Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

3

Boston Consulting Grouppartners with leaders in business and society

to tackle their most important challenges and capture their greatest

opportunities. BCG was the pioneer in business strategy when it was

founded in 1963. Today, we work closely with clients to embrace a

transformational approach aimed at benefiting all stakeholders—

empowering organizations to grow, build sustainable competitive

advantage, and drive positive societal impact.

Our diverse, global teams bring deep industry and functional expertise

and a range of perspectives that question the status quo and spark change.

BCG delivers solutions through leading–edge management consulting,

technology and design, and corporate and digital ventures. We work in a

uniquely collaborative model across the firm and throughout all levels of

the client organization, fueled by the goal of helping our clients thrive and

enabling them to make the world a better place.

ABOUT BCG

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

5

Once focused primarilyon transactional efficiency, GCCs have now evolved into strategic powerhouses, cementing

their role as key enablers of enterprise transformation. However, only 8% of GCCs qualify as top performers,

demonstrating maturity across three key strategic levers: market advantage, innovation, and enterprise efficiency

(incl. cost advantage).

These top performers distinguish themselves through three fundamental pillars:

GCC maturity: Multi-dimensional evaluation framework

Enterprises are looking to their GCCs to evolve from being delivery engines to becoming strategic value creators.

This means co-owning global business outcomes, influencing enterprise strategy, and enabling transformation—not

just supporting it.

High-performing GCCs stand out through nine key enablers, including embedded leadership, dedicated innovation

budgets, AI integration, and strong governance—marking a clear shift from traditional models.

Value creation is now central to GCC maturity. Leading centers take full ownership, influence decisions, and deliver

tangible impact. technology firms lead in AI and product innovation, while Consumer products and goods players

excel with innovation-driven models.

By advancing next-gen capabilities, GCCs are redefining their role—from execution arms to engines of

enterprise innovation.

Beyond cost and scale: Rethinking the GCC mandate

01

Scaling AI-driven automation and

adopting mature microservices

architectures and modular

algorithm to enhance efficiency

and innovation

AI, Techology

and Data

Expanding and establishing CoEs

with an AI/ML focus, increasing

end-to-end product ownership, and

strengthening business continuity

and resilience

Delivery

Excellence

Embedding global roles in hubs,

activating localized EVP models,

and ensuring clear outcome-

based KPIs

People and

Organizational

Effectiveness

02

Top three enablers with highest difference between top performers and others, across these pillars, are modular

algorithms, leadership and autonomy, and microservices/API.

Executive

Summary (I)

6.

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

6

Leveraging AI hasbecome a defining factor separating mature GCCs from the rest. While many organizations are

still exploring early-stage applications, top-performers have already embedded AI into its operating model, with

GenAI use cases progressing well beyond pilots and into scaled deployment. This shift is delivering measurable

impact, including 5–10%+ baseline cost savings, up to 30% productivity gains, and reallocation of 30–40% of the

workforce from repetitive to higher-value tasks.

AI is no longer optional—it is foundational to GCC maturity. Delayed adoption risks widening performance gaps and

missed value in a rapidly evolving landscape.

However, it is important to note that GenAI adoption is not a straight line to success. It is, in fact, a phased approach

involving identifying and validating use cases, scaling them and then ultimately refining and optimizing these

applications – this is when the transformation is truly complete.

Top-performing GCCs are institutionalizing GenAI through AI CoEs, modular architectures, and cross-functional

teams—embedding it as a core enterprise capability, not an isolated initiative.

Closing the maturity gap requires more than just intent—it demands a clear plan of action. For GCCs aiming to

maximize impact, the focus must shift to activating the nine key enablers that drive real change.

People and organizational effectiveness must be enabled through clear decision rights, embedded global roles,

outcome-driven KPIs, and localized, fully activated EVP models.

Delivery excellence hinges on building resilient operations, scaling AI/ML-focused CoEs, and expanding end-to-end

process ownership with stronger C-suite alignment.

AI and technology transformation are non-negotiable. Leading GCCs are deploying AI at scale, building flexible

microservices platforms, and implementing modular, interoperable architectures to support agility and innovation.

