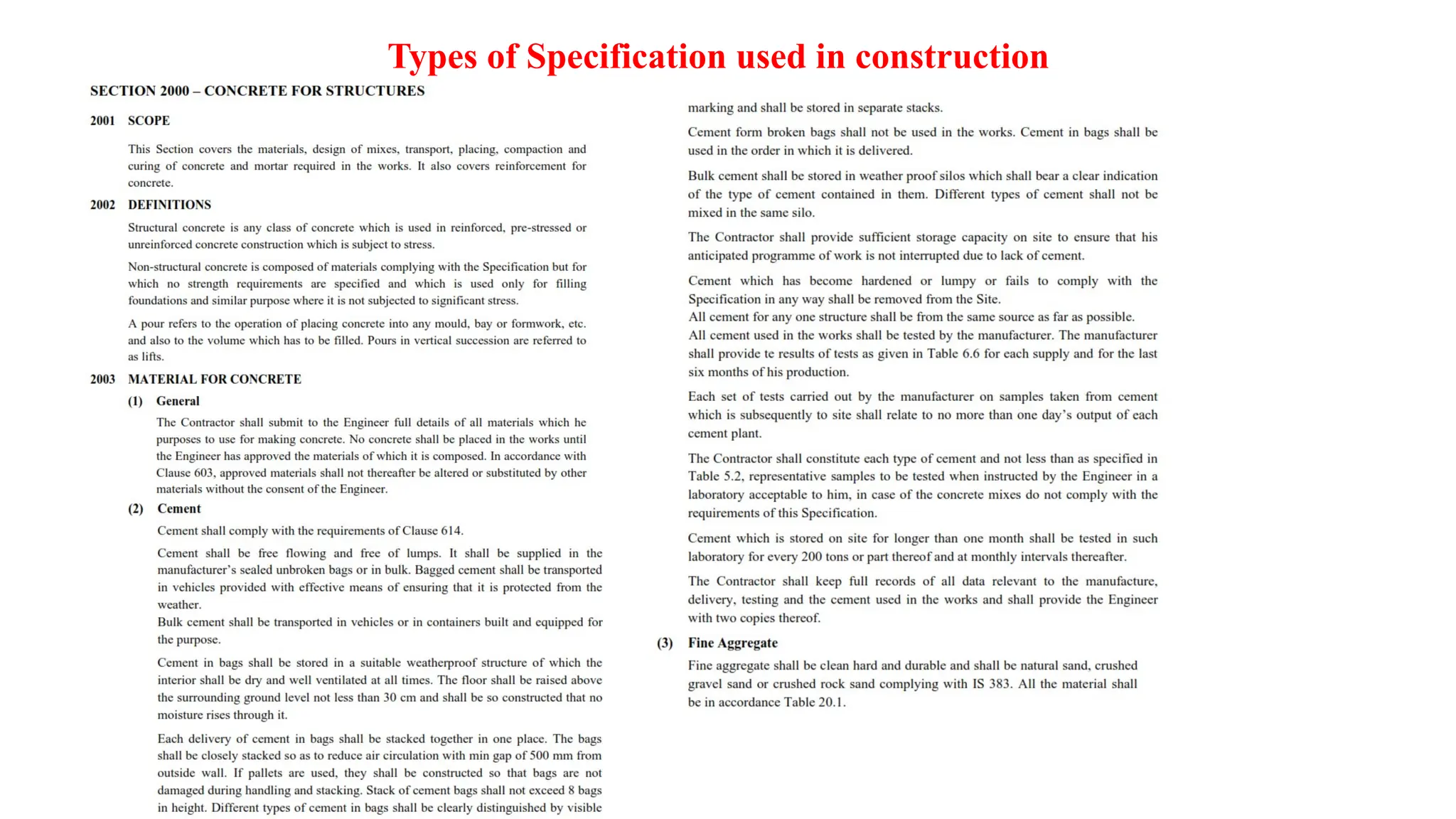

Norms of Governmentof Nepal for rate analysis

To get dry or unmixed volume of PCC, increase it by 50-63%.

To get dry or unmixed volume of mortar, increase it by about 30%.

To account the wastages of steel reinforcement, increase the weight of steel by 10%.

The general norms of skilled and unskilled labors during rate analysis of important works are given as:

S.N

.

Work Specification DoR Norms Material Remarks

Skilled

Labor

Unskilled

Labor

1 PCC (1:3:6) per 15

m3

2 22 Cement 0.16

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.51

Maximum Nominal Size Aggregate 40mm.

2 PCC/RCC (1:2:4)

per 15 m3

3 30 Cement 0.19

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.54

•Formwork @ 4 per cent on cost of concrete

i.e. cost of Material, Labour and Equipment

• Maximum Nominal Size Aggregate 20mm.

24.

Norms of Governmentof Nepal for rate analysis

S.N

.

Work Specification DoR Norms Material Remarks

Skilled

Labor

Unskilled

Labor

3 PCC/RCC(1:1.5:3)

M20 per 15 m3

3 30 Cement 0.24

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.59

•Formwork @ 4 per cent on cost of concrete

i.e. cost of Material, Labor and Equipment

• For PCC Maximum Nominal Size 40mm,

for RCC 20mm Aggregate.

4 PCC (1:1:2) M25

per 15 m3

3 30 Cement 0.28

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.63

•Formwork @ 4 per cent on cost of concrete

i.e. cost of Material, Labor and Equipment

• For PCC Maximum Nominal Size 40mm,

for RCC 20mm Aggregate.

5 Reinforcement

Works [SS 2014]

(for 1 MT)

4 9 MS Bars 1.1

Binding Wire 8 Kg

10% for wastage.

25.

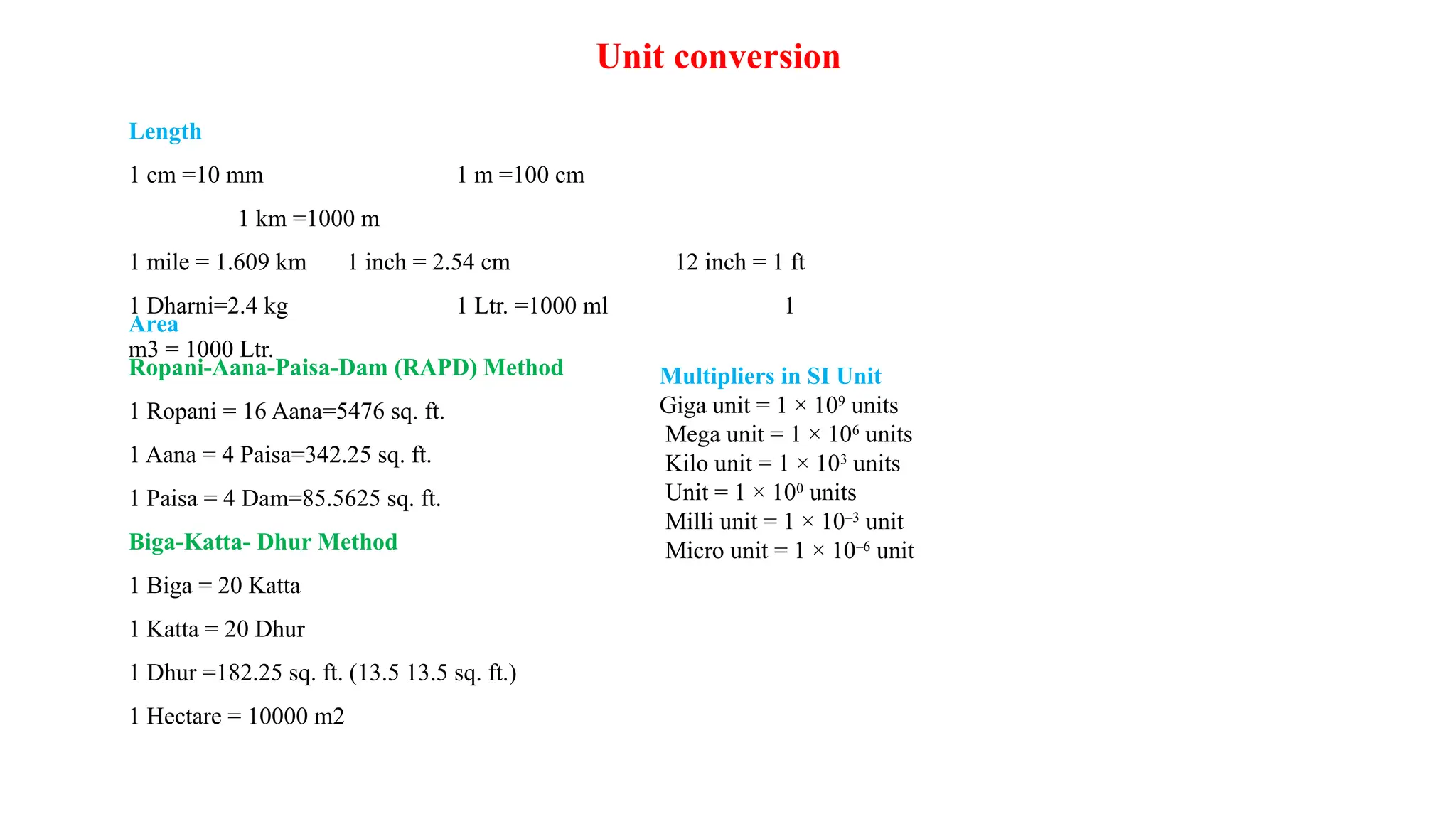

Unit conversion

Length

1 cm=10 mm 1 m =100 cm

1 km =1000 m

1 mile = 1.609 km 1 inch = 2.54 cm 12 inch = 1 ft

1 Dharni=2.4 kg 1 Ltr. =1000 ml 1

m3 = 1000 Ltr.

Area

Ropani-Aana-Paisa-Dam (RAPD) Method

1 Ropani = 16 Aana=5476 sq. ft.

1 Aana = 4 Paisa=342.25 sq. ft.

1 Paisa = 4 Dam=85.5625 sq. ft.

Biga-Katta- Dhur Method

1 Biga = 20 Katta

1 Katta = 20 Dhur

1 Dhur =182.25 sq. ft. (13.5 13.5 sq. ft.)

1 Hectare = 10000 m2

Multipliers in SI Unit

Giga unit = 1 × 109

units

Mega unit = 1 × 106

units

Kilo unit = 1 × 103

units

Unit = 1 × 100

units

Milli unit = 1 × 10–3

unit

Micro unit = 1 × 10–6

unit

26.

