The document provides an economic summary of Lebanon for the week of November 9-13, 2009. It includes indicators showing Lebanon's rankings in managing natural resources and remittances received. Global banks see positive economic and financial implications from the Lebanese government formation. The IMF calls for reforms to reduce fiscal vulnerabilities while noting the strength of the banking sector. Total Paris III commitments reached $5.7 billion with credit and debit cards reaching 1.6 million and ATMs totaling 1,181.

U.S. Companies Consider Vietnam the Most Attractive Destination in ASEAN. Four Vietnam hotels win recognition in Smart Travel Asia Poll. American golfer Bryan Saltus promotes Vietnam?s Sea Links golf course. Vietnam Airlines Cuts Domestic Fares by 50 Percent...

IPOS10 -t125 - Identification of Patient Reported Distress by Clinical Nurse ...Alex J Mitchell

This is a talk from IPOS 2010 on Identification of Patient Reported Distress by Clinical Nurse Specialists in Routine Oncology Practice: A Multicentre UK Study.

U.S. Companies Consider Vietnam the Most Attractive Destination in ASEAN. Four Vietnam hotels win recognition in Smart Travel Asia Poll. American golfer Bryan Saltus promotes Vietnam?s Sea Links golf course. Vietnam Airlines Cuts Domestic Fares by 50 Percent...

IPOS10 -t125 - Identification of Patient Reported Distress by Clinical Nurse ...Alex J Mitchell

This is a talk from IPOS 2010 on Identification of Patient Reported Distress by Clinical Nurse Specialists in Routine Oncology Practice: A Multicentre UK Study.

Cardiff09 - Detecting Depression in Primary & Secondary Care (May2009)Alex J Mitchell

Lecture for the University of Cardiff Psychiatry programme 2009. Topic is detecting depression - an evidence based approach. 86 slides; most self-explanatory but some slide labels added. Warning! can be a bit statistically heavy!

Netherlands to help promote Vietnam tourism image abroad. Sofitel Legend Metropole Hanoi won the PATA gold award 2010. Contest to seek new slogan for National Tourism Campaign. International Tourism Festival to be held with Hanoi’s millennial years. Vietnam Water Puppetry.....

This presentation summarizes the debate on net neutrality in the United States. It explains the concept, why it's important, and addresses the arguments for and against the concept.

This presentation was last given at the Bay Area Seniors Computer Club in Coos Bay, Oregon, on January 7, 2011.

Presentation at Tourism Industry and Education Symposium

March 5-7, 2009 in Jyväskylä, Finland

Innovative and Sustainable Products in the Tourism and Hospitality Business

http://www.jamk.fi/english/research/internationalevents/tie2009/mainpage

Dynamic Learning Maps: Geography Curriculum, skills and careersSimon Cotterill

Presentation including overview of a project to evaluate use of Dynamic Learning Maps in Geography at Newcastle University. Excludes the live demonstration but does include early formative evaluation.

Cardiff09 - Detecting Depression in Primary & Secondary Care (May2009)Alex J Mitchell

Lecture for the University of Cardiff Psychiatry programme 2009. Topic is detecting depression - an evidence based approach. 86 slides; most self-explanatory but some slide labels added. Warning! can be a bit statistically heavy!

Netherlands to help promote Vietnam tourism image abroad. Sofitel Legend Metropole Hanoi won the PATA gold award 2010. Contest to seek new slogan for National Tourism Campaign. International Tourism Festival to be held with Hanoi’s millennial years. Vietnam Water Puppetry.....

This presentation summarizes the debate on net neutrality in the United States. It explains the concept, why it's important, and addresses the arguments for and against the concept.

This presentation was last given at the Bay Area Seniors Computer Club in Coos Bay, Oregon, on January 7, 2011.

Presentation at Tourism Industry and Education Symposium

March 5-7, 2009 in Jyväskylä, Finland

Innovative and Sustainable Products in the Tourism and Hospitality Business

http://www.jamk.fi/english/research/internationalevents/tie2009/mainpage

Dynamic Learning Maps: Geography Curriculum, skills and careersSimon Cotterill

Presentation including overview of a project to evaluate use of Dynamic Learning Maps in Geography at Newcastle University. Excludes the live demonstration but does include early formative evaluation.

지난 토론회에서 다뤄진 네트워크 치과 문제는 오늘 토론회의 주제인 「서비스산업발전기본법」과 밀접하게 연관되어 있습니다. 환자를 유인하여 과잉진료 등 수익 극대화 위주의 진료, 환자 부담으로 이어지는 문제는 네트워크 병원의 한 사례는 의료를 상업적으로만 보는 문제를 단편적으로 보여주고 있습니다.

민주당 정책위원회가 주관하는 오늘 토론회는 보건의료 관점에서 「서비스산업발전기본법」 의 문제점을 짚어보고 여러 보건의료 단체들과 대안을 고민하기 위하여 마련되었습니다. 보건복지위원으로 의료의 영리 문제에 대해 늘 고민하시고 함께 애써주신 김용익 의원님께 감사드립니다.

교육, 복지 그리고 의료는 ‘산업’이 아니라 ‘공공성’ 차원에서 접근해야 합니다. 그러나 「서비스산업발전기본법」은 1, 2차 산업을 제외한 모든 분야를 서비스산업으로 규정하여 앞으로 공공성에 대한 침해 논란이 끊임없이 제기될 수 있습니다.

특히 우리나라 같이 공공의료가 절대적으로 부족한 상황에서 ‘보건의료’가 서비스산업의 범주에 포함될 경우 투자개방형 의료법인, 메디텔 설립, 영리병원, 건강관리서비스 기관의 영리기업화 허용 등 의료의 상업화, 시장화는 시간문제입니다. 이미 원격의료를 허용하자는 의료법 개정안도 입법예고되어 있지 않습니까?

저는 지난 10월, 기회재정부 국정감사에서 이러한 「서비스산업발전기본법」에 대한 문제점을 지적한 바 있습니다.

오늘 토론회는 의료를 공공성으로 볼 것이냐? 산업적으로 육성시킬 것이냐? 하는 정부의 정책 방향에 우려와 준엄한 경고를 하는 큰 계기가 되는 자리라고 생각합니다.