Together, these enablers define a structured path from operational maturity to strategic leadership.

The acceleration playbook: Closing the maturity gap

04

Executive

Summary (II)

03 AI: The differentiator and accelerator

8

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

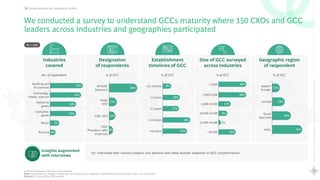

Survey approach andrespondents' profile

We conducted a survey to understand GCCs maturity where 150 CXOs and GCC

leaders across industries and geographies participated

Insights augmented

with interviews

No. of respondents % of GCC % of GCC % of GCC % of GCC

62%

VP/SVP/

Directors1

Head,

GCC

CXO, GCC

CEO/

President/ MD/

Chairman

17%

<12 months

1-3 years

3-5 years

5-10 years

>10 years

9%

18%

17%

27%

11%

18%

28%

43%

Eastern

Europe

LATAM

South

East Asia

India

Designation

of respondents

Establishment

timelines of GCC

Size of GCC surveyed

across industries

Industries

covered

Geographic region

of respondent

N = 150

<1,000

1,000-5,000

5,000-10,000

10,000-15,000

15,000-20,000

>20,000

29%

19%

13%

29%

29%

9%

3%

11%

8%

Banking and

Fin services

Consumer

goods

Retail

Pharma

25%

24%

20%

7%

4%

20%

Industrial

goods

Technology,

media, telecom

1. VP: Vice President; SVP: Senior Vice President

Note: Survey question: Industry in which you are operating; your designation; establishment timeline of your GCC, size of your GCC

Source: GCC Survey 2024, BCG Analysis

25+ interviews with industry experts and advisors with deep domain expertise in GCC transformation

9.

9

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

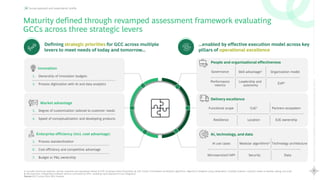

Survey approach andrespondents' profile

Defining strategic priorities for GCC across multiple

levers to meet needs of today and tomorrow...

...enabled by effective execution model across key

pillars of operational excellence

Enterprise efficiency (incl. cost advantage)

5. Process standardization

6. Cost efficiency and competitive advantage

7. Budget or P&L ownership

People and organizational effectiveness

Delivery excellence

AI, technology, and data

Functional scope CoE3 Partners ecosystem

Resilience Location E2E ownership

AI use cases Modular algorithms4 Technology architecture

Microservices5/API Security Data

Maturity defined through revamped assessment framework evaluating

GCCs across three strategic levers

Governance Skill advantage1 Organization model

Performance

metrics

Leadership and

autonomy

EVP2

1. Includes functional expertise, domain expertise and specialized skillset 2. EVP: Employee Value Proposition 3. CoE: Center of Excellence 4. Modular algorithms: Algorithms designed using independent, reusable modules, making it easier to develop, debug, and scale

5. Microservices: Independent software services connected by APIs—enabling rapid deployment and integration

Source: GCC Survey 2024, BCG Analysis

Market advantage

3. Degree of customization tailored to customer needs

4. Speed of conceptualization and developing products

Innovation

1. Ownership of innovation budgets

2. Process digitization with AI and data analytics

11

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

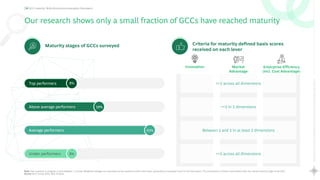

GCC maturity: Multi-dimensionalevaluation framework

Our research shows only a small fraction of GCCs have reached maturity

Top performers

Above average performers

Average performers

Under performers

Criteria for maturity defined basis scores

received on each lever

>=3 across all dimensions

>=3 in 2 dimensions

Between 2 and 3 in at least 2 dimensions

<=2 across all dimensions

Enterprise Efficiency

(incl. Cost Advantage)

Market

Advantage

Innovation

65%

8%

19%

8%

Note: Each question is assigned a score between 1–4 scale. Weighted averages are calculated across questions within each lever, generating a composite score for all three levers. The combination of these scores determines the overall maturity stage of the GCC.

