SEB:s Boprisindikator juni 2010

•

0 likes•2,618 views

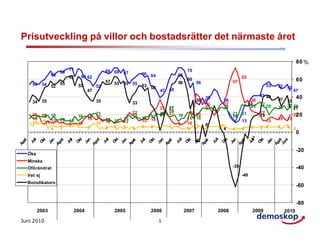

Färre hushåll tror på stigande bostadspriser och fler än tidigare tror på fallande priser det kommande året. Det visar SEB:s Boprisindikator för juni. Hushållen tror att reporäntan ligger på en procent om ett år och andelen som planerar att binda räntan är oförändrad sedan förra månaden.

More Related Content

Viewers also liked

Viewers also liked (14)

More from SEBgroup

More from SEBgroup (20)

SEB:s Boprisindikator juni 2010

- 1. Prisutveckling på villor och bostadsrätter det närmaste året 80 % 71 69 68 70 68 67 66 64 65 62 63 62 65 62 57 55 56 60 56 57 60 54 54 52 55 53 52 55 55 53 50 53 52 50 47 47 48 47 39 41 40 40 35 35 36 36 36 37 35 34 33 32 33 27 27 31 27 28 29 32 29 31 28 30 29 27 22 24 22 20 19 19 21 19 21 21 19 20 20 21 21 19 20 20 18 18 18 18 15 14 13 13 13 15 17 14 15 16 17 13 14 16 16 15 15 11 12 13 12 13 13 9 11 9 10 7 9 10 9 10 8 4 5 5 5 6 6 4 6 6 5 7 7 4 7 4 7 4 4 4 5 5 6 6 6 4 0 -7 li li t t t n n n t t li li li n n n t t li li ni ril n ril Ju l ril Ok Ok Ok Ok Ok Ok Ok ril ril ril ril ri Ju Ju Ju Ju Ju Ju Ju Ja Ja Ja Ja Ja Ja Ja Ap Ap Ap Ap Ap Ap Ap Ap -20 Öka Minska Oförändrat -39 -40 Vet ej -49 Boindikatorn -60 -80 2003 2004 2005 2006 2007 2008 2009 2010 Juni 2010 1

- 2. Prisutveckling på villor och bostadsrätter det närmaste året 80 % 73 72 72 73 71 73 73 73 73 69 71 69 68 68 70 69 68 67 68 70 65 64 62 64 63 62 63 63 65 66 63 62 66 64 66 62 62 66 65 6563 66 62 60 58 58 58 59 57 60 59 58 57 57 58 60 59 60 56 60 60 56 57 57 60 54 55 54 52 54 55 53 52 5 55 55 55 53 54 4 53 52 50 52 54 55 53 54 54 53 52 50 51 49 50 49 49 47 47 45 47 47 48 47 46 42 43 41 43 41 41 42 43 44 42 42 44 42 41 41 41 40 41 40 41 40 40 39 40 38 39 38 35 37 35 37 36 37 36 36 37 35 36 34 33 32 33 31 33 33 31 3234 31 32 30 32 30 32 31 29 30 29 31 30 30 27 29 27 27 26 27 28 25 27 27 28 27 27 28 29 25 27 2927 22 25 24 22 24 22 26 25 22 20 22 20 24 22 26 25 23 22 22 24 26 20 19 17 19 18 21 21 21 21 21 21 19 21 21 21 21 20 19 18 19 18 18 17 16 18 17 20 18 19 16 17 19 17 15 15 17 14 13 15 13 13 15 16 14 14 15 13 13 15 13 15 7 16 13 17 16 15 15 1 20 18 15 13 16 16 19 18 18 16 18 19 20 19 17 20 20 16 16 15 15 1413 14 11 12 14 13 14 13 12 14 14 14 13 13 13 3 1 14 13 11 11 11 11 10 9 9 9 10 10 10 10 12 12 10 11 11 11 12 12 10 10 12 11 7 9 9 7 7 5 7 6 7 7 6 9 9 5 5 5 5 8 5 6 6 5 6 5 6 6 6 66 5 7 5 5 7 7 6 9 5 8 5 7 7 8 8 66 7 8 5 6 7 6 7 8 4 4 4 3 4 4 4 2 4 44 4 4 44 4 4 3 3 44 6 5 5 6 5 6 5 5 6 6 4 6 4 -1 -2 0 -5 -7 ar b Aarsb ar b MFeb Aarsb Aarsb Aarsb De v De v De v De v De v Seugi Seugi De v Ju aj Not JMalj Not Ju alj Not Not JMalj Not Ju aj Seug Seug Seug De v MFen MFen MFen Not A ulii A ulii n n n JMaj Ju aj Not JMaj Seugi Auli Seugi Ji Ji Auli ni n A ul A uil Okt Okt Okt Ji Ok Ok Ok Ok pt pt pt pt Jac Jac Jac Jac Jac Jac Aul -11 -11 Mil il Aps Mil Aps ril Mil Jn un Jn un un Mri i c Aars MFe MFe ri un Jn MFe p p p pr Ja r pr pr pr p Ap J -15 -23 -20 Öka Minska -39 -40 Oförändrat -49 Vet ej -52 Boindikatorn -62 -60 -80 2003 2004 2005 2006 2007 2008 2009 2010 Juni 2010 2