발제를 해주실 우석균 보건의료단체연합 정책실장님, 토론자로 참석해 주신 송형곤 대한의사협회 상근 부회장님, 김철신 대한치과의사협회 정책이사님, 김대원 대한약사회 부회장님, 김지호 대한한의사협회 기획이사님, 김준현 건강세상네트워크 정책실장님, 강종석 기획재정부 서비스경제과장님께 감사드립니다.

김용익 의원님과 함께 「서비스산업발전기본법」이 가진 문제점에 뜻을 같이하고 의료의 공공성이 강화되는 정책방향으로 이끌기 위한 최선의 노력을 다하겠습니다.

9월 11일 오전 10시, 국회도서관 대강당에서 이미경·김현미의원실 주최, 민주당 을지로위원회 후원으로 ‘공공 건설공사 분할·분리발주 제도화’를 위한 국가계약법 개정 토론회가 열린다.

건설 하도급 시장은 원도급자에 의한 부당한 단가후려치기, 대금 지연지급, 부당한 특약 등 고질적인 불법·불공정행위가 여전히 개선되고 있지 못하다.

이에 기존 하도급방식의 공사수행에 대한 근본적인 전환을 위해 공공부문의 건설공사 계약 체결시 전문건설사가 종합건설사를 거치지 않고 직접 건설공사를 수주할 기회를 확대하는 ‘분리발주 의무화’가 해결책으로 제시되어 왔다.

지난 5월말 정부는 ‘박근혜정부 국정과제’를 발표하면서 창조경제 추진전략 중 ‘중소기업 성장 희망사다리 구축’을 위해 중소기업 참여기회 확대 차원에서 ‘대규모 계약의 분할·분리발주 법제화’제시하였는데, 이는 지난 대선 당시 박근혜후보가 내걸었던 공약(2012.11)과 대통령직인수위원회가 지난 2월 발표한 ‘공약 이행 로드맵 및 입법 추진계획’의 ‘분리발주 법제화’를 국정과제로 담아낸 것이다.

그러나 최근 정부와 새누리당은 분리발주의 부작용(하자책임 불분명 등)을 이유로 기존 통합발주원칙 유지를 고수하기로 결정하면서 분리발주 법제화 추진을 중단하였다.

이에 민주당 이미경의원실·김현미의원실은 건설업계 ‘乙 ’지키기 제도 개선 차원에서 불법·불공정거래행위를 근절을 위한 대책을 마련하고자 각계 전문가들과 함께 토론회를 개최합니다.

Публичный доклад заведующей муниципального дошкольного образовательного учреждения детский сад «Берёзка» п.им.М.Горького Соловьёвой Анны Ивановны 2015 г.

International Trade Compliance Strategy Responsibility MatrixGHY International

A quick reference tool that supports the white paper, The Case for an Integrated Trade Compliance Strategy. It shows a road map of relationships, owners, and tasks that are intertwined when an organization is active in international trade. This road map can assist an organization to benchmark their current practice versus that proposed with an Integrated Trade Strategy.

Social Media presentation on digital branding from Social Media speaker and trainer Dawn Raquel Jensen of Virtual Options Coaching & Training. @virtualoptions , @dawnrjensen

For more information about Dawn visit http://www.dawnonfacebook.com or http://www.dawnraqueljensen.com

Moodle 2.0 themes; Pieter van der Hijden; Sofos Consultancy, 2011. Overview of the standard Moodle 2.0 themes and the parameters accessible for system administrators.

What price will pi network be listed on exchangesDOT TECH

The rate at which pi will be listed is practically unknown. But due to speculations surrounding it the predicted rate is tends to be from 30$ — 50$.

So if you are interested in selling your pi network coins at a high rate tho. Or you can't wait till the mainnet launch in 2026. You can easily trade your pi coins with a merchant.

A merchant is someone who buys pi coins from miners and resell them to Investors looking forward to hold massive quantities till mainnet launch.

I will leave the telegram contact of my personal pi vendor to trade with.

@Pi_vendor_247

What website can I sell pi coins securely.DOT TECH

Currently there are no website or exchange that allow buying or selling of pi coins..

But you can still easily sell pi coins, by reselling it to exchanges/crypto whales interested in holding thousands of pi coins before the mainnet launch.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and resell to these crypto whales and holders of pi..

This is because pi network is not doing any pre-sale. The only way exchanges can get pi is by buying from miners and pi merchants stands in between the miners and the exchanges.

How can I sell my pi coins?

Selling pi coins is really easy, but first you need to migrate to mainnet wallet before you can do that. I will leave the telegram contact of my personal pi merchant to trade with.

Tele-gram.

@Pi_vendor_247

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

US Economic Outlook - Being Decided - M Capital Group August 2021.pdfpchutichetpong

The U.S. economy is continuing its impressive recovery from the COVID-19 pandemic and not slowing down despite re-occurring bumps. The U.S. savings rate reached its highest ever recorded level at 34% in April 2020 and Americans seem ready to spend. The sectors that had been hurt the most by the pandemic specifically reduced consumer spending, like retail, leisure, hospitality, and travel, are now experiencing massive growth in revenue and job openings.

Could this growth lead to a “Roaring Twenties”? As quickly as the U.S. economy contracted, experiencing a 9.1% drop in economic output relative to the business cycle in Q2 2020, the largest in recorded history, it has rebounded beyond expectations. This surprising growth seems to be fueled by the U.S. government’s aggressive fiscal and monetary policies, and an increase in consumer spending as mobility restrictions are lifted. Unemployment rates between June 2020 and June 2021 decreased by 5.2%, while the demand for labor is increasing, coupled with increasing wages to incentivize Americans to rejoin the labor force. Schools and businesses are expected to fully reopen soon. In parallel, vaccination rates across the country and the world continue to rise, with full vaccination rates of 50% and 14.8% respectively.

However, it is not completely smooth sailing from here. According to M Capital Group, the main risks that threaten the continued growth of the U.S. economy are inflation, unsettled trade relations, and another wave of Covid-19 mutations that could shut down the world again. Have we learned from the past year of COVID-19 and adapted our economy accordingly?

“In order for the U.S. economy to continue growing, whether there is another wave or not, the U.S. needs to focus on diversifying supply chains, supporting business investment, and maintaining consumer spending,” says Grace Feeley, a research analyst at M Capital Group.