Source: GCC Survey 2024, BCG Analysis

Maturity stages of GCCs surveyed

12.

12

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

Top performers Above average performers Average performers Under performer

Technology, media, telecom leads

in overall maturity with ~35% of

hubs performing above average

or top performers and lowest

share of underperformers at 3%

Consumer goods and Banking and

financial services are anchored in

the middle—with ~70% average

performing GCCs; indicating a

need to accelerate their maturity

Industrial goods has the highest

share of above-average performers

(27%)—but only 3% reach top-tier,

highlighting opportunity for targeted

improvement

GCC maturity varies sharply across 6 key industries

Source: GCC Survey 2024, BCG Analysis

Consumer

goods

Retail

Pharma

Technology,

media, telecom

3%

27%

18% 55%

17%

17% 66%

8% 25% 3%

5% 22% 68% 5%

64%

3%

13% 7% 77%

13%

27% 57%

Industrial

goods

Banking and

Fin services

Maturity of GCCs across industries

z

13.

13

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

Maturity of GCCs across top 9 countries (by number of hubs)

1.The other countries in the survey include UK, Brazil, Indonesia, France, Germany, Spain, Thailand, China, Puerto Rico, Vietnam etc.

Note: Total responses for each country – India (77), Malaysia (15), Mexico (18), Philippines (12), Poland (11), Singapore (26), U.S. (52), Others (195)

Source: GCC Survey 2024, BCG Analysis

India strikes a rare balance—

~30% of GCCs are mature

performers, while

underperformance is limited

to just 6%

Despite 0% underperformance in

Poland, only 9% of GCCs are above

average—suggesting a stagnant

mid-tier with minimal progression

into higher maturity

U.S. has the highest share of top

and above average performers

(~35%) but 10% underperformers,

indicating polarized maturity

India,Mexico,and U.S.lead in GCC maturity—India ahead on scale with consistency

India

Malaysia

Mexico

Philippines

Poland

Singapore

Others1

4%

4% 23% 69%

6%

8% 20% 66%

9%

19% 62%

27% 60% 13%

8% 84% 8%

U.S. 10%

11% 25% 54%

17% 72%

11%

10%

Top performers Above average performers Average performers Under performer

9% 91%

14.

14

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

Note: Overall scores assigned by allocating weightages to different responses from 1 to 4

Source: GCC Survey 2024, BCG Analysis

Responses evaluated on a four-point scale for each strategic lever

>=3

2 to 3

<2

Scores

Lowest (1)

Highest (4)

Enterprise Efficiency

(incl. Cost Advantage)

(Process standardization, P&L

ownership and competitive advantage)

>50% processes

standardized with budget

or P&L ownership and

cost efficiencies

20-50% of processes

standardized with limited

budget or P&L ownership

expected cost arbitrage

0-20% of the processes

standardized with no

budget or P&L ownership

and low-cost savings

41%

50%

Innovation

(Innovation budget,

digitization with AI)

Powered by AI co-pilots,

automation focus with

enterprise workflow

tools, RPA

Automated sub process,

with multiple

manual processes

Manual process,

minimal automation

19%

60%

21%

Market Advantage

(Degree of customization and

localization tailored to specific

market need)

Full to high level of design

customized to local and

market needs

Limited customization

and low agility

No customization

58%

37%

5% 9%

Low High

Lever definition

% respondents

Strategic levers

xx

15.