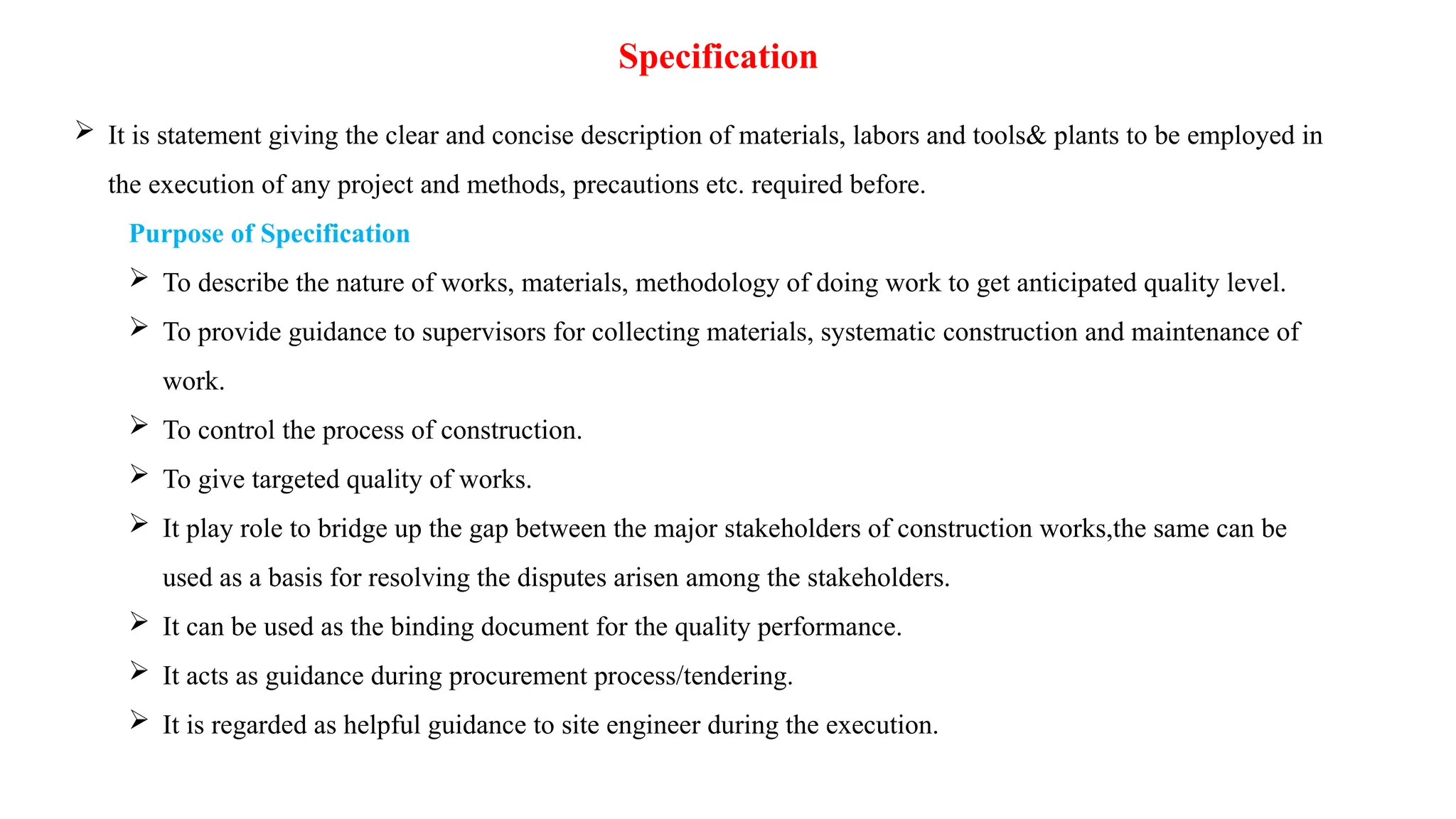

Specification

It isstatement giving the clear and concise description of materials, labors and tools& plants to be employed in

the execution of any project and methods, precautions etc. required before.

Purpose of Specification

To describe the nature of works, materials, methodology of doing work to get anticipated quality level.

To provide guidance to supervisors for collecting materials, systematic construction and maintenance of

work.

To control the process of construction.

To give targeted quality of works.

It play role to bridge up the gap between the major stakeholders of construction works,the same can be

used as a basis for resolving the disputes arisen among the stakeholders.

It can be used as the binding document for the quality performance.

It acts as guidance during procurement process/tendering.

It is regarded as helpful guidance to site engineer during the execution.

27.

Specification Writing

Specificationlanguage

Brevity (brief)

Fairness

Standard size and pattern

Inclusion of all items

Avoidance of repetition of information

Inapplicable text

Statement regarding quality of final product

Specification in paragraph

28.

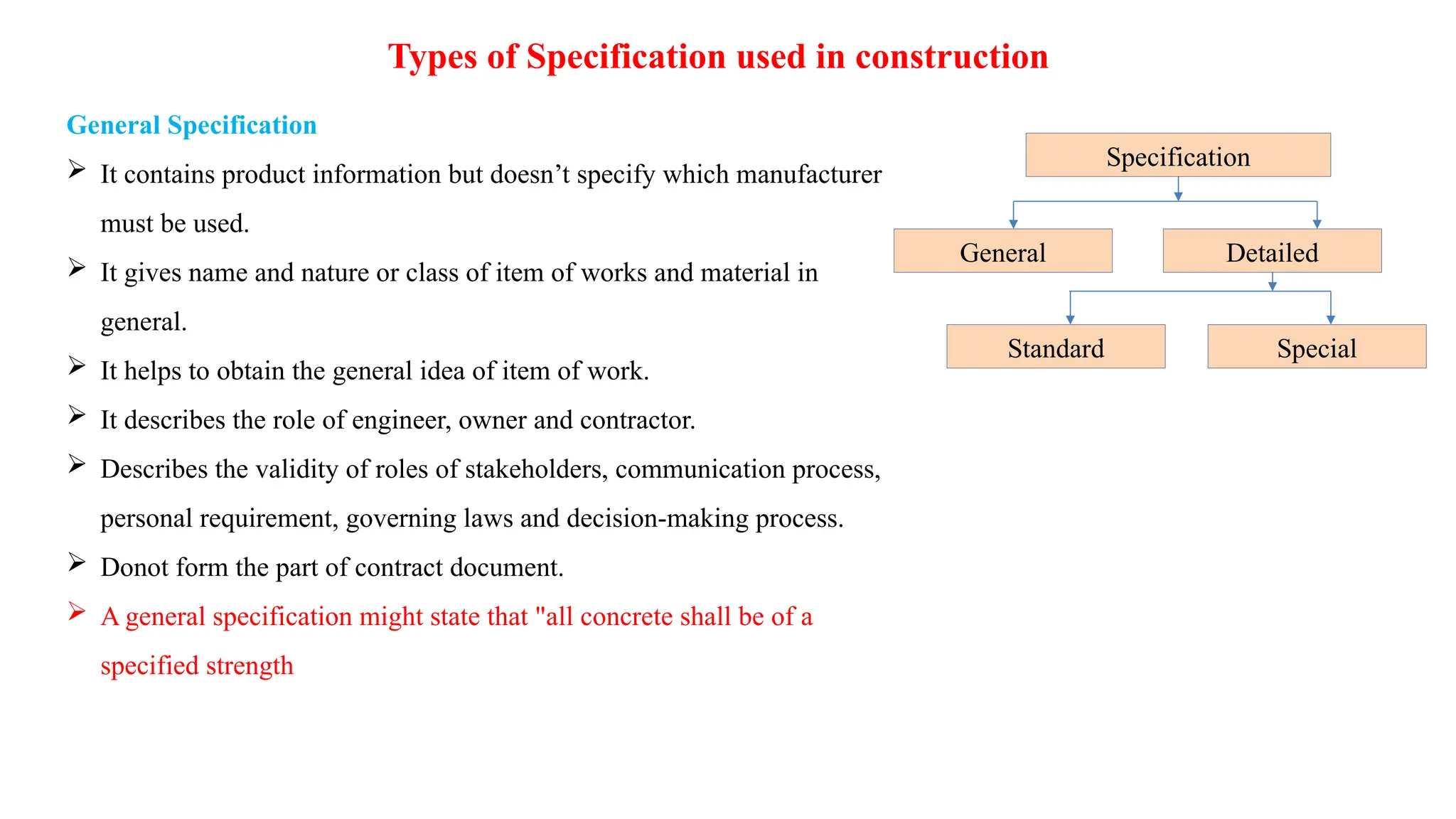

Types of Specificationused in construction

General Specification

It contains product information but doesn’t specify which manufacturer

must be used.

It gives name and nature or class of item of works and material in

general.

It helps to obtain the general idea of item of work.

It describes the role of engineer, owner and contractor.

Describes the validity of roles of stakeholders, communication process,

personal requirement, governing laws and decision-making process.

Donot form the part of contract document.

A general specification might state that "all concrete shall be of a

specified strength

Specification

General Detailed

Standard Special

29.

Types of Specificationused in construction

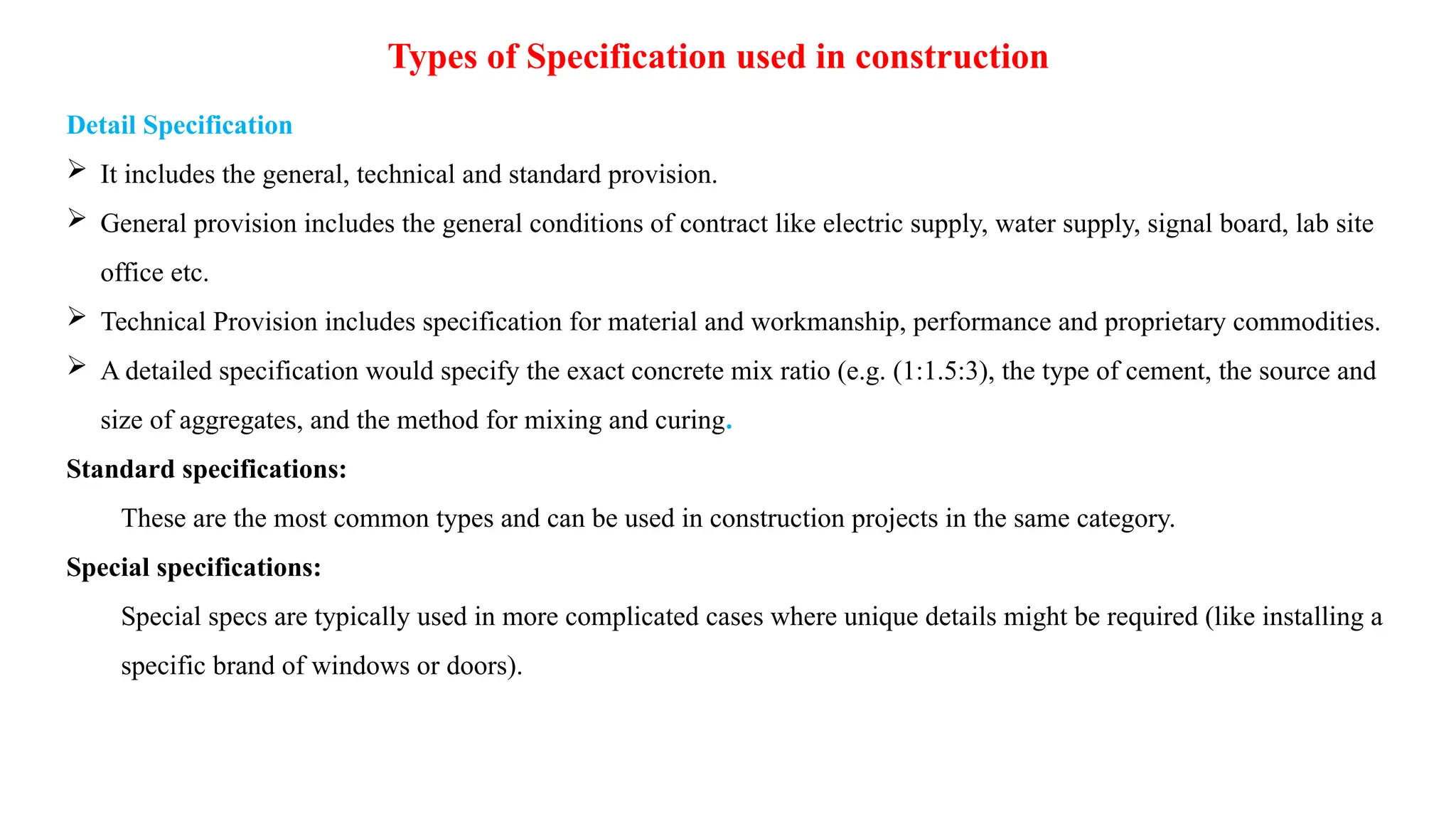

Detail Specification

It includes the general, technical and standard provision.

General provision includes the general conditions of contract like electric supply, water supply, signal board, lab site

office etc.

Technical Provision includes specification for material and workmanship, performance and proprietary commodities.

A detailed specification would specify the exact concrete mix ratio (e.g. (1:1.5:3), the type of cement, the source and

size of aggregates, and the method for mixing and curing.

Standard specifications:

These are the most common types and can be used in construction projects in the same category.

Special specifications:

Special specs are typically used in more complicated cases where unique details might be required (like installing a

specific brand of windows or doors).

Preparation of Billof Quantities (BoQs)

It is a statement showing the item number, description of work, unit of measurement, quantity, item rate (in fig. and

word) and amount in column is unfilled. It is filled by tenderer/bidder.

The BoQ after filled by the bidders is called priced BoQ.