While the economic indicators are positive, the risks are coming closer to manifesting and threatening such growth. The new variants spreading throughout the world, Delta, Lambda, and Gamma, are vaccine-resistant and muddy the predictions made about the economy and health of the country. These variants bring back the feeling of uncertainty that has wreaked havoc not only on the stock market but the mindset of people around the world. MCG provides unique insight on how to mitigate these risks to possibly ensure a bright economic future.

how can i use my minded pi coins I need some funds.DOT TECH

If you are interested in selling your pi coins, i have a verified pi merchant, who buys pi coins and resell them to exchanges looking forward to hold till mainnet launch.

Because the core team has announced that pi network will not be doing any pre-sale. The only way exchanges like huobi, bitmart and hotbit can get pi is by buying from miners.

Now a merchant stands in between these exchanges and the miners. As a link to make transactions smooth. Because right now in the enclosed mainnet you can't sell pi coins your self. You need the help of a merchant,

i will leave the telegram contact of my personal pi merchant below. 👇 I and my friends has traded more than 3000pi coins with him successfully.

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

How to get verified on Coinbase Account?_.docxBuy bitget

t's important to note that buying verified Coinbase accounts is not recommended and may violate Coinbase's terms of service. Instead of searching to "buy verified Coinbase accounts," follow the proper steps to verify your own account to ensure compliance and security.

how to sell pi coins in South Korea profitably.DOT TECH

Yes. You can sell your pi network coins in South Korea or any other country, by finding a verified pi merchant

What is a verified pi merchant?

Since pi network is not launched yet on any exchange, the only way you can sell pi coins is by selling to a verified pi merchant, and this is because pi network is not launched yet on any exchange and no pre-sale or ico offerings Is done on pi.

Since there is no pre-sale, the only way exchanges can get pi is by buying from miners. So a pi merchant facilitates these transactions by acting as a bridge for both transactions.

How can i find a pi vendor/merchant?

Well for those who haven't traded with a pi merchant or who don't already have one. I will leave the telegram id of my personal pi merchant who i trade pi with.

Tele gram: @Pi_vendor_247

#pi #sell #nigeria #pinetwork #picoins #sellpi #Nigerian #tradepi #pinetworkcoins #sellmypi

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Even tho Pi network is not listed on any exchange yet.

Buying/Selling or investing in pi network coins is highly possible through the help of vendors. You can buy from vendors[ buy directly from the pi network miners and resell it]. I will leave the telegram contact of my personal vendor.

@Pi_vendor_247

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

how to swap pi coins to foreign currency withdrawable.

419 ltw 142

1. Issue 142

November 9-13, 2009 Economic Research & Analysis Department

LEBANON THIS WEEK

In This Issue Charts of the Week

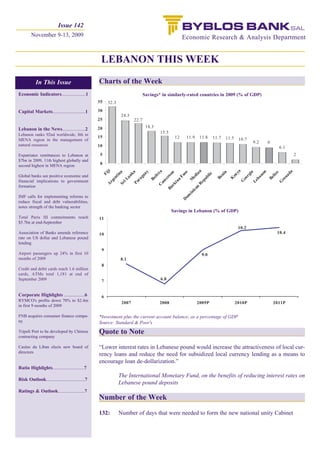

Economic Indicators....................1 Savings* in similarly-rated countries in 2009 (% of GDP)

35 32.3

Capital Markets...........................1 30

24.3

25 22.7

20 18.3

Lebanon in the News...................2

Lebanon ranks 92nd worldwide, 8th in

15.5

15 12 11.9 11.8 11.7 11.5

MENA region in the management of 10.7

9.2 9

natural resources 10 6.1

Expatriates remittances to Lebanon at 5 2

$7bn in 2009, 11th highest globally and

second highest in MENA region 0

ji

ya

n

ia

da

ay

n

a

ka

a

n

so

n

e

Fi

ia

no

lic

tin

gi

liz

ni

oo

liv

en

Global banks see positive economic and

Fa

gu

na

an

ed

r

Be

ub

ba

Be

er

en

eo

K

Bo

ra

re

M

iL

a

financial implications to government

ep

am

Le

rg

G

in

G

Pa

Sr

R

A

rk

C

formation

an

Bu

ic

in

om

IMF calls for implementing reforms to

D

reduce fiscal and debt vulnerabilities,

notes strength of the banking sector

Savings in Lebanon (% of GDP)

Total Paris III commitments reach 11

$5.7bn at end-September

10.2

Association of Banks amends reference 10 10.4

rate on US dollar and Lebanese pound

lending

9

Airport passengers up 24% in first 10 9.0

months of 2009 8.1

8

Credit and debit cards reach 1.6 million

cards, ATMs total 1,181 at end of

September 2009 7 6.8

Corporate Highlights .................6 6

RYMCO's profits down 70% to $2.4m

2007 2008 2009P 2010P 2011P

in first 9 months of 2009

FNB acquires consumer finance compa- *Investment plus the current account balance, as a percentage of GDP

ny Source: Standard & Poor's

Tripoli Port to be developed by Chinese Quote to Note

contracting company

Casino du Liban elects new board of “Lower interest rates in Lebanese pound would increase the attractiveness of local cur-

directors

rency loans and reduce the need for subsidized local currency lending as a means to

encourage loan de-dollarization.”

Ratio Highlights..........................7

The International Monetary Fund, on the benefits of reducing interest rates on

Risk Outlook................................7

Lebanese pound deposits

Ratings & Outlook......................7

Number of the Week

132: Number of days that were needed to form the new national unity Cabinet

2. Economic Indicators

$m (unless otherwise mentioned) 2007 Aug 08 2008 June 09 July 09 Aug 09 % Change*

Exports 2,816 283 3,478 249 230 239 (15.55)

Imports 11,815 1,417 16,133 1,551 1,470 1,439 1.55

Trade Balance (8,999) (1,134) (12,655) (1,302) (1,240) (1,200) 5.82

Balance of Payments 2,036 402 3,462 443 1,246 1,020 153.73

Checks Cleared in LBP 8,409 773 9,350 873 1,028 937 21.22

Checks Cleared in FC 29,893 4,282 43,174 3,658 4,115 4,233 (1.14)

Total Checks Cleared 38,302 5,055 52,524 4,531 5,143 5,170 2.27

Budget Deficit/Surplus (2,546) (247) (2,921) (151) (157) (127) (48.58)

Primary Balance 731 (26) 597 161 136 121 (565.38)

Airport Passengers 3,408,834 547,237 4,085,334 460,223 621,522 612,956 12.01

$bn (unless otherwise mentioned) Dec. 2007 Aug 2008 May 09 June 09 July 09 Aug 09 % Change*