15

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

Industry Exemplar:

Global consumer company

Achieved best-in-class process

standardization by empowering

GPOs1, eliminating non-value

steps, optimizing global models,

and automating workflows—

delivering 25%+ productivity gains,

faster PR-to-PO cycles, and 99%+

payroll accuracy

Average score of industries in the three strategic pillars

2.5

2.3

2.4

2.3

2.2

1.9

2.3

Innovation

2.7

Market

Advantage

2.8

2.7

2.7

2.7

2.7

3.0

2.7

2.4

2.7

2.6

2.2

2.0

2.6

Enterprise Efficiency

(incl. Cost Advantage)

Industrial

goods

Retail

Pharma

Technology,

media, telecom

Consumer

goods

Banking and

Fin services

Strategic levers

Overall

Average score

Above average score Below average score

1. Global Process Owners

Source: GCC Survey 2024, BCG Analysis, Expert Interviews

Industry Exemplar:

Leading pharma company

R&D hubs established across

multiple locations, focused on

developing personalized healthcare

solutions tailored to local market

needs—such as cancer treatments

adapted to regional genetic profiles

Majority industries showcase average performance across the three maturity

levers, except for technology, media, telecom which outperforms in all

16.

16

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

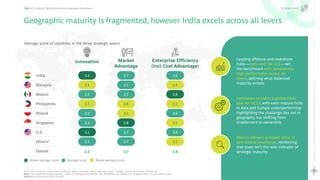

Geographic maturity is fragmented, however India excels across all levers

1.The other countries in the survey include UK, Brazil, Indonesia, France, Germany, Spain, Thailand, China, Puerto Rico, Vietnam etc.

Note: Total responses for each country – India (77), Malaysia (15), Mexico (18), Philippines (12), Poland (11), Singapore (26), U.S. (52), Others (195)

Source: GCC Survey 2024, BCG Analysis

Average score of countries in the three strategic levers

Mexico delivers outsized value in

operational excellence, reinforcing

that scale isn’t the sole indicator of

strategic maturity

Innovation remains a global weak

spot for GCCs, with even mature hubs

in Asia and Europe underperforming-

highlighting the challenge lies not in

geography, but shifting from

enablement to ownership

Leading offshore and nearshore

hubs—India and the U.S.—set

the benchmark with consistently

high performance across all

levers, defining what balanced

maturity entails

India

Malaysia

Mexico

Philippines

Poland

Singapore

U.S.

Overall

Enterprise Efficiency

(incl. Cost Advantage)

2.6

2.6

2.4

2.8

2.5

2.6

2.5

2.6

2.5

Innovation

2.4

2.1

2.3

2.1

2.3

2.3

2.5

2.3

2.3

Market

Advantage

2.7

2.7

2.7

2.7

2.6

2.5

2.8

2.7

2.7

Others1

Strategic levers

Average score

Above average score Below average score

17.

17

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

What a strategic value creating GCC looks like

Strategic levers

Enterprise Efficiency

(incl. Cost Advantage)

Smart Scaling: Growing through

strategic P&L ownership

Top performers unlock scale through

standardization—all exceed 50% process

standardization, vs none among underperformers

90%+ top performers unlock superior cost

advantage vs industry benchmark

~60% top performers retain P&L ownership

across large products and services

portfolios (>70%)

Innovation

Driving Innovation: Technology

as a Core Enabler

80%+ top performers embed AI, automation and

other advanced technologies in E2E processes to

drive efficiency and business outcome

40%+ top performers own dedicated budgets for

driving enterprise innovation

Top performers drive outsized patent impact—

80%+ file more than a quarter of all patents

Market Advantage

Market Mastery: Leading with

ownership and expertise

100% of top performers are winning in markets by

customizing products and services to local market

needs

Top performers play a pivotal role in value

creation with 80%+ owning strategic

processes and high value work and

knowledge—based work

Source: GCC Survey 2024, BCG Analysis

18.