Item

no.

Description of work Quantity Unit Rate Amount Remarks

Figures Words

1. Earthwork in excavation in

foundation with lifts 1.5 m

and lead 30 m in ordinary

soil. [SSRBW 900]

……… Cum

2. Providing and laying soling

brick on flat foundation

including sand blinding.

……….. Cum

To be filled by

bidder

32.

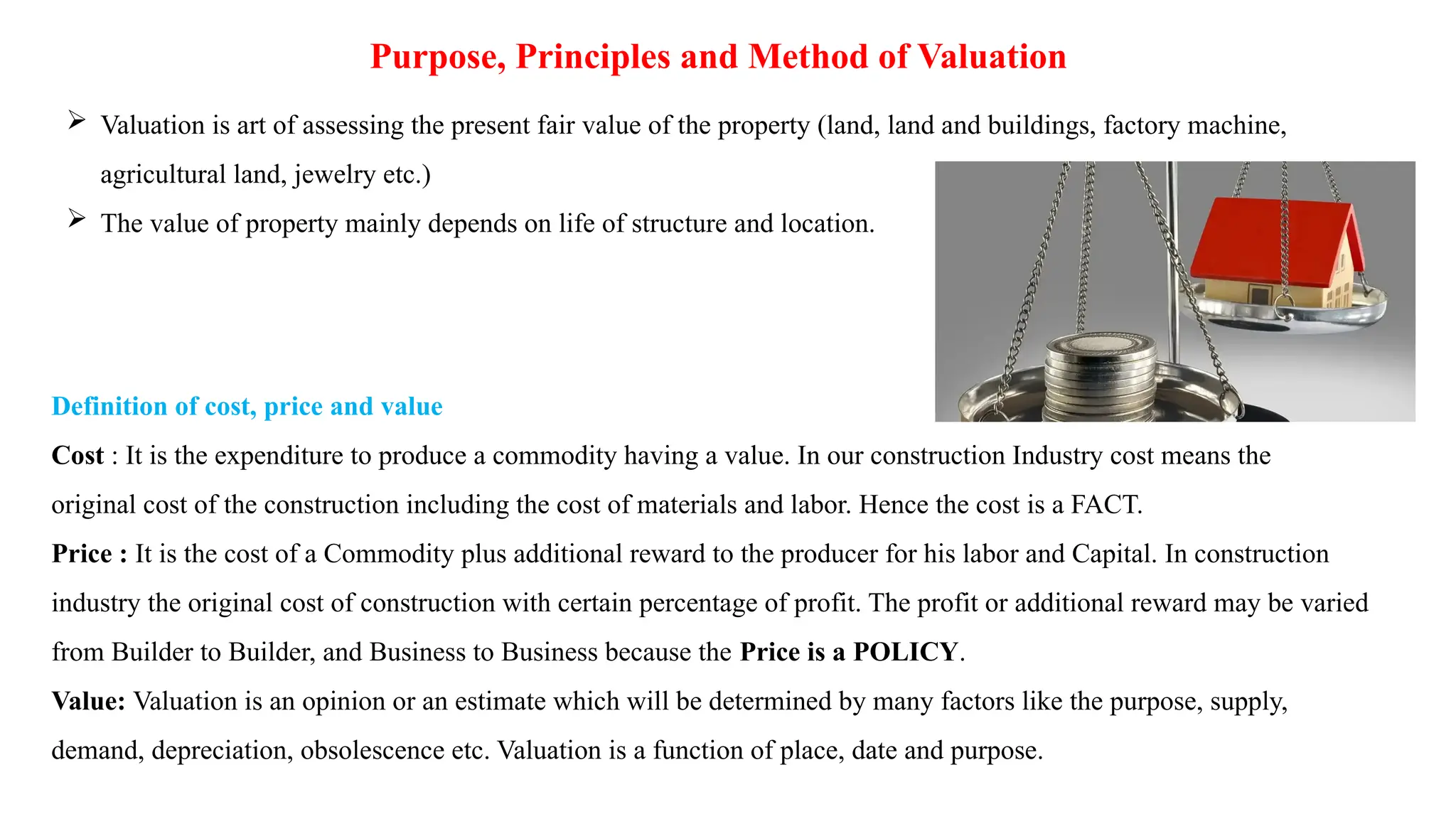

Purpose, Principles andMethod of Valuation

Valuation is art of assessing the present fair value of the property (land, land and buildings, factory machine,

agricultural land, jewelry etc.)

The value of property mainly depends on life of structure and location.

Definition of cost, price and value

Cost : It is the expenditure to produce a commodity having a value. In our construction Industry cost means the

original cost of the construction including the cost of materials and labor. Hence the cost is a FACT.

Price : It is the cost of a Commodity plus additional reward to the producer for his labor and Capital. In construction

industry the original cost of construction with certain percentage of profit. The profit or additional reward may be varied

from Builder to Builder, and Business to Business because the Price is a POLICY.

Value: Valuation is an opinion or an estimate which will be determined by many factors like the purpose, supply,

demand, depreciation, obsolescence etc. Valuation is a function of place, date and purpose.

33.

Purpose of Valuation

Buying and selling of the property

Auction bid of the property

Acquisition of property (compensation)

Partition of property

Insurance of property

Assessment of tax

Security of loan

Determination of rent of property

Preparation of balance sheet of company/firm

Determination of court fee of property

34.

Principles of Valuation

Supply and demand of property.

Its design and specification of materials used.

Location.

Purpose of valuation.

Age of property and physical conditions.

Present and future use of property

35.

Depreciation

It isthe gradual reduction in the value of property due to wear and tear, decay, obsolescence etc.It is

dependent on longevity of structure, physical condition, usage etc.

Types of Depreciation

• Physical depreciation • Functional depreciation • Locational

depreciation

36.

Method of CalculatingDepreciation

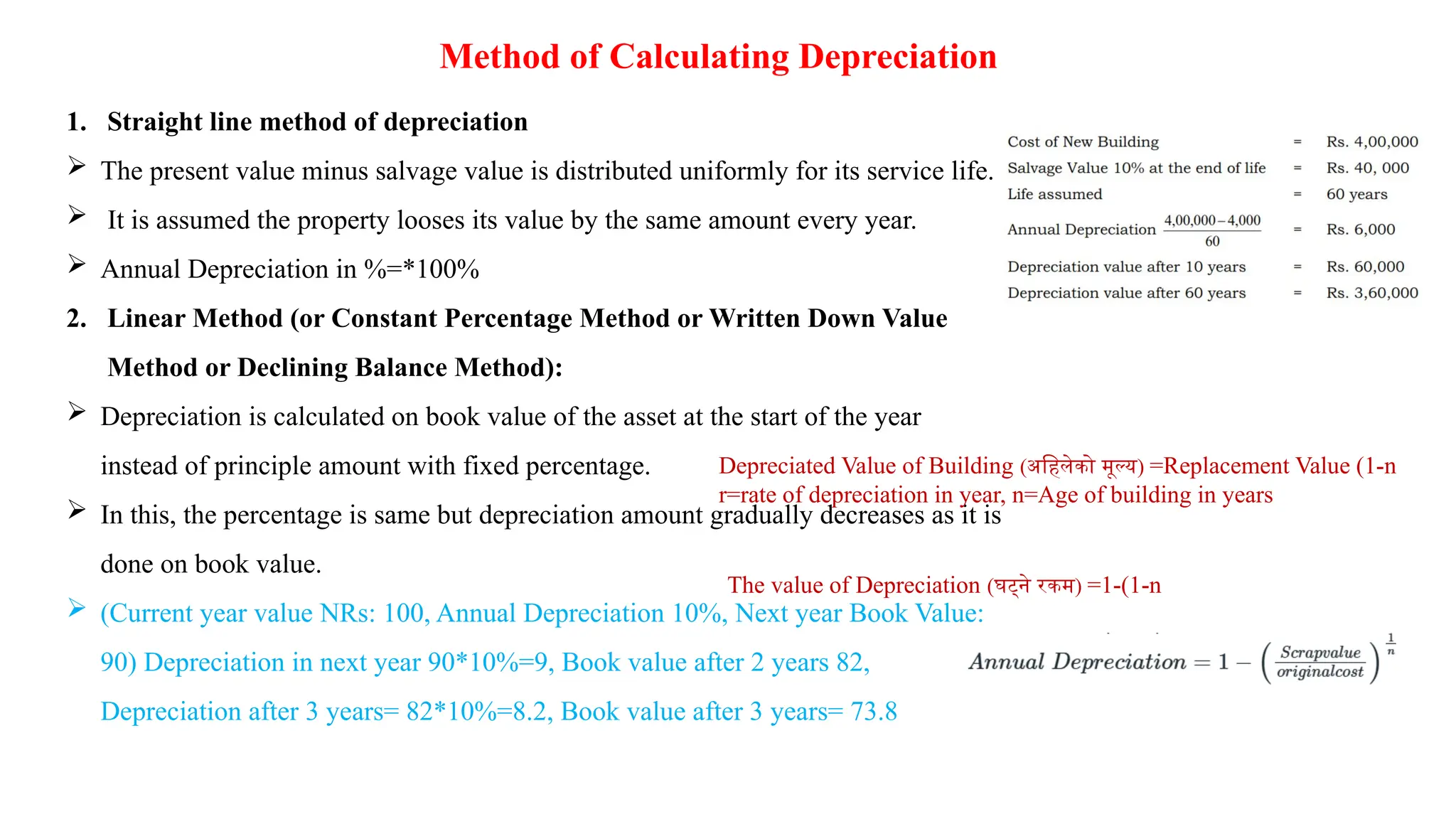

1. Straight line method of depreciation

The present value minus salvage value is distributed uniformly for its service life.

It is assumed the property looses its value by the same amount every year.

Annual Depreciation in %=*100%

2. Linear Method (or Constant Percentage Method or Written Down Value

Method or Declining Balance Method):

Depreciation is calculated on book value of the asset at the start of the year

instead of principle amount with fixed percentage.

In this, the percentage is same but depreciation amount gradually decreases as it is

done on book value.

(Current year value NRs: 100, Annual Depreciation 10%, Next year Book Value:

90) Depreciation in next year 90*10%=9, Book value after 2 years 82,

Depreciation after 3 years= 82*10%=8.2, Book value after 3 years= 73.8

Depreciated Value of Building (अहिलेको मूल्य) =Replacement Value (1-n

r=rate of depreciation in year, n=Age of building in years

The value of Depreciation (घट्ने रकम) =1-(1-n

37.