- 3. Typ av lån på sin bostad Fast ränta 50 % Rörlig ränta Kombination av fast och rörlig Har inga lån 40 38 Vet ej 37 36 36 35 34 33 33 33 33 33 32 32 32 32 32 31 31 31 31 31 31 29 30 30 30 30 30 30 29 29 29 29 29 29 29 29 29 29 28 28 28 28 28 28 28 28 28 27 27 27 27 27 27 27 27 27 27 27 26 26 26 26 25 25 25 25 25 25 25 25 25 24 24 24 24 24 23 23 22 22 22 22 22 23 21 21 21 21 21 19 20 20 20 19 20 20 18 18 18 17 17 17 17 16 16 16 16 16 16 16 15 15 15 15 15 14 14 14 14 14 13 13 12 12 12 11 11 10 10 6 6 5 5 5 5 5 5 4 4 4 4 4 4 4 4 4 4 4 4 3 3 3 2 2 2 2 2 2 2 0 kt t t t t t t li li n n li li li li n n n n li ni n ril ril ril ril ril ril ril Ok Ok Ok Ok Ok Ok ril Ju Ju Ju Ju Ju Ju Ju Ja Ja Ja Ja Ja Ja Ja O Ju Ap Ap Ap Ap Ap Ap Ap Ap 2003 2004 2005 2006 2007 2008 2009 2010 Juni 2010 3

- 4. Typ av lån på sin bostad Fast ränta 50 % Rörlig ränta Kombination av fast och rörlig Har inga lån 40 38 Vet ej 37 37 37 36 36 36 36 35 35 3535 35 35 34 34 34 34 33 32 33 32 32 33 33 33 33 32 33 32 32 32 32 32 33 32 33 32 32 3233 32 31 31 31 3131 31 31 31 31 31 31 31 31 31 31 31 31 31 31 31 29 29 30 30 30 30 30 30 30 30 30 30 30 30 30 30 30 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 29 28 28 28 28 28 28 28 28 28 28 28 28 28 28 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 27 26 26 26 26 26 26 26 26 26 26 26 26 2626 25 25 25 25 24 24 24 25 25 25 24 24 25 25 25 24 25 24 24 25 24 24 24 24 24 24 25 24 23 23 23 23 23 23 23 23 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 22 21 21 21 21 21 21 2121 2121 21 2121 21 20 19 19 20 20 20 20 19 1919 19 20 19 19 19 19 20 20 18 18 18 18 18 18 17 17 17 17 17 17 17 17 17 17 17 17 16 16 16 16 16 16 1616 16 16 16 16 16 16 16 16 16 16 15 14 14 15 14 15 15 15 15 14 14 14 15 15 14 15 15 14 14 15 14 15 14 15 15 14 14 15 1415 14 13 13 13 13 13 13 13 13 13 13 13 12 12 12 12 12 11 11 11 10 10 6 66 6 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 44 4 44 4 4 44 44 4 44 4444 4 4 4 4 4 44 4 33 3 3 33 3 3 3 3 33 3 3 33 33 33 33 3 2 2 2 2 2 222 2 22 2 2 2 2 2 22 0 Apsb Apsb Aarsb Apsb Apsb Apsb Apsb Seug De v De v De v De v De v De v De v Seugi No t Aulii No t No t Aulii Aulii Aulii Aulii Aulii Seug Se g Se g Se g Seug Juaj Juaj Juaj Juaj Juaj Juaj JMalj J i i Maen Maen Ma en Ma en MFen Ma en Ma en JMalj Not Not Not Not Mril Mril Mril Opt Jac Jac Jac Jac Jac Mril Mril Mril Opt Opt Aul Jn n n n Jn Jac Jac un Jn un k k k pt pt pt Ot ri k Ok Ok Ok ri Ju Ju Ju p r r r r r r Ap p F F F F F F 2006 2007 2008 2009 2010 2003 2004 2005 Juni 2010 4

- 5. Andel av de som har rörlig ränta som tror de kommer att binda räntorna inom tre månader 50 % Tror sig binda räntorna inom tre månader 40 30 19 20 17 16 13 12 12 12 12 12 11 11 10 10 10 10 10 9 8 8 8 7 7 7 7 6 6 6 6 6 5 5 5 4 4 4 0 kt kt ni n n n n n n n t t t t t li li li li li li li ril ril ril ril ril ril ril Ju l Ok Ok Ok Ok Ok ri Ju Ju Ju Ju Ju Ju Ju Ja Ja Ja Ja Ja Ja Ja O O Ap Ap Ap Ap Ap Ap Ap Ap 2003 2004 2005 2006 2007 2008 2009 2010 Juni 2010 5

- 6. Ap Mril Juaj Jn Aulii 17 Juni 2010 Seug 99 Okpt Not 16 2003 De v 11 Jac 1 10 0 MFen Aarsb pr 6 6 i 7 7 JMalj un 9 J Aulii 12 Seug 11 Opt 13 k 2004 No t 6 De v Jac F 10 10 7 7 Ma en r 8 Apsb Mril 12 Juaj 5 Ju n 7 Aulii 6 6 Se g 9 Opt k 2005 13 No t De v 10 Jac 9 Fn Ma e r 11 11 Apsb månader 17 Mril Juaj 19 10 Ju n 8 Aulii Se g 5 Okpt 6 6 6 Not 2006 De v 10 6 Jac 11 MFen Aarsb 88 pr i 7 12 JMalj un J Aulii Seug 10 10 Opt 66 6 6 Notk 8 De v 2007 Tror sig binda räntorna inom tre Jac 10 F 55 Ma en r 6 Apsb Mril Juaj Jn Aulii Seug 44 4 44 4 Opt 8 k No t De v 2008 Jac 6 Fn 55 5 Ma e binda räntorna inom tre månader r 3 Apsb 7 Mril Juaj Jn Auli 12 9 9 Seugi pt 11 11 Ok 4 Not 8 De v 2009 Jac 55 F 7 Ma en r 6 Apsb 5 Mril 7 Juaj ni 12 Andel av de som har rörlig ränta som tror de kommer att 11 2010 11 0 10 10 20 30 40 50 %