18

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

1. EVP: Employee Value Proposition 2. Includes functional expertise, domain expertise and specialized skillset 3. CoE: Center of Excellence 4. Modular algorithms: Algorithms designed using independent, reusable modules, making it easier to develop, debug, and scale

5. Microservices: Independent software services connected by APIs—enabling rapid deployment and integration

Source: GCC Survey 2024, BCG Analysis

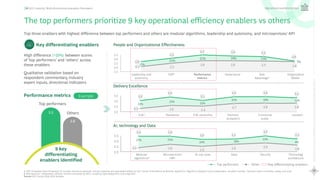

The top performers prioritize 9 key operational efficiency enablers vs others

High difference (>20%) between scores

of ‘top performers’ and ‘others’ across

these enablers

Qualitative validation based on

respondent commentary, industry

expert inputs, directional indicators

9 key

differentiating

enablers identified

Performance metrics Example

Top performers

Others

3.5

2.8

Top performers Other Key differentiating enablers

Key differentiating enablers People and Organizational Effectiveness

AI, technology and Data

1.5

2.0

2.5

3.0

3.5

Leadership and

autonomy

EVP1 Performance

metrics

Governance Skill

Advantage2

Organization

Model

25%

21%

21% 15%

7%

3.2

2.5

2.8 2.8

3.4

2.7

3.2

2.8

2.6

2.1

2.8

3.5

19%

Operational excellence pillars

Top three enablers with highest difference between top performers and others are modular algorithms, leadership and autonomy, and microservices/ API

Microservices5

/API

AI use cases Data Security Technology

architecture

2.0

2.5

3.0

3.5

27% 25%

20% 18%

13%

8%

Modular

algorithms4

3.4 3.4

3.1

3.4

3.1

2.8

2.9

2.6

2.6

2.5

3.0

2.4

Functional

scope

Location

2.0

2.5

3.0

3.5

CoE3 Resilience E2E ownership Partners

ecosystem

23%

22%

20% 18% 12%

2.7 2.8 2.8

2.4

2.6

3.4 3.2

2.3

23%

3.1

3.0

3.4 3.4

Delivery Excellence

19.

19

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

GCC maturity: Multi-dimensionalevaluation framework

Only 8% of GCCs are mature,

excelling across innovation,

market advantage, and

enterprise efficiency—most

spike in just one or two levers

Maturity varies sharply by

industry and geography—

technology, media, and

telecom leads with balanced

performance across all levers,

while India, Mexico and U.S.

stand out as the key

geographies excelling across

the board

Top performers stand apart on

9 enablers, especially in modular

algorithms, leadership and

autonomy, and microservices/API

—with AI emerging as a future-

defining differentiator

Three key

takeaways from

the multi-

dimensional

GCC maturity

evaluation

framework

01 02 03

Source: GCC Survey 2024, BCG Analysis

21

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

People and

Organizational

Effectiveness

A1. Leadership and Autonomy

● ~70% of top performers host a

significant number of global roles in

hubs, vs ~10% for underperformers

● ~60% of top performers operate

under centralized or semi-

centralized decision models

A2. EVP1

● 50%+ of top performers have a fully activated,

robust EVP—6x higher than underperformers

● Technology, media, telecom leads with ~30%

of hubs activating EVP

● Banking and financial services lags–65% tailor

EVP, but only 5% activate it effectively

A3. Performance Metrics

● All top performers regularly track

outcome based KPIs vs ~10%

underperformers

● Top metrics being tracked are cost

reduction, digitization and automation,

and business revenue/ sales growth

Delivery

Excellence

B1. CoE2

● 90%+ top performers set up or

expanded CoEs in the last

18 months

● AI/ML dominates the CoE agenda

with ~25% more setups than any

other area

B2. Resilience

● 90%+ of top performers align strong BCP

planning and resilient ops—setting the bar

for continuity

● Steep drop from top to above-average

performers in “highly resilient operations”

—from 50%+ to ~10%

B3. E2E Ownership

● True E2E ownership is rare—only

8–11% of top and above average hubs

fully own product development

● Active involvement without full

ownership is common— ~70% of top

and above-average performers fall

into this middle ground

AI, technology

and data

C3. AI Use Cases

● 90%+ top performing GCCs

implement advanced AI use cases

vs ~50% of others

● Technology, media, telecom leads

the way in AI implementation

C2. Microservices4/API

● Microservices maturity sets top performers

apart—100% vs. ~60% overall adoption at

advanced levels

C1. Modular Algorithms3

● Modular algorithm adoption is

nearly 1.5x higher among top

performers

What sets leaders apart: Top 3 enablers across people and organizational

effectiveness, delivery excellence, and AI, technology and data

Market Advantage, Innovation, Efficiency and Cost Advantage

Operational excellence pillars

A

B

C

1. EVP: Employee value proposition 2.CoE: Center of excellence 3. Modular algorithms: Algorithmsdesignedusing independent,reusable modules, making it easier to develop, debug, and scale 4. Microservices: Independentsoftware servicesconnectedby APIs—enabling rapiddeployment and integration