Method of CalculatingDepreciation

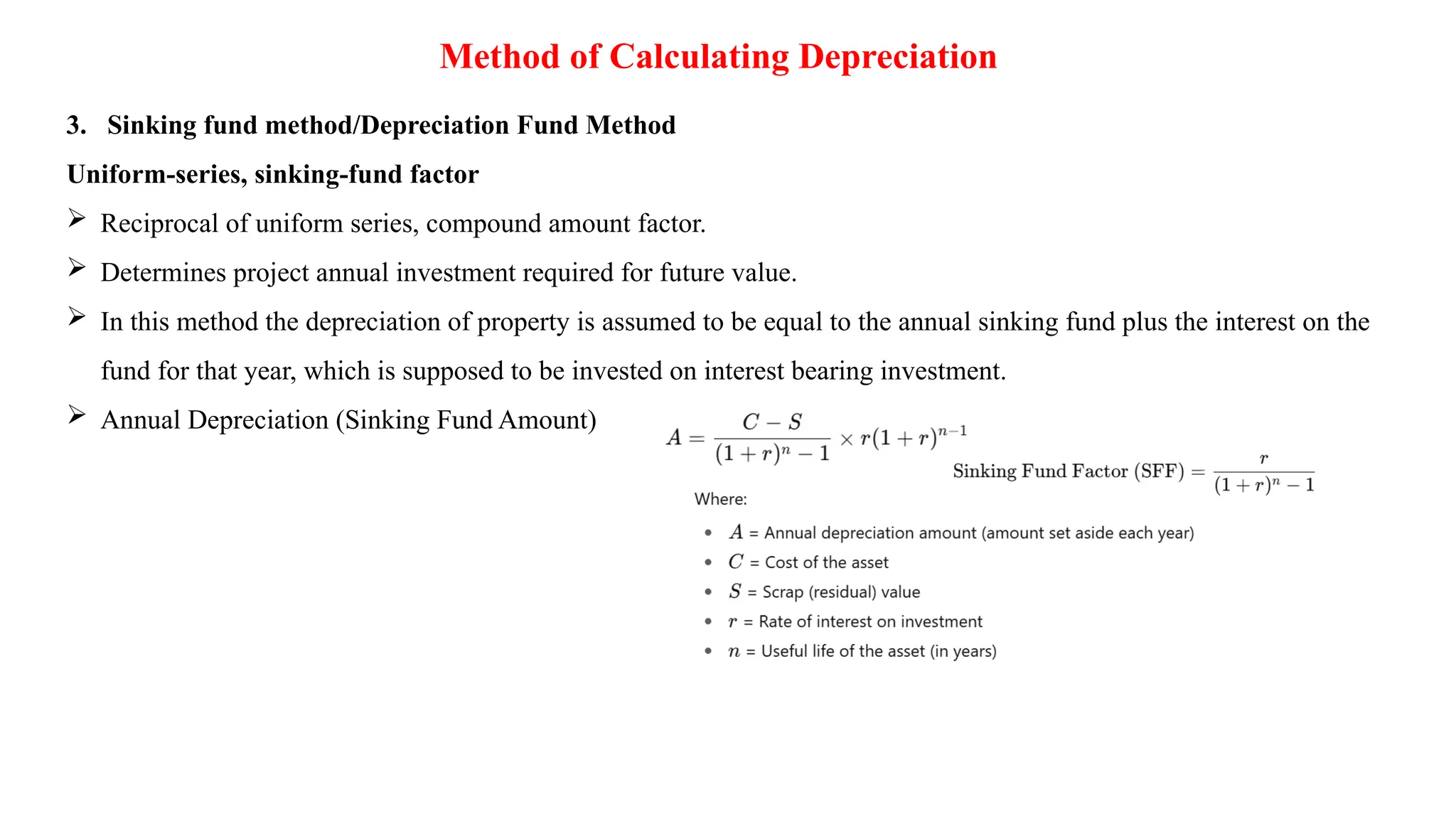

3. Sinking fund method/Depreciation Fund Method

Uniform-series, sinking-fund factor

Reciprocal of uniform series, compound amount factor.

Determines project annual investment required for future value.

In this method the depreciation of property is assumed to be equal to the annual sinking fund plus the interest on the

fund for that year, which is supposed to be invested on interest bearing investment.

Annual Depreciation (Sinking Fund Amount)

38.

Method of valuation

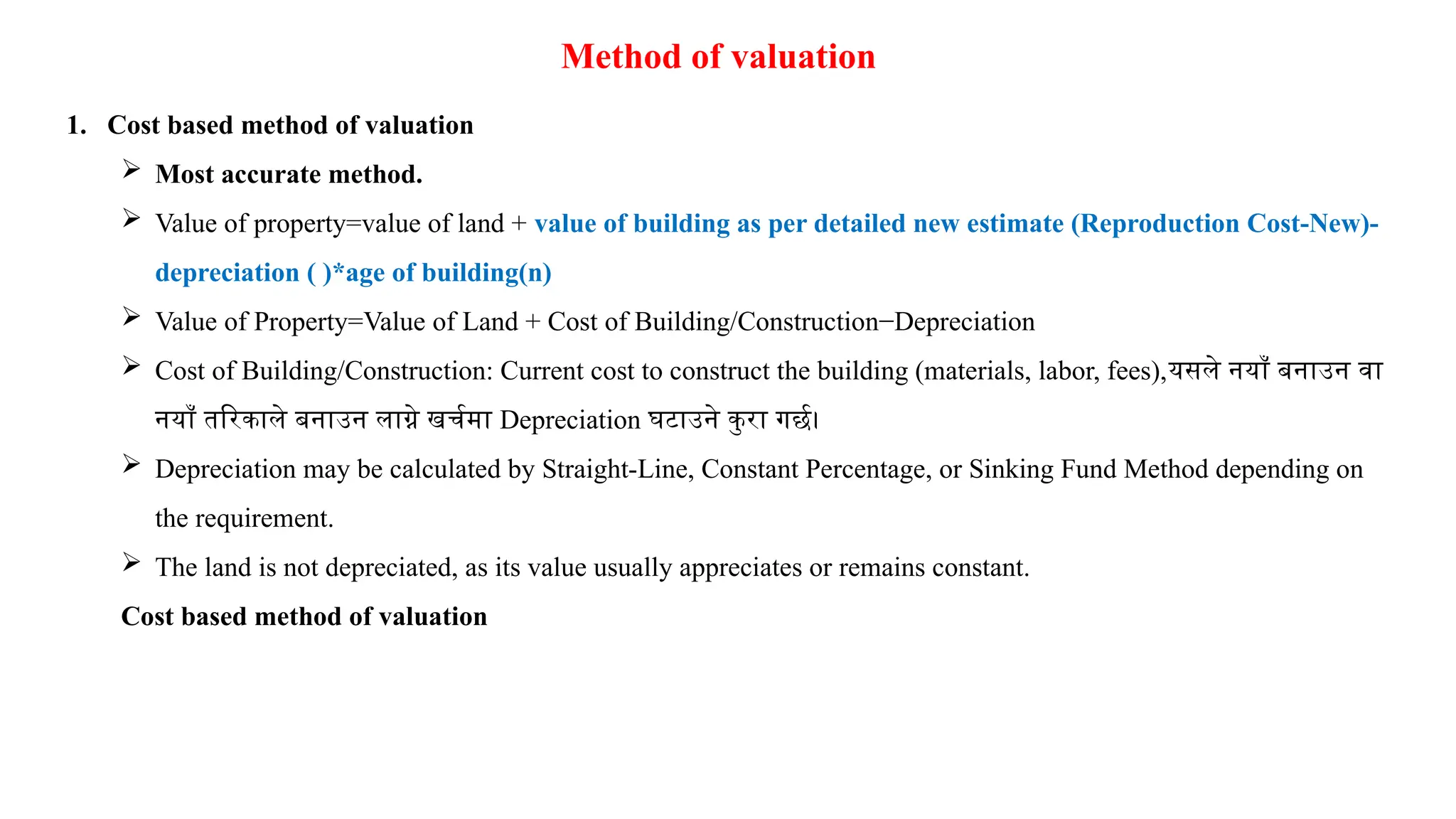

1.Cost based method of valuation

Most accurate method.

Value of property=value of land + value of building as per detailed new estimate (Reproduction Cost-New)-

depreciation ( )*age of building(n)

Value of Property=Value of Land + Cost of Building/Construction−Depreciation

Cost of Building/Construction: Current cost to construct the building (materials, labor, fees),यसले नयाँ बनाउन वा

नयाँ तरिकाले बनाउन लाग्ने खर्चमा Depreciation घटाउने कुरा गर्छ।

Depreciation may be calculated by Straight-Line, Constant Percentage, or Sinking Fund Method depending on

the requirement.

The land is not depreciated, as its value usually appreciates or remains constant.

Cost based method of valuation

39.

Method of valuation

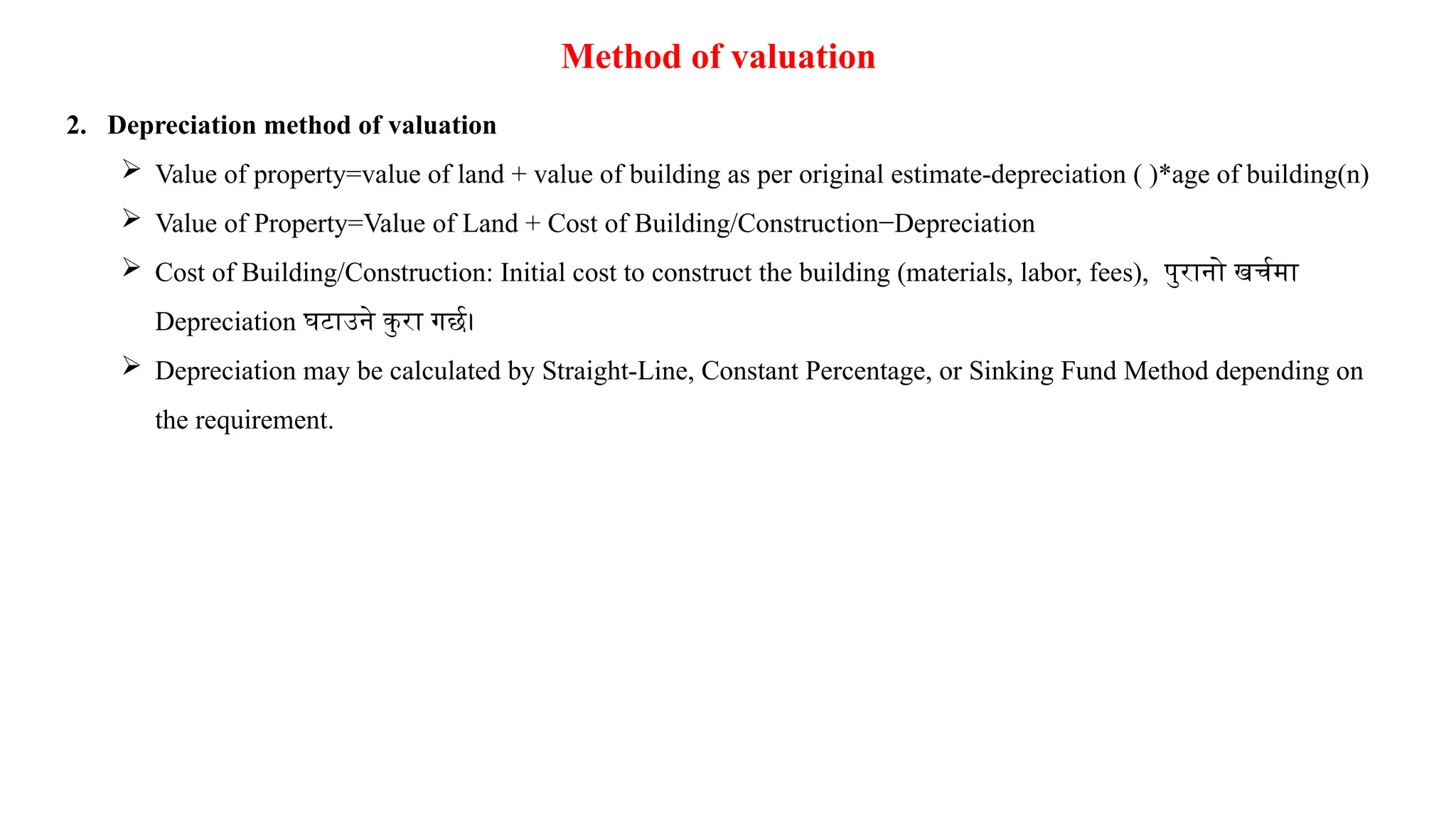

2.Depreciation method of valuation

Value of property=value of land + value of building as per original estimate-depreciation ( )*age of building(n)

Value of Property=Value of Land + Cost of Building/Construction−Depreciation

Cost of Building/Construction: Initial cost to construct the building (materials, labor, fees), पुरानो खर्चमा

Depreciation घटाउने कु रा गर्छ।

Depreciation may be calculated by Straight-Line, Constant Percentage, or Sinking Fund Method depending on

the requirement.

40.