BdL FX Reserves 9.78 15.13 20.22 20.62 22.01 22.82 50.83

In months of Imports 9.19 10.67 16.28 13.29 14.97 15.86 48.64

Public Debt 42.03 45.35 47.75 47.33 47.92 48.51 6.97

Net Public Debt 39.03 40.69 42.79 42.98 43.05 43.24 6.27

Bank Assets 82.26 90.70 101.65 103.62 105.38 107.37 18.38

Bank Deposits (Private Sector) 67.29 75.00 84.35 85.78 87.69 89.30 19.07

Bank Loans to Private Sector 20.42 24.77 26.07 26.07 26.98 27.11 9.45

Money Supply M2 16.47 20.28 28.15 29.07 30.11 30.91 52.42

Money Supply M3 59.83 66.14 73.58 74.68 76.17 77.22 16.75

LBP Lending Rate (%) 10.10 9.96 9.79 9.76 9.43 9.27 (69b.p.)

LBP Deposit Rate (%) 7.40 7.23 7.06 6.96 7.02 7.00 (23b.p.)

USD Lending Rate (%) 8.02 7.17 7.28 7.24 7.24 7.05 (12b.p.)

USD Deposit Rate (%) 4.69 3.55 3.22 3.18 3.19 3.18 (37b.p.)

%* Change in CPI** 5.92 13.52 1.88 3.31 2.42 1.52 (1,200b.p.)

* Year-on-Year; ** Consumer Price Index

Note: b.p. i.e. basis point

Sources: ABL, BdL

Capital Markets

Most Traded Last Price % Change* Total Weight in Sovereign Coupon Mid Price Mid Yield

Stocks on BSE ($) Volume Market Eurobonds % $ %

Capitalization

Solidere "A" 25.48 (5.59) 768,577 20.50% Mar. 2010 7.125 101.44 2.28

Solidere "B" 25.25 (6.45) 403,793 13.20% May 2011 7.875 106.25 3.58

Byblos Common 2.01 (1.47) 127,802 3.51% Mar. 2012 7.500 107.00 4.32

Byblos Priority 2.02 0.00 156,959 3.35% Sep. 2012 7.750 108.38 4.53

Byblos Pref. 08 100.00 0.50 750 1.61% June 2013 8.625 111.38 5.12

BLOM GDR 88.85 0.28 1,760 5.28% Apr. 2015 10.000 116.88 6.29

BLOM Listed 85.00 0.00 0 14.70% Jan. 2016 8.500 111.25 6.27

Audi GDR 84.60 (2.76) 5,930 6.69% May 2016 11.625 126.25 6.59

Audi Listed 75.00 0.00 173,732 20.63% Mar. 2017 9.000 115.13 6.38

HOLCIM 13.02 (3.56) 2,671 2.04% Apr. 2021 8.250 111.00 6.84

Source: Beirut Stock Exchange (BSE); *Week-on-week Source: Byblos Capital Markets

This Week Last Week % Change October 2009 October 2008 % Change

Total Shares Traded 1,780,207 1,370,795 29.87 4,968,999 14,251,997 (65.13)

Total Value Traded $46,991,002 $31,779,627 47.61 $103,486,832 $129,604,201 (20.15)

Market Capitalization $12.43bn $12.73bn (2.35) $12.60bn $11.69bn 7.77

Source: Beirut Stock Exchange (BSE)

LEBANON THIS WEEK November 9-13, 2009

1

3. Lebanon in the News

Lebanon ranks 92nd worldwide, 8th in MENA region in the man-

agement of natural resources

The 2009 Natural Resources Management Index in 216 countries ranked Natural Resources Management Index

Lebanon in 92nd place worldwide and 8th among 17 countries in the Middle Rankings & Scores

East and North Africa region. Lebanon came in 57th place globally and in 5th MENA Global

place regionally in the 2008 survey. Lebanon also ranked in 23rd place among Country Score Rank Rank

30 Upper Middle Income countries (UMICs) included in the current survey. Israel 94.4 1 27

The index measures a country's economic policies that promote the sustain- Jordan 92.4 2 33

able management of natural resources. It is intended to reflect whether gov- Oman 89.7 3 47

ernments are investing limited resources in ways that will increase economic Iran 85.8 4 58

growth, reduce poverty, and improve natural resource management. It is based Algeria 85.1 5 60

on four sub-indices that cover eco-region protection, access to improved Egypt 79.7 6 77

water, access to improved sanitation, and child mortality. Each category is Qatar 75.7 7 90

rated on a scale from zero to 100, with the overall index calculated as the sim- Lebanon 75.4 8 92

ple average of the four sub-indices. The index is issued by Columbia and Yale UAE 74.0 9 103

universities. Libya 73.5 10 107

Tunisia 72.4 11 110

Globally Lebanon ranked ahead of Mongolia, French Polynesia and Syria 71.4 12 112

Zimbabwe and came behind Nicaragua, Malawi and Yugoslavia. It also Morocco 70.6 13 115

ranked ahead of Turkey and Uruguay and came behind Grenada and Romania Iraq 61.9 14 131

among UMICs. Lebanon received a score of 75.4 points, below the global and Djibouti 57.0 15 142

UMICs averages of 75.7 points and 85.1 points respectively, but above the Sudan 52.9 16 154

MENA and Arab averages of 74.2 points and 72.1 points respectively. On a Yemen 49.2 17 158

global basis, Lebanon's rank regressed by 35 spots, while its score decreased Source: Columbia & Yale universities, Byblos Research

by 14.1% from the 2008 survey.

Lebanon shared first place with 41 other countries including Canada, France, Switzerland, Germany, Japan and Luxembourg and

ranked ahead of the United States on the Access to Improved Water Sub-Index. This component measures the percentage of the pop-

ulation with access to at least 20 liters of water per person per day from an 'improved' source within one kilometer of residency. It also

tied with Czech Republic, Hungary, Uruguay and Mauritius and ranked ahead of Croatia, Malaysia and Latvia among UMICs in this

category.