Note:Other key enablers include: (a) Peopleand org Effectiveness: Org model, governance, and skill advantage (b) Deliveryexcellence: Locationstrategy, functional scope, and partner ecosystem (c) GenAI, technology and data: security, technology architecture,and data management

Source: GCC Survey 2024, BCG Analysis

22.

22

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Leadership and autonomy: Top-performing GCCs have significant number of

global leaders in hubs enabling speed, ownership, and scale

GCC maturity correlates with on-ground

leadership presence

Number of global leadership roles based in the hubs

Large number of global roles based out of hubs (>30) Significant number of global roles based out of hubs (16 to 30)

Some global roles based out of hubs (5 to 15) Limited to no global roles at hubs (<5)

Top

performer

Above average

performer

Average

performer

Under

performer

As maturity decreases, so does

local leadership—limiting

responsiveness and ability to

drive continuous improvements.

Top-performing GCCs embed

leadership in hubs— ~70% have

16+ global roles based outside HQ

50% of underperformers host

fewer than 5 global roles,

reinforcing limited empowerment

People and Organizational Effectiveness A1

33%

50%

17%

7% 29% 46% 18%

16%

1%

50%

42%

8%

Source: GCC Survey 2024, BCG Analysis

29%

54%

23.

23

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

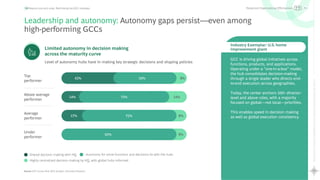

Leadership and autonomy: Autonomy gaps persist—even among

high-performing GCCs

Limited autonomy in decision making

across the maturity curve

Level of autonomy hubs have in making key strategic decisions and shaping policies

Shared decision making with HQ Autonomy for some functions and decisions lie with the hubs

Highly centralized decision making by HQ, with global hubs informed

A1

Industry Exemplar: U.S. home

improvement giant

GCC is driving global initiatives across

functions, products, and applications.

Operating under a “one-in-a-box” model,

the hub consolidates decision-making

through a single leader who directs end-

to-end execution across geographies.

Today, the center anchors 100+ director-

level and above roles, with a majority

focused on global—not local—priorities.

This enables speed in decision making

as well as global execution consistency.

Source: GCC Survey 2024, BCG Analysis, Secondary Research

Top

performer

Above average

performer

Average

performer

Under

performer

50%

42%

14%

72%

14%

17% 75%

92%

8%

8%

8%

People and Organizational Effectiveness

24.

24

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

EVP1: GCCs across the maturity curve recognize the importance of having

customized EVP1 in the local markets

Robust EVP1 is a defining trait of top

performers with 50% top performers

customizing and activating EVP1, over

6x higher than under performers

GCCs struggle to move from

customization of EVP1 to activation –

57% above average and 48% average

performers have customized EVP1 but

lack execution and activation

Under performers need to focus on

building EVP1 – 25% of under

performers have no EVP1, 6x more

than that of above average

performers

Top

performer

Above average

performer

Average

performer

Under

performer

How compelling is a hub's EVP1 to access, attract, hire and retain top talent

Robust EVP1 catering to local talent sensibilities with sufficient activation to target top quality talent

EVP1 customized to local talent sensibilities, but not enough measures taken to activate it in local markets

Global EVP1 rolled down to global hubs, with little customization for local talent sensibilities

No robust EVP1 for global hubs

25%

25%

50%

4%

28%

57%

11% 9%

48%

29%

14% 25%

50%

17%

8%

01

02

03

1. EVP: Employee value proposition

Source: GCC Survey 2024, BCG Analysis

A2

People and Organizational Effectiveness

25.