Method of valuation

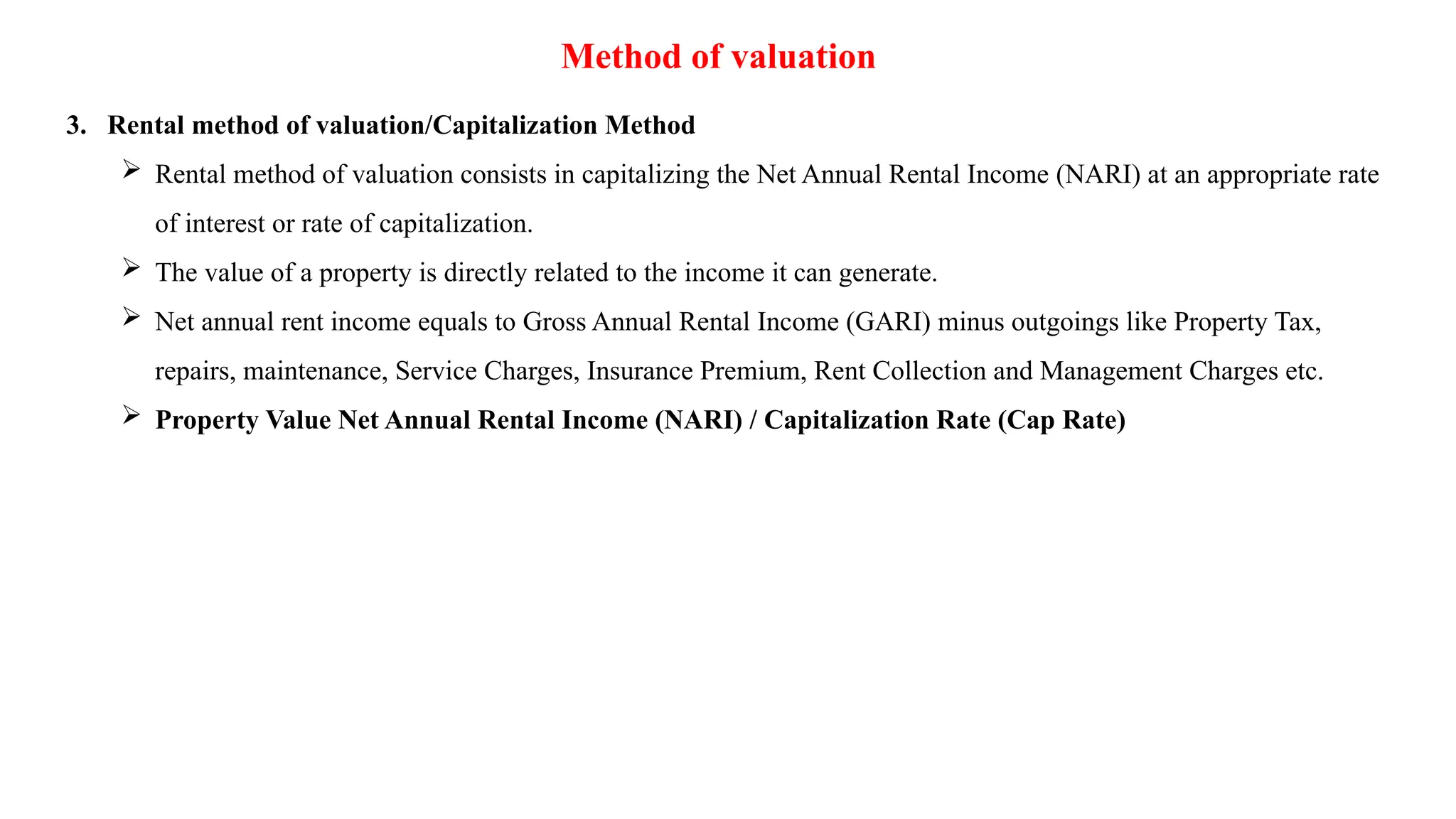

3.Rental method of valuation/Capitalization Method

Rental method of valuation consists in capitalizing the Net Annual Rental Income (NARI) at an appropriate rate

of interest or rate of capitalization.

The value of a property is directly related to the income it can generate.

Net annual rent income equals to Gross Annual Rental Income (GARI) minus outgoings like Property Tax,

repairs, maintenance, Service Charges, Insurance Premium, Rent Collection and Management Charges etc.

Property Value Net Annual Rental Income (NARI) / Capitalization Rate (Cap Rate)

41.

Method of valuation

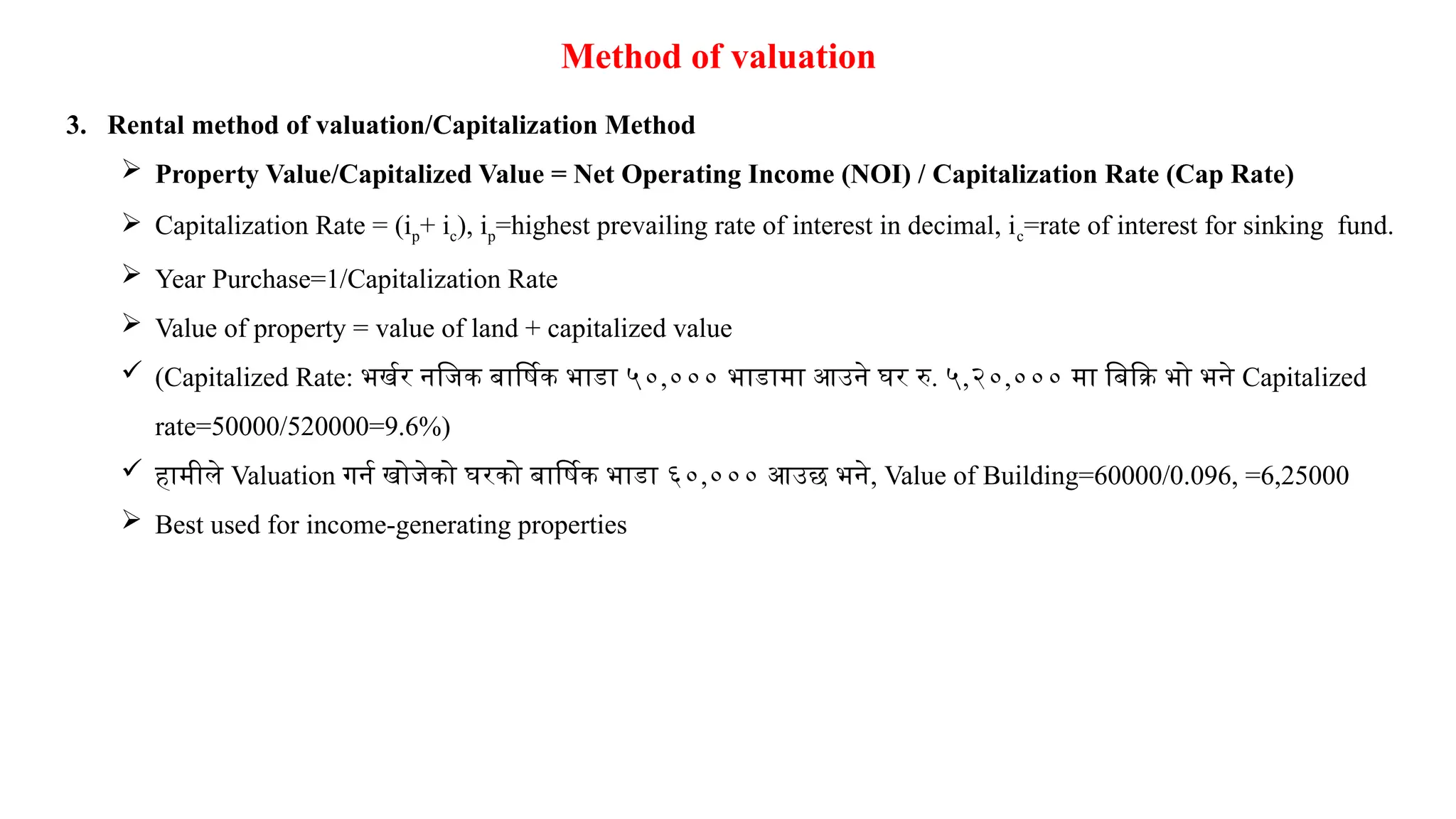

3.Rental method of valuation/Capitalization Method

Property Value/Capitalized Value = Net Operating Income (NOI) / Capitalization Rate (Cap Rate)

Capitalization Rate = (ip+ ic), ip=highest prevailing rate of interest in decimal, ic=rate of interest for sinking fund.

Year Purchase=1/Capitalization Rate

Value of property = value of land + capitalized value

(Capitalized Rate: भर्खर नजिक बार्षिक भाडा ५०,००० भाडामा आउने घर रु. ५,२०,००० मा बिक्रि भो भने Capitalized

rate=50000/520000=9.6%)

हामीले Valuation गर्न खोजेको घरको बार्षिक भाडा ६०,००० आउछ भने, Value of Building=60000/0.096, =6,25000

Best used for income-generating properties

42.

Method of valuation

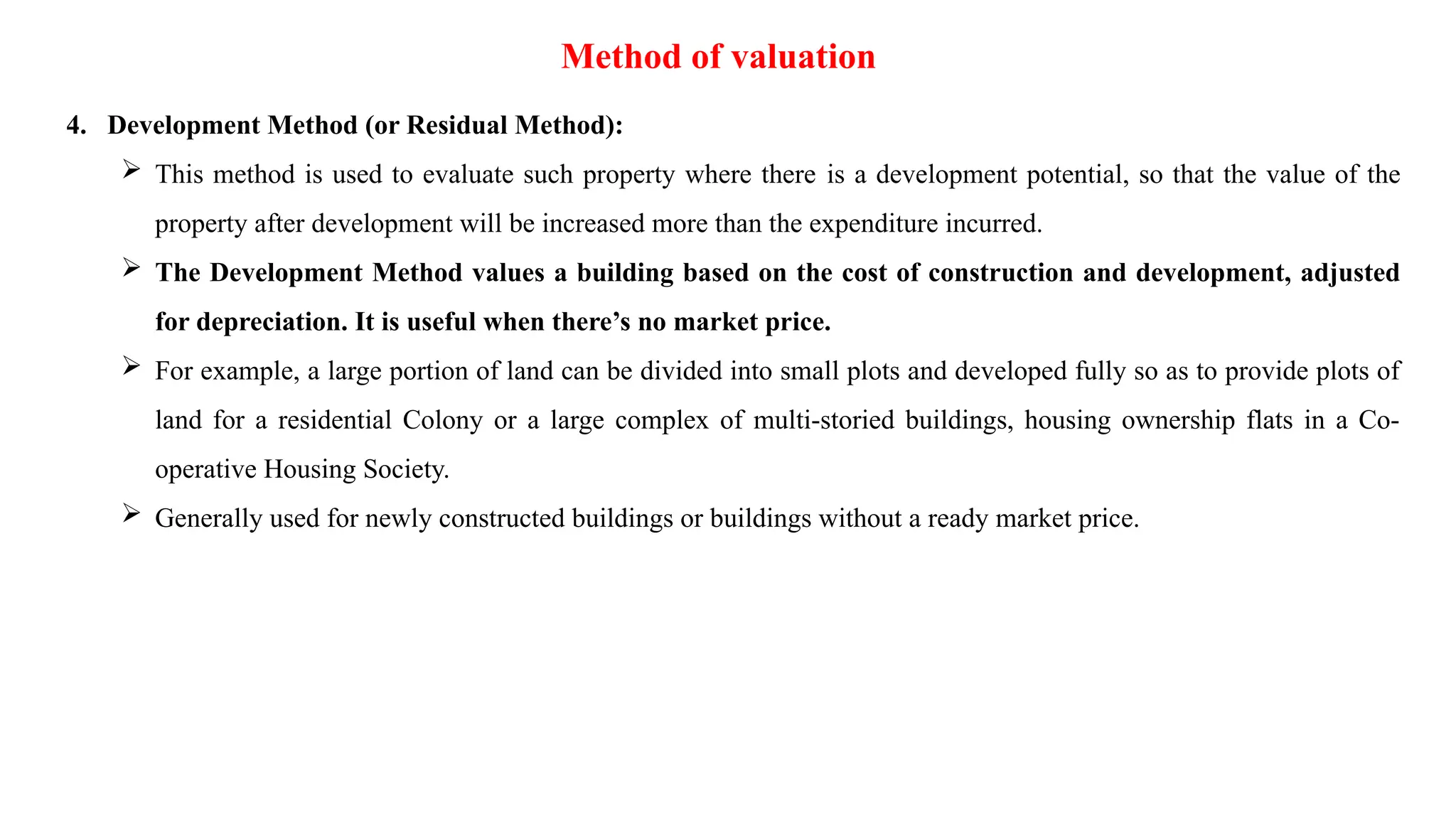

4.Development Method (or Residual Method):

This method is used to evaluate such property where there is a development potential, so that the value of the

property after development will be increased more than the expenditure incurred.