Further, Lebanon came ahead of Sri Lanka, Tonga and Philippines and behind Vietnam, Dominican Republic and Thailand on the Child

Mortality Sub-Index, which measures the probability of a child dying between the ages of 1 and 4 years. It also ranked ahead of Belize

and Turkey and came behind Russia and Mexico among UMICs. Finally, Lebanon ranked ahead of Afghanistan, Bosnia Herzegovina

and French Polynesia and behind Mauritania, Somalia and Ireland on the Eco-Region Protection Sub-Index. The indicator assesses the

comprehensiveness of a government's commitment to habitat preservation and biodiversity protection. It also came ahead of Uruguay

and Barbados and behind Saint Kitts and Nevis and Turkey among UMICs. Lebanon's score on the Access to Improved Sanitation sub-

index was not available.

Components of the 2009 Natural Resources Management Index for Lebanon

Global MENA UMICs

Global MENA UMICs Lebanon Average Average Average

Category Rank Rank Rank Score Score Score Score

Access to Improved Water 1 1 1 100.0 84.4 89.4 94.6

Child Mortality 92 10 21 97.2 87.9 93.5 94.7

Eco-Region Protection 199 11 28 4.4 61.2 32.2 65.8

Source: Columbia & Yale universities, Byblos Research

LEBANON THIS WEEK November 9-13, 2009

2

4. Lebanon in the News

Expatriates remittances to Lebanon at $7bn in 2009, 11th highest

globally and second highest in MENA region

The World Bank estimated remittance inflows to Lebanon at $7bn in 2009, Remittance Inflows to MENA Countries in 2009

constituting a decrease of 2.5% from $7.2bn in 2008 and compared to $5.8bn Global

in 2007 and $5.2bn in 2006. Further, the Bank revised upward its earlier esti- Country US$m Rank % of GDP*

mate of $6bn for remittance inflows in 2008. Globally, Lebanon was the 16th Egypt 7,800 14 5.3%

largest recipient of remittances, and the 11th largest recipient among develop- Lebanon 7,000 16 25.1%

ing economies, ranking ahead of Vietnam, Indonesia and Morocco, and com- Morocco 5,720 19 8.0%

ing immediately behind Egypt, Romania and Poland. Lebanon was the second Jordan 3,650 28 19.0%

largest recipient among 12 countries in the MENA region included in the sur- Algeria 2,193 46 1.3%

vey, coming behind Egypt. Further, Lebanon was the fourth largest recipient Tunisia 1,860 50 4.7%

of remittances among 36 Upper Middle Income Countries (UMICs) covered Yemen 1,413 60 5.3%

by the survey. It ranked ahead of Russia, Hungary and Malaysia, and came Iran 1,072 69 0.3%

behind Romania, Poland and Mexico. Lebanon's 2009 rankings were Syria 827 72 1.5%

unchanged regionally and among UMICs from the previous year. West Bank 630 81 n/a

Djibouti 30 136 3.5%

Remittances to Lebanon account for 21.7% of total remittance flows to the Libya 16 142 0.0%

MENA region in 2009 compared to 20.7% in 2008 and 18.4% in 2007. They *for 2008

account for 10.3% of remittance inflows to UMICs in 2009 relative to 9.4% in Source: World Bank, Byblos Research

2008 and 8% in 2007, while they represent 2.2% of aggregate remittances to

developing economies this year, almost unchanged from 2.1% in 2008 and 2% in 2007. Further, remittance inflows to Lebanon account

for 1.7% of the global inflow of remittances in 2009, almost unchanged from 1.6% in 2008 and 1.5% in 2007. Also, the 2.5% project-

ed decline of remittances to Lebanon for 2009 is lower than the 7.2% decline in inflows to the MENA region, the 6% decline for devel-

oping countries and the 11% decrease for UMICs this year. In parallel, the World Bank estimated expatriates' remittances to Lebanon

to be equivalent to 25.1% of GDP in 2008, the 7th highest such ratio in the world behind Samoa, Lesotho, the Kyrgyz Republic,

Moldova, Tonga and Tajikistan, as well as the highest in the MENA region and among UMICs.

The World Bank estimated remittance inflows to developing countries to reach $317bn in 2009, constituting a decrease of 6.1% from

$338bn in 2008. It expected remittances to remain almost flat in 2010, increasing by 1.4% to $322bn and rising by 3.9% to $334bn in

2011. It noted that the main risks to the outlook for remittance flows to developing countries in 2010 and 2011 are a longer than expect-

ed crisis, weak job markets in the destination countries that may lead to further tightening of immigration controls, and highly unpre-

dictable exchange rates.

Global banks see positive economic and financial implications to government formation

Merrill Lynch indicated that the formation of Lebanon's long-awaited national unity government is positive, as it correlates Lebanon's

economic performance over the last two years largely to political stability in the aftermath of Doha accord in 2008. It said the nation-

al unity government took five months to form and includes deeply divided political parties. But it noted that, while it reflects the pol-

icy challenges, unity governments have proved to be fruitful for Lebanon. It ruled out any improvement in the contentious political

issues as well as in painful fiscal reforms such as the planned increase in VAT. But it expressed optimism about the long-delayed sale

of the mobile phone licenses, which is going to be largely used for debt reduction. It noted that political stability and some progress on

reforms and privatization, along with the currently solid macroeconomic performance and strong banking sector, should pave the way

for a sovereign rating upgrade. It considered that Lebanon is getting closer to such an upgrade following the formation of the national

unity government.

In parallel, Credit Suisse said that the formation of the government means that the risks of another breakdown of talks and of renewed

political tensions have diminished considerably, adding that policy makers will get a chance to focus on economic an financial issues,

five months after the parliamentary elections. It expected Prime Minister Hariri to focus in particular on economic policy issues, at least

initially, as scope for resolving key contentious issues on the domestic political agenda is set to remain elusive. It noted that the pro-

Hariri majority has retained control over the key finance portfolio as well as over the Economy & Trade Ministry.

Further, Standard Chartered Bank noted that Lebanon's economic activity is strongly correlated to political stability. It added that the

formation of a government will strengthen sentiment and further improve the economic environment. It considered that political sta-

bility in Lebanon is crucial to GDP growth, as domestic consumption, confidence in the banking sector, investments by overseas

Lebanese, and tourism are the largest contributors to GDP. It said that the majority has kept the critical finance and economy portfo-

lio, while the opposition received the telecommunications, energy, tourism, and industry portfolios.