The Development Method values a building based on the cost of construction and development, adjusted

for depreciation. It is useful when there’s no market price.

For example, a large portion of land can be divided into small plots and developed fully so as to provide plots of

land for a residential Colony or a large complex of multi-storied buildings, housing ownership flats in a Co-

operative Housing Society.

Generally used for newly constructed buildings or buildings without a ready market price.

43.

Method of valuation

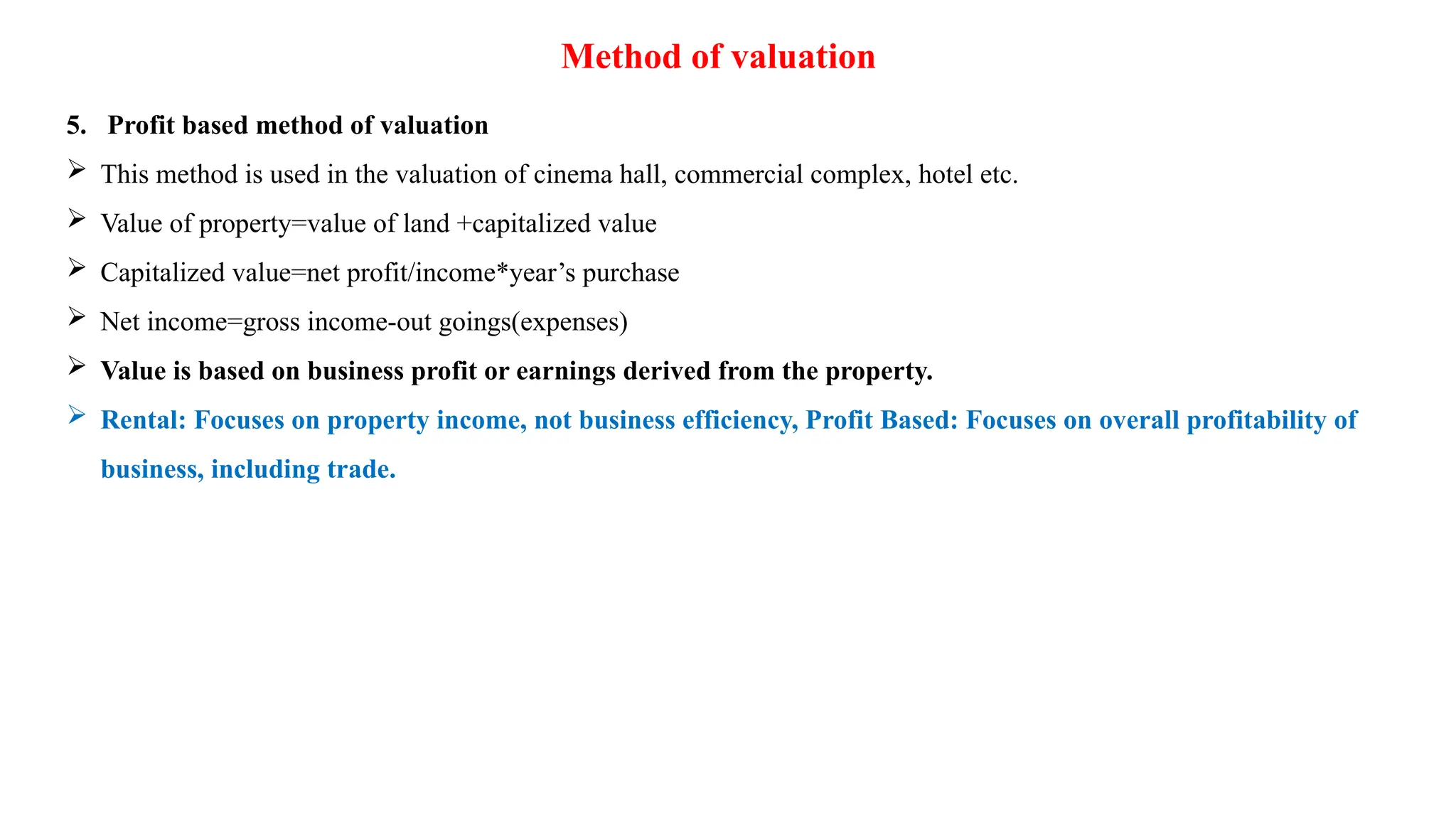

5.Profit based method of valuation

This method is used in the valuation of cinema hall, commercial complex, hotel etc.

Value of property=value of land +capitalized value

Capitalized value=net profit/income*year’s purchase

Net income=gross income-out goings(expenses)

Value is based on business profit or earnings derived from the property.

Rental: Focuses on property income, not business efficiency, Profit Based: Focuses on overall profitability of

business, including trade.

44.

Important Terminologies

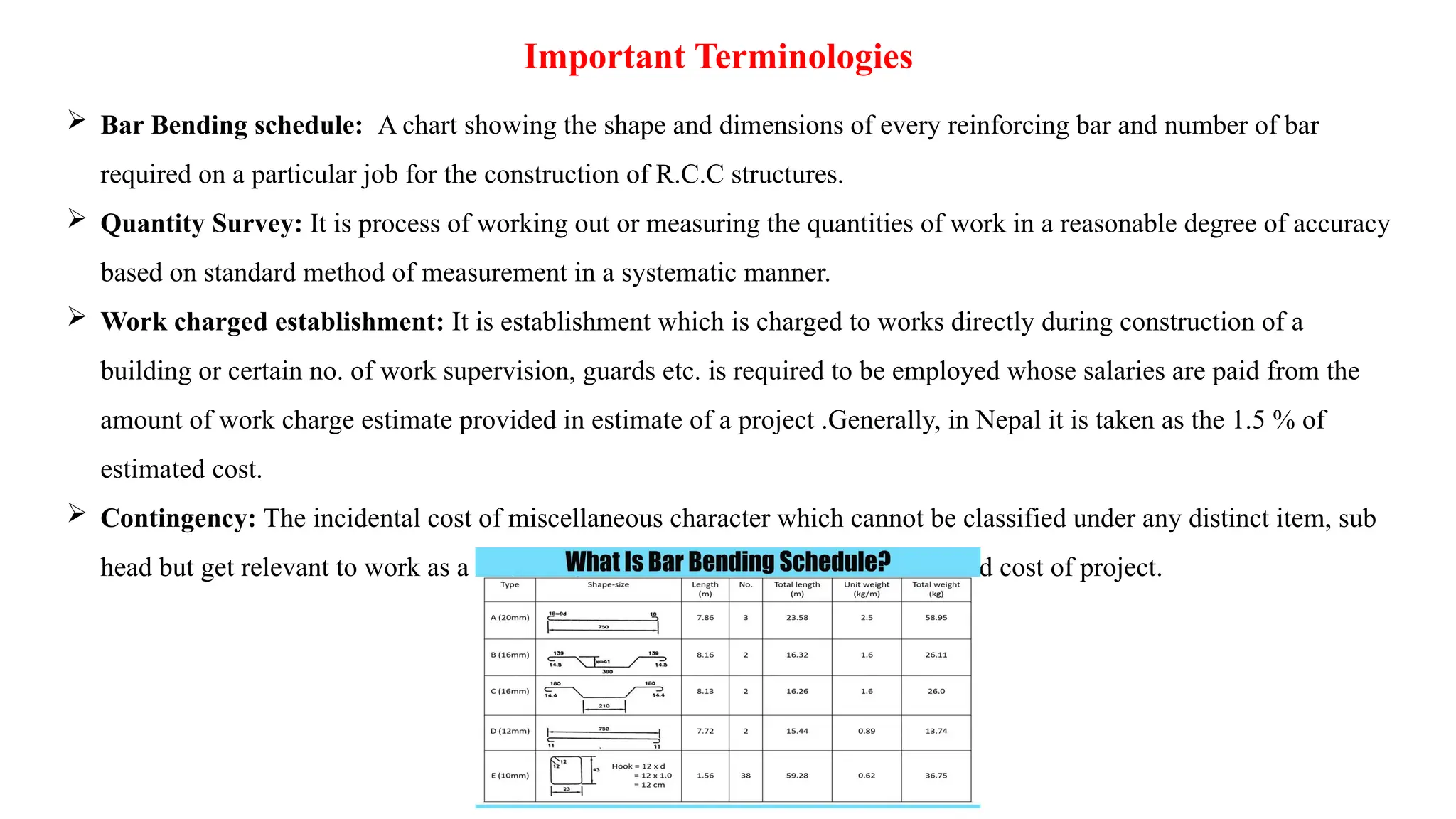

BarBending schedule: A chart showing the shape and dimensions of every reinforcing bar and number of bar

required on a particular job for the construction of R.C.C structures.

Quantity Survey: It is process of working out or measuring the quantities of work in a reasonable degree of accuracy

based on standard method of measurement in a systematic manner.

Work charged establishment: It is establishment which is charged to works directly during construction of a

building or certain no. of work supervision, guards etc. is required to be employed whose salaries are paid from the

amount of work charge estimate provided in estimate of a project .Generally, in Nepal it is taken as the 1.5 % of

estimated cost.

Contingency: The incidental cost of miscellaneous character which cannot be classified under any distinct item, sub

head but get relevant to work as a whole. In Nepal, it is taken as 3 % of estimated cost of project.

45.

Important Terminologies

Provisionalsum (PS): It is amount provided in estimate and bill of quantities for some special works whose details

and cost are not known at the time of the estimate and paid on actual basis.

Lump sum (LS): It is the amount provide based when details is not known but when output is known and paid as

BoQ item.

Value Added Tax (VAT): It is charge on taxable supplies of goods and services made in use in country by taxable

person and must pay the amount to board of customs and enterprises. For output tax, In Nepal, the VAT employed is

13 %.

Contract tax: It is the tax paid by the contractor upon the work done. In Nepal, the contract tax is taken as the 1.5%

of the paid bill.

Centage charge: It is the charge levied to other department for planning, designing, monitoring and supervision of

work. In Nepal, its value varies from 10% to 15% estimated cost.

46.

Important Terminologies

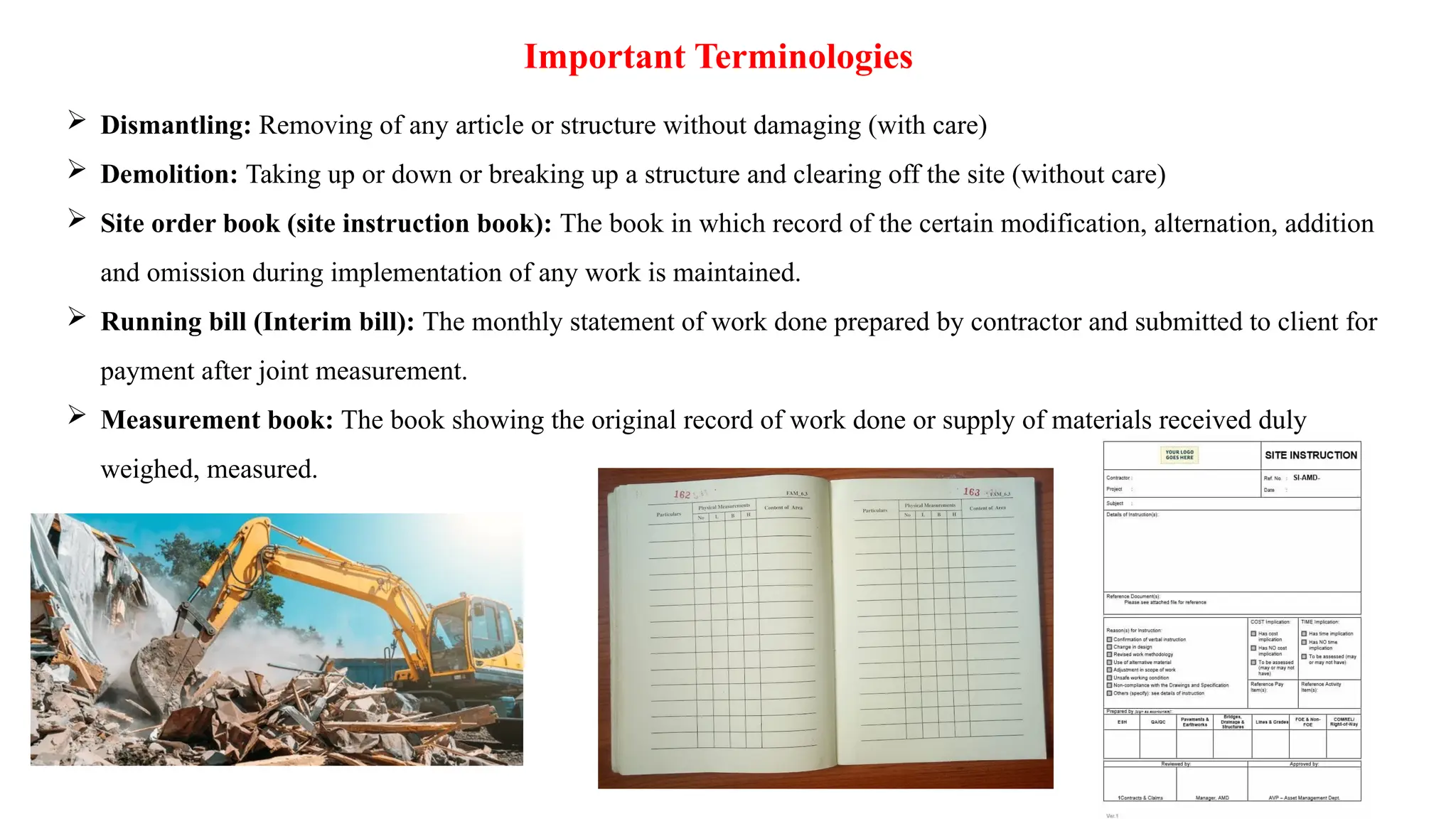

Dismantling:Removing of any article or structure without damaging (with care)

Demolition: Taking up or down or breaking up a structure and clearing off the site (without care)

Site order book (site instruction book): The book in which record of the certain modification, alternation, addition

and omission during implementation of any work is maintained.

Running bill (Interim bill): The monthly statement of work done prepared by contractor and submitted to client for

payment after joint measurement.

Measurement book: The book showing the original record of work done or supply of materials received duly

weighed, measured.

47.

Important Terminologies

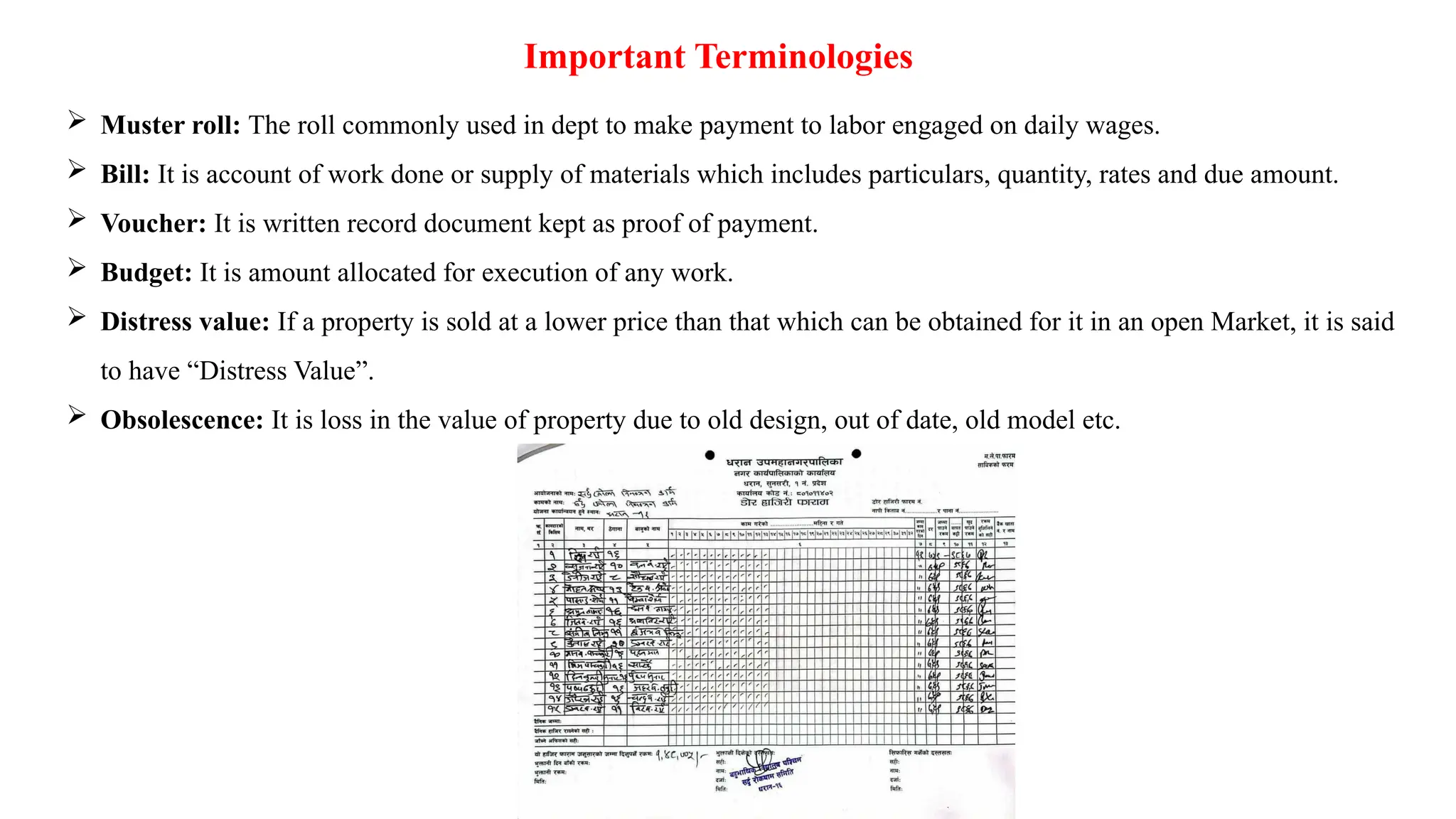

Musterroll: The roll commonly used in dept to make payment to labor engaged on daily wages.

Bill: It is account of work done or supply of materials which includes particulars, quantity, rates and due amount.

Voucher: It is written record document kept as proof of payment.

Budget: It is amount allocated for execution of any work.

Distress value: If a property is sold at a lower price than that which can be obtained for it in an open Market, it is said

to have “Distress Value”.

Obsolescence: It is loss in the value of property due to old design, out of date, old model etc.

48.

Important Terminologies

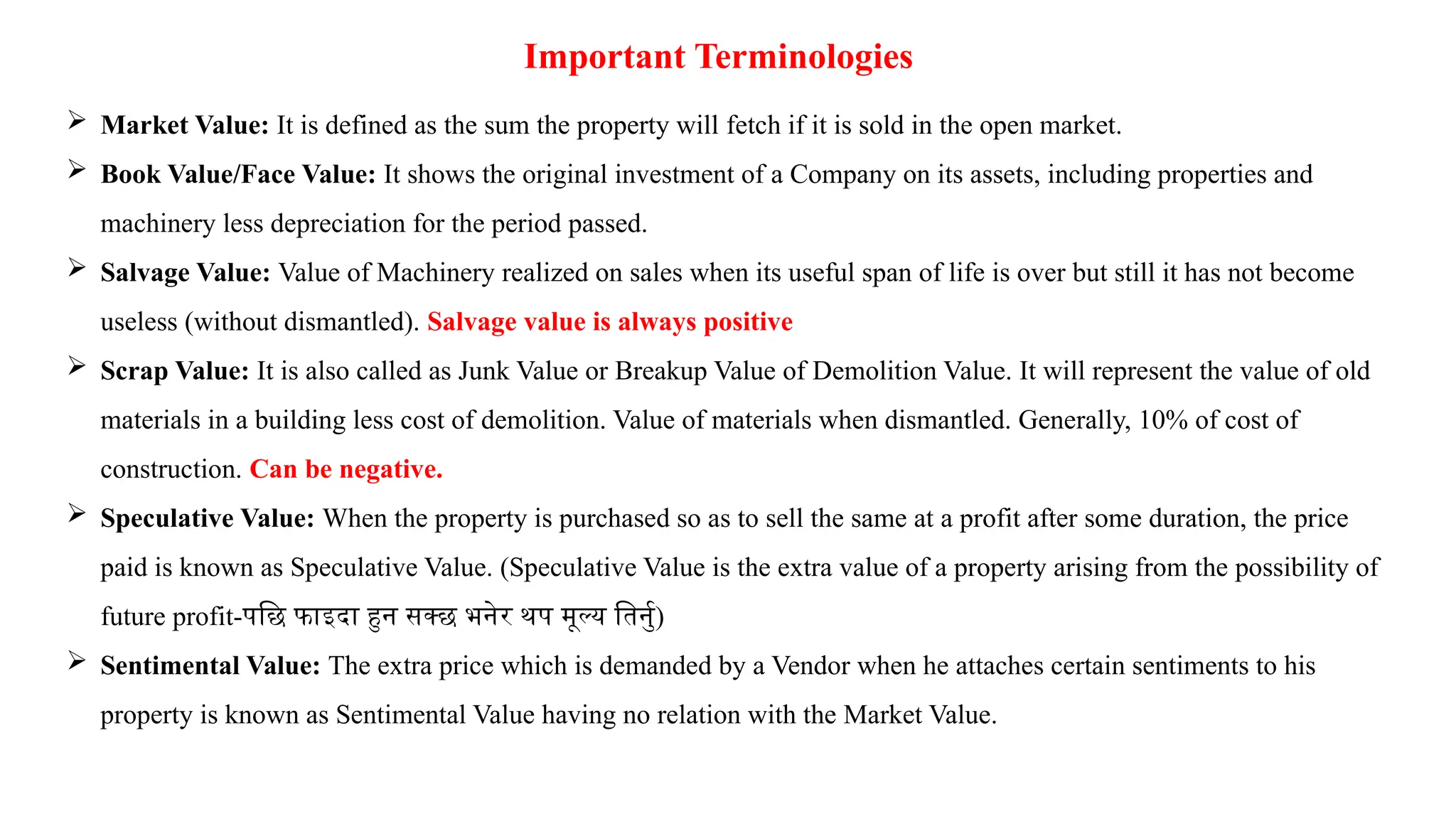

MarketValue: It is defined as the sum the property will fetch if it is sold in the open market.

Book Value/Face Value: It shows the original investment of a Company on its assets, including properties and

machinery less depreciation for the period passed.

Salvage Value: Value of Machinery realized on sales when its useful span of life is over but still it has not become

useless (without dismantled). Salvage value is always positive

Scrap Value: It is also called as Junk Value or Breakup Value of Demolition Value. It will represent the value of old

materials in a building less cost of demolition. Value of materials when dismantled. Generally, 10% of cost of

construction. Can be negative.

Speculative Value: When the property is purchased so as to sell the same at a profit after some duration, the price

paid is known as Speculative Value. (Speculative Value is the extra value of a property arising from the possibility of

future profit-पछि फाइदा हुन सक्छ भनेर थप मूल्य तिर्नु)

Sentimental Value: The extra price which is demanded by a Vendor when he attaches certain sentiments to his

property is known as Sentimental Value having no relation with the Market Value.

49.