LEBANON THIS WEEK November 9-13, 2009

3

5. Lebanon in the News

IMF calls for implementing reforms to reduce fiscal and debt vulnerabilities, notes strength of the banking sector

The International Monetary Fund considered that the very high debt level remains a key vulnerability in Lebanon despite the recent

successes in reducing the public debt-to-GDP ratio. It indicated that Lebanon’s strong economic growth offers an opportunity to move

decisively towards fiscal reforms, and called for strict control of expenditures in order to benefit from strong revenues and reduce the

large fiscal deficit. It noted that a primary surplus of 0.9% of GDP is reachable for this year, implying an overall fiscal deficit of 10.6%

of GDP leading to a decline in the debt ratio to 151% of GDP by the end of the year.

The Fund added that continued fiscal discipline would help the government obtain the necessary financing from the market during the

remainder of 2009, given continued strong commercial bank deposit inflows and the gradual unfreezing of international capital mar-

kets. In parallel, the IMF called for the incoming government to decisively implement the Paris III reforms program to reach fiscal sus-

tainability over the medium term. It considered that the top priorities should include a reduction in the need for budgetary transfers to

Electricité du Liban and an increase in the VAT rate. It also encouraged authorities to reform the energy sector and to reconsider the

privatization of the two mobile phone providers in light of evolving market conditions.

In parallel, the IMF said that financial indicators point to the strength of the banking sector. It noted that commercial bank deposits are

growing at a rate of more than 20% year-on-year and deposit dollarization has dropped, helped by ongoing confidence and attractive

domestic interest rates. It indicated that net problem loans have declined to 2.7% at end-July 2009 from 3.1% at end-2008 and 4.7%

at end-2007, while provisions against problem loans reached 61.8% of overall problem loans at end-July, relative to 61% at end-2008

and 57% at end-2007. Further, the sector’s average return on assets was 1% as at July relative to 1.1% in 2008, while the average

return on equity was 23.9% in July compared to 14% in 2008 and 12.1% in 2007. Finally, the sector’s net liquid assets were equiva-

lent to 51.4% of short-term liabilities as at July, increasing from 50.1% at end-2008 and 47.9% at end-2007.

Total Paris III commitments reach $5.7bn at end-September

The Ministry of Finance indicated that a total of $5.7bn in Paris III-related pledges has been signed as at the end of September 2009,

equivalent to 75.6% of the $7.53bn that were pledged at the donor conference held in January 2007. It estimated that $3.77bn were

disbursed by end-September, equivalent to 66% of signed agreements and 50% of total pledges. Budget support agreements totaled

$2.13bn, equivalent to 37.5% of total signed agreements by the end of September, followed by private sector support with $1.5bn

(27%), project finance support with $1.23bn (21.6%), in-kind support with $327m (5.7%), support through the UN with $326m (5.7%),

support through civil society organizations (CSO) with $99m (1.7%) and Central Bank support with $43m (0.8%). The ministry said

disbursements increased by $600m since end-March, mainly due disbursement of $364m in private sector support, $118m in budget

support, and $102m in project finance. It said the remaining $500m in budget support are conditional on progress in implementing

reforms in the power and telecom sectors. The Finance Ministry added that 100% of Central Bank and CSO support, 97.6% of UN

support, 92.6% of budget support, 83.7% of in-kind support, and 80.8% of private-sector support have been disbursed. The United

States accounted for $1.03bn, or 18.1% of total signed grants and loan agreements. It was followed by the European Investment Bank

with $943m (16.6%), France with $599 (10.5%), Malaysia with $500m (8.8%), the World Bank Group with $475m (8.3%), the Arab

Fund for Social & Economic Development with $442m (7.8%), the Arab Monetary Fund with $375m (6.6%), the UAE with $300m

(5.3%), and the Islamic Development Bank with $250m (4.3%) as the top donors.

Association of Banks amends reference rate on US dollar and Lebanese pound lending

The Association of Banks in Lebanon (ABL) recommended to its member banks to decrease the Beirut Reference Rate in US dollars

to 5.18% from 5.2% previously. The rate, considered as the reference rate for lending in foreign currency, replaced earlier this year the

London Inter-Bank Offering Rate (LIBOR) since the ABL considered that the LIBOR no longer accurately reflects the cost of fund-

ing and lending in Lebanon. Additionally, the ABL recommended to its member banks to decrease the Beirut Reference Rate in

Lebanese pounds to 8.78% from 8.85% previously. The Beirut Reference Rate in US dollars and Lebanese pounds were adopted in

March and May 2009, respectively. The ABL indicated that the BRR does not replace the Beirut Prime Lending Rate in each curren-

cy, but constitutes the basis to calculate the prime rate after adding the cost of liquidity and refinancing, credit risks, and the profitabil-

ity of banks to the prime lending rate. The prime lending rate for US dollar and Lebanese pounds are 8.25% and 10% respectively.

Airport passengers up 24% in first 10 months of 2009

Figures released by the Hariri International Airport (HIA) show that the number of airport passengers (arrivals, departures, transit)

amounted to 4.2 million in the first 10 months of 2009, up 24% from the same period last year. The total number of flights reached

47,165 in the first 10 months of 2009, up 28.3% year-on-year. Also, the HIA processed 59,546 metric tons of cargo, of which 58,692

tons of freight and 854 tons of mail. The total cargo processed in the first 10 months of 2009 increased by 7.1% compared to the same

period of 2008.

LEBANON THIS WEEK November 9-13, 2009

4

6. Lebanon in the News

Credit and debit cards reach 1.6 million cards, ATMs total 1,181 at end of September 2009

Figures released by the Figures released by the Central Bank of Lebanon show that the number of credit and debit cards issued in

Lebanon reached 1.61 million cards at the end of September 2009, constituting a 1.3% decrease from end-June 2009, a 2.7% rise in

the first 9 months of the year and a 4.2% rise on a yearly basis. Resident cardholders accounted for 97.2% of total cards issued in

Lebanon. The distribution of payment cards by type shows that debit cards with residents accounted for 63% of the total, followed by

credit cards with residents (22.4%), charge cards with residents (9.8%), non-resident debit cards (2.2%), resident prepaid cards (2%),

non-resident charge cards (0.4%), and non-resident credit cards (0.2%). The number of ATMs rose by 1.6% to 1,181 machines on a

quarterly basis, by 3.6% in the first 9 months of the year and by 5.9% from 1,115 ATMs at the end of September 2008. The Greater

Beirut area had 584 ATMs, accounting for 49.4% of the total, followed by Mount Lebanon with 262 (22.2%), the North with 128

(10.8%), the South with 98 (8.3%), the Bekaa with 88 (7.5%), and Nabatiyeh with 21 (1.8%). Further, the aggregate number of point

of sales accepting payment cards reached 45,145 by the end of September, increasing by 1.3% since the end of 2008 and decreasing

by 1% annually.

The average monthly domestic payment by residents totaled $102.8m in the third quarter of 2009, rising by 20.6% quarter-to-quarter

and by 24.1% from the third quarter of 2008, while the average monthly payment abroad by residents increased by 17.7% to $62.2m

on a quarterly basis and by 11.3% from the end of September 2008. In parallel, domestic payments by residents rose by 20.9%, while

payments abroad by residents increased by 7.4% in the first 9 months of 2009 compared to the same period last year.

Further, the average monthly value of cash withdrawals by residents using ATMs increased quarterly by 10.6% to $415.9m and rose

annually by 19.5%, while average monthly withdrawals by non-residents grew by 45.2% to $7.8m quarter-to-quarter and by 19% year-

on-year. Also, the average monthly purchases in Lebanon by non-residents rose 19.2% quarter-to-quarter and by 10.2% annually to

$2.1m. Domestic card payments in Lebanese pounds accounted for 12.6% of aggregate payments in all currencies, while local curren-

cy withdrawals represented 66.1% of the total.

Number and Usage of Payment Cards Issued in Lebanon

(for the quarters ending September 2009 and September 2008)

Sep-09 Sep-08 Change

Cards

With residents 1,560,991 1,492,888 4.6%

With non-residents 44,970 48,335 -7.0%

Total 1,605,961 1,541,223 4.2%

ATMs 1,181 1,115 5.9%

Points of Sales 45,145 45,596 -1.0%

Purchases (in US$m)

by residents in Lebanon 308.4 248.4 24.2%

% in Lebanese pounds 12.6 11.6

by non-residents in Lebanon 6.2 5.6 10.7%

by residents outside Lebanon 186.7 167.7 11.3%

Cash withdrawal (in US$m)

by residents in Lebanon 1,247.6 1,044.1 19.5%

% in Lebanese pounds 66.1 67.8

by non-residents in Lebanon 23.5 19.8 18.7%

Source: Central Bank of Lebanon, Byblos Research

LEBANON THIS WEEK November 9-13, 2009

5

7. Corporate Highlights

RYMCO's profits down 70% to $2.4m in first 9 months of 2009

Automobile dealer Rasamny Younis Motor Co. sal (RYMCO) declared net profits of $2.41m in the first 9 months of 2009, down 70.5%

from $8.17m in the same period last year. Sales revenues (net of discounts) totaled $142.9m, posting a 4% increase year-on-year; while

net earnings from servicing and repairs, or 'garage income', increased by 41.8% to $3.2m. The firm's cost of goods sold rose by 7.4%

to $128.8m. Also, general and administrative expenses increased by 28.1% to $3.3m, while advertising & selling expenses decreased

by 17.6% to $1.1m, and overall operating charges rose by 15.4% to $9.5m.

RYMCO's total assets and total equity amounted to $138.3m and $54.1m at the end of September 2009 respectively, compared to

$120.6m and $49.7m a year earlier. RYMCO's inventory of cars and spare parts increased 47.3% to $55.6m. RYMCO is the only car

retailer listed on the Beirut bourse. It had a 23% market share in new cars registered in 2008, the highest among car dealerships in the

country.

FNB acquires consumer finance company

First National Bank sal (FNB) acquired a majority stake in Capital Finance Company sal (CFC), a consumer finance firm. CFC was

established at the end of 1999 with a paid-in capital of LBP 10m and started operations in 2000. It extends credit facilities at retail out-

lets to customers buying cars, computers, and home appliances. FNB acquired the stake from Business Projects Company after the lat-

ter’s plan to swap its stake in CFC for a stake in the bank was declined by the Central Bank. CFC has assets of $80.4m, loans of $70.4m

and capital of $23.5m.

Tripoli Port to be developed by Chinese contracting company

The Ministry of Transportation & Public Work approved the Chinese contracting company ‘Chinese Harbor Engineering Company’ to

pursue the second phase of the project aiming at enlarging the Tripoli Port. The development of the Tripoli Port is projected to be com-

pleted over an 18-month period and to cost $48m.

Casino du Liban elects new board of directors

The Ordinary General Assembly of Companie du Casino du Liban sal (CCL) elected a new Board of Directors for a three-year term

and voted in Mr. Hamid Kreidi as chairman to replace the outgoing Dr. Khater Bou Habib. Intra Investment Company sal, the govern-

ment-controlled investment firm, owns 51% of CCL. The General Assembly also approved the distribution of $25 per share in divi-

dends for 2008. CCL posted net profits of $16.2m in the first 9 months of 2009, up 89.3% from the same period last year. Its net prof-

its totaled $27.2m in 2008.

LEBANON THIS WEEK November 9-13, 2009

6

8. Ratio Highlights

(in % unless specified) 2006 2007 2008 Change*

Nominal GDP(1) ($bn) 22.7 24.6 28.8

External Debt / GDP 89.9 86.4 73.4 (1,300)

Local Debt / GDP 88.1 84.6 89.8 520

Total Debt / GDP 178.4 171.0 163.2 (780)

Trade Balance / GDP (31.3) (36.6) (43.9) (730)

Exports / Imports 24.3 23.8 21.6 (220)

Budget Revenues / GDP 19.4 23.6 24.4 80

Budget Expenditures / GDP 30.8 33.9 34.5 60

Budget Balance / GDP (11.5) (10.3) (10.1) 20

Primary Balance / GDP 0.4 2.9 2.1 (80)

BdL FX Reserves / M2 65.6 59.6 68.9 930

M3 / GDP 234.4 243.2 238.4 (480)

Bank Assets / GDP 327.2 334.4 327.3 (710)

Bank Deposits / GDP 267.4 273.5 270.1 (340)

Private Sector Loans / GDP 67.4 72.2 86.9 1,470

Dollarization of Deposits 76.2 77.3 69.6 (770)

Dollarization of Loans 84.0 84.3 86.6 230

* Change in basis points 07/08

(1) Based on Ministry of Finance Estimations and the International Monetary Fund

Source: Association of Banks in Lebanon, Byblos Research Calculations

Note: M2 includes money in circulation and deposits in LBP, M3 includes M2 plus Deposits in FC and bonds