Important Terminologies

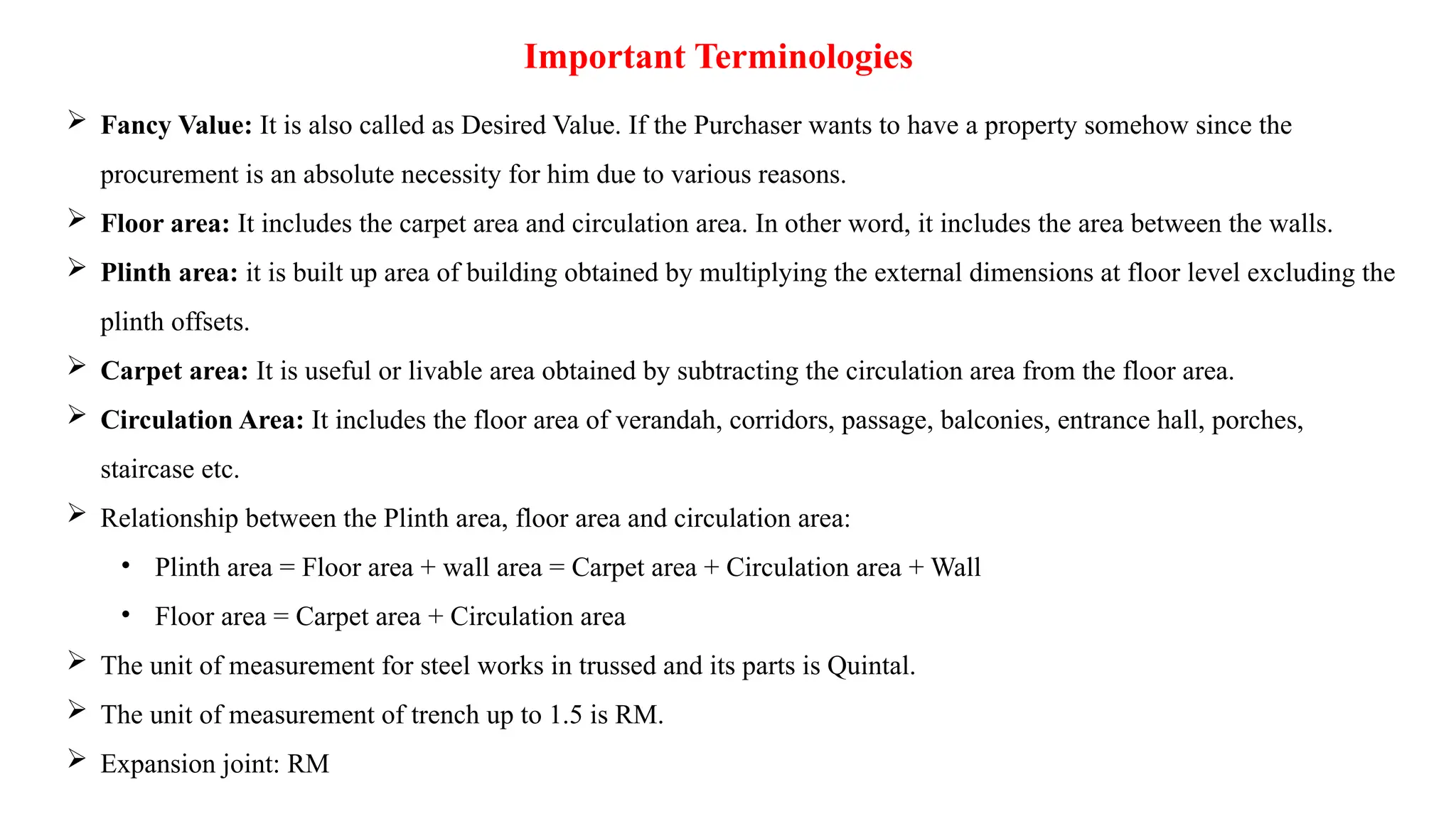

FancyValue: It is also called as Desired Value. If the Purchaser wants to have a property somehow since the

procurement is an absolute necessity for him due to various reasons.

Floor area: It includes the carpet area and circulation area. In other word, it includes the area between the walls.

Plinth area: it is built up area of building obtained by multiplying the external dimensions at floor level excluding the

plinth offsets.

Carpet area: It is useful or livable area obtained by subtracting the circulation area from the floor area.

Circulation Area: It includes the floor area of verandah, corridors, passage, balconies, entrance hall, porches,

staircase etc.

Relationship between the Plinth area, floor area and circulation area:

• Plinth area = Floor area + wall area = Carpet area + Circulation area + Wall

• Floor area = Carpet area + Circulation area

The unit of measurement for steel works in trussed and its parts is Quintal.

The unit of measurement of trench up to 1.5 is RM.

Expansion joint: RM

50.

Important Terminologies

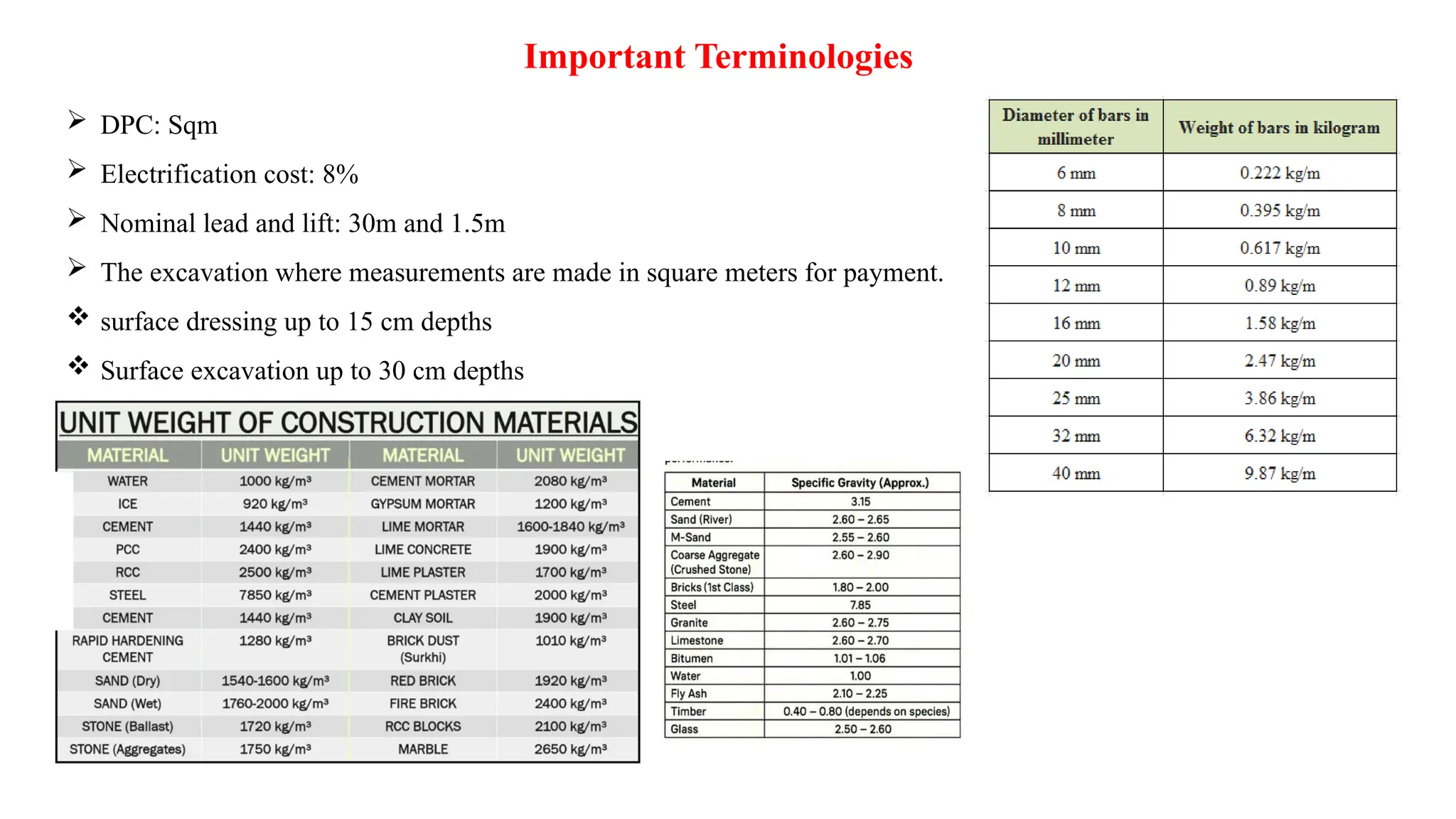

DPC:Sqm

Electrification cost: 8%

Nominal lead and lift: 30m and 1.5m

The excavation where measurements are made in square meters for payment.

surface dressing up to 15 cm depths

Surface excavation up to 30 cm depths

51.

Questions for Practices

•The most reliable estimate is

a. Detailed estimate b. Preliminary estimate

c. Plinth area estimate d. Cube rate estimate

• The floor area includes the area of the balcony up to

a. 50% b. 75% c. 100% d. 0%

• Berm are provided in canals if these are

a. partly in excavation and partly in embankment

b. partly in excavation and full in embankment

c. full in excavation and partly in embankment

d. full in excavation and full in embankment

• Total length of a cranked bar through a distance d at 45 degree in case of beam of effective length L is

a. L+2*0.42*d b. L+3*0.42*d c. L+5*0.42*d d. L+4*0.42*d

52.

Questions for Practices

•In long and short wall method of estimation, the length of long wall is the center-to-center distance between the walls

and

a. breadth of the wall b. half breadth of wall on each side

c. one fourth breadth of wall on each side d. None of these.

• The rent of house is generally

a. 6-10 % of cost of property. b. 6-15 % of cost of property.

c. 10-15 % of cost of property. d. 10-20 % of cost of property.

• The tentative cost of tools and plants on earthwork of excavation item in the governmental norms of rate analysis is

a. 3% of labour b. 3% of materials

c. 3% of construction cost d. 3% of income

• When the contractor fails to complete the work, an agency is employed to execute a part or whole of the work at the

cost of contractor. Such an agency is known as

a. creditable agency b. secondary agency

c. substitute agency d. debitable agency

• The two important types of specification commonly used are

a. initial and final b. material and item c. labour and item d. none

• In Nepal, the weightage given to the fair market value and governmental land value during the valuation of land is

a. 70% fair market value and 30% governmental land value

b. 30% fair market value and 70% governmental land value

c. 50% fair market value and 50% governmental land value

d. 40% fair market value and 60% governmental land value

![Norms of Government of Nepal for rate analysis

S.N

.

Work Specification DoR Norms Material Remarks

Skilled

Labor

Unskilled

Labor

3 PCC/RCC(1:1.5:3)

M20 per 15 m3

3 30 Cement 0.24

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.59

•Formwork @ 4 per cent on cost of concrete

i.e. cost of Material, Labor and Equipment

• For PCC Maximum Nominal Size 40mm,

for RCC 20mm Aggregate.

4 PCC (1:1:2) M25

per 15 m3

3 30 Cement 0.28

Sand 0.45

Aggregate 0.9

Total Loose for 1 Cum: 1.63

•Formwork @ 4 per cent on cost of concrete

i.e. cost of Material, Labor and Equipment

• For PCC Maximum Nominal Size 40mm,

for RCC 20mm Aggregate.

5 Reinforcement

Works [SS 2014]

(for 1 MT)

4 9 MS Bars 1.1

Binding Wire 8 Kg

10% for wastage.](https://image.slidesharecdn.com/7estimatingandcosting-251211152205-d571949c/75/7_Estimating-and-Costing-pptx-for-civil-engineering-24-2048.jpg)

![Preparation of Bill of Quantities (BoQs)

It is a statement showing the item number, description of work, unit of measurement, quantity, item rate (in fig. and

word) and amount in column is unfilled. It is filled by tenderer/bidder.

The BoQ after filled by the bidders is called priced BoQ.

Item

no.

Description of work Quantity Unit Rate Amount Remarks

Figures Words

1. Earthwork in excavation in

foundation with lifts 1.5 m

and lead 30 m in ordinary

soil. [SSRBW 900]

……… Cum

2. Providing and laying soling

brick on flat foundation

including sand blinding.

……….. Cum

To be filled by

bidder](https://image.slidesharecdn.com/7estimatingandcosting-251211152205-d571949c/75/7_Estimating-and-Costing-pptx-for-civil-engineering-31-2048.jpg)