Risk Outlook

Lebanon July 2008 July 2009 Aug 2009 Change* Risk Level

Political Risk Rating 57.0 57.5 57.5 High

Financial Risk Rating 31.5 28.0 27.5 High

Economic Risk Rating 28.5 30.0 27.5 High

Composite Risk Rating 58.5 57.7 56.2 High

Regional Average July 2008 July 2009 Aug 2009 Change* Risk Level

Political Risk Rating 65.6 65.1 65.1 Moderate

Financial Risk Rating 41.2 41.6 41.7 Very Low

Economic Risk Rating 39.8 34.4 34.3 Moderate

Composite Risk Rating 73.3 70.5 70.5 Low

*year-on-year

Source: The PRS Group, Byblos Research

Note: Political & Composite Risk Ratings range from 0 to 100 (where 100 indicates the lowest risk)

Financial & Economic Risk ratings range from 0 to 50 (where 50 indicates the lowest risk)

Ratings & Outlook

Sovereign Ratings Foreign Currency Local Currency

LT ST Outlook LT ST Outlook

Moody's B2 NP Stable

Fitch B- B Stable B-

S&P B- C Stable B- C Stable

Capital Intelligence B B Stable B B Stable

Source: Rating agencies

Banking Ratings Banks' Financial Strength Banking Sector Risk Outlook

Moody's D- Stable

EIU B Stable

Source: Rating agencies

LEBANON THIS WEEK November 9-13, 2009

7

9. Economic Research & Analysis Department

Byblos Bank Group

P.O. Box 11-5605

Beirut – Lebanon

Tel: (961) 1 338 100

Fax: (961) 1 217 774

E-mail: research@byblosbank.com.lb

www.byblosbank.com.lb

Lebanon This Week is a research document that is owned and published by Byblos Bank sal. The contents of this publication, includ-

ing all intellectual property, trademarks, logos, design and text, are the exclusive property of Byblos Bank sal, and are protected pur-

suant to copyright and trademark laws. No material from Lebanon This Week may be modified, copied, reproduced, repackaged, repub-

lished, circulated, transmitted, redistributed or resold directly or indirectly, in whole or in any part, without the prior written authoriza-

tion of Byblos Bank sal.

The information and opinions contained in this document have been compiled from or arrived at in good faith from sources deemed

reliable. Neither Byblos Bank sal, nor any of its subsidiaries or affiliates or parent company will make any representation or warranty

to the accuracy or completeness of the information contained herein.

Neither the information nor any opinion expressed in this publication constitutes an offer or a recommendation to buy or sell any assets

or securities, or to provide investment advice. This research report is prepared for general circulation and is circulated for general infor-

mation only. Byblos Bank sal accepts no liability of any kind for any loss resulting from the use of this publication or any materials

contained herein.

The consequences of any action taken on the basis of information contained herein are solely the responsibility of the person or organ-

ization that may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities

or investment strategies that may be discussed in this report and should understand that statements regarding future prospects may not

be realized.

LEBANON THIS WEEK November 9-13, 2009

8

10. BYBLOS BANK GROUP

LEBANON BELGIUM

Byblos Bank S.A.L Byblos Bank Europe S.A

Achrafieh - Beirut Bussels Head Office

Elias Sarkis Avenue - Byblos Bank Tower 10, Rue Montoyer

P.O.Box: 11-5605 B-1000 Brussels - Belgium

Riad El Solh - Beirut 1107 2811 - Lebanon Phone: (+32) 2 551 00 20

Phone: (+961) 1 335200 Fax: (+32) 2 513 05 26

Fax: (+961) 1 339436 E-mail: byblos.europe@byblosbankeur.com

SYRIA ENGLAND

Byblos Bank Syria S.A London Branch

Abu Roummaneh Head Office Berkeley Square House - Suite 5

Al Chaalan - Amine Loutfi Hafez Str. Berkeley Sq.

P.O.Box: 5424 Damascus - Syria GB - London W1J 6BS - United Kingdom

Phone: (+ 963) 11 9292 - 3348240 / 1 / 2 / 3 / 4 Phone: (+44) 207 493 35 37

Fax: (+ 963) 11 3348207 Fax: (+44) 207 493 12 33

E-mail: byblosbanksyria@byblosbank.com E-mail: byblos.europe@byblosbankeur.com

SUDAN FRANCE

Byblos Bank Africa Ltd. Paris Branch

Khartoum - Sudan 15 Rue Lord Byron

El Amarat -Street 21 F- 75008 Paris - France

P.O.Box: 8121 El Amarat - Khartoum - Sudan Phone: (+33) 1 45 63 10 01

Phone: (+249) 183 566 444 Fax: (+33) 1 45 61 15 77

Fax: (+249) 183 566 454 E-mail: byblos.europe@byblosbankeur.com

E-mail: byblosbankafrica@byblosbank.com

IRAQ CYPRUS

Erbil Branch, Kurdistan, Iraq Limassol Branch

Street 60, 1, Arch. Kyprianou / St. Andrew Street

Near Sports Stadium P.O.Box 50218

P.O.Box: 34 - 0383 Erbil - Iraq 3602 Limassol - Cyprus

Phone: (+ 964) 66 2233457 / 9 Phone: (+357) 25 341433 / 4 / 5

Fax: (+ 964) 66 2233458 Fax: (+357) 25 367139

E-mail: iraqbranch@byblosbank.com.lb E-mail: bybloscyprus@byblosbank.com

ARMENIA UNITED ARAB EMIRATES

Byblos Bank Armenia CJSC Byblos Bank Abu Dhabi Representative Office

18/3 Amiryan Street Intersection of Muroor and Electra Streets

Yerevan, 37500 - Republic of Armenia P.O.Box: 73893 Abu Dhabi - UAE

Phone: (+374) 10 530 362 Phone: (+ 971) 2 6336400

Fax: (+374) 10 535 296 Fax: (+971) 2 6338400

E-mail: byblosbankuae@byblosbank.com

NIGERIA

Byblos Bank Nigeria Representative Office

10-14 Bourdillon Road

Ikoyi, Lagos - Nigeria

Phone: (+ 234) 1 6653633

(+ 234) 1 8990799

E-mail: melamm@byblosbank.com.lb

LEBANON THIS WEEK November 9-13, 2009

9