25

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Good relationship with colleagues

Good relationship with superior

Good work-life balance

Financial compensation

Financial stability of employer

Appreciation for work

Job security

Learning and skills training

Career development possibilities

Interesting job content

01

02

03

04

05

06

07

08

09

10

Good relationship with colleagues

Good relationship with superior

Opportunities to lead

Good work-life balance

Company values

Learning and skills training

Job security

Creative and innovative

environment

Career development possibilities

Collaborative working approach

-

-

-1

+2

-

-

Good relationship with colleagues

Learning and skills training

Good relationship with superior

Employer Reputation

Good work-life balance

Appreciation for work

Financial stability of employer

Appreciation for work

Career development possibilities

Company Values

-

+6

-1

-2

-

-2

-2

-

1. EVP: Employee Value Proposition

Source: BCG/The Network Proprietary Web Survey and Analysis

Global India North Africa

Good relationship with colleagues

Interesting job content

Good relationship with superior

Good work-life balance

Appreciation for your work

Financial compensation

(salary, bonuses)

Company values

Financial stability of your employer

Learning and skills training

Personal impact

-

+8

-1

-1

+1

-3

-1

Non-Exhaustive

More important in Region Importance +/- 2 vs. Global Less important in Region # Represents difference in Rank

Western Europe

EVP1: With EVP1 drivers differing by region, tailoring EVP1 locally is key to

attracting and retaining top talent

A2

People and Organizational Effectiveness

26.

26

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Banking and

Fin services

14%

16%

65%

5%

Technology,

media, telecom

8%

28%

36%

28%

EVP1: While many players are tailoring EVP1 to regional needs, activation

remains a major gap across most industries

How compelling is a hub's EVP1 to access, attract, hire and retain top talent

Robust EVP1 catering to local talent sensibilities with sufficient activation to target top quality talent

EVP1 customized to local talent sensibilities, but not enough measures taken to activate it in local markets

Global EVP1 rolled down to global hubs, with little customization for local talent sensibilities

No robust EVP1 for global hubs

Pharma 33%

17%

50%

Retail 36%

18%

46%

Industrial

goods

43%

37%

17% 3%

10%

43%

40%

7%

Consumer

goods

A2

One Team Culture

Strong internal culture rooted in unity

and collaboration with emphasis on

“one team” mindset

Focused Skill Development

Ongoing investment in employee

upskilling and certifications

Mobility

High cross-functional mobility across

roles and teams

Career Progression

Strong internal progression with

succession planning every 6 months

Locally Aligned Delivery Model

Cultural nuances are embedded in

delivery, driven by local leadership

Exceptional Retention

Lower-than-industry attrition

(single-digit), driven by strong culture

and above-industry pay

Industry Exemplar: Leading

global bank

1. EVP: Employee value proposition

Source: GCC Survey 2024, BCG Analysis

People and Organizational Effectiveness

27.

27

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Top

performer

50%

50%

Performance metrics: Top GCCs establish outcome-driven KPIs, ensuring

strategic alignment and faster execution

SLA and transaction KPI-only based monitoring have given way to

incorporating outcome based KPIs for performance measurement

Top outcome metrics that

GCCs use to measure success1

1. Percentages calculated on the base of 102 responses to the question received

Source: GCC Survey 2024, BCG Analysis

Regular tracking of value delivered by the global hubs using outcome-based KPIs linked to business outcome

Regular tracking of value delivered by the global hubs using a mix of transactional and outcome based KPIs

Regular tracking of value delivered by the global hubs using transactional KPIs

No regular tracking of value delivered by the global hubs, with only SLA-based performance monitoring

Track cost reduction

80%

Track process digitization

and automation

72%

Track business revenue/

sales growth

71%

Average

performer

4%

34%

46%

16%

Under

performer

8%

84%

8%

Above

average

performer

39% 32% 29%

A3

People and Organizational Effectiveness

28.

28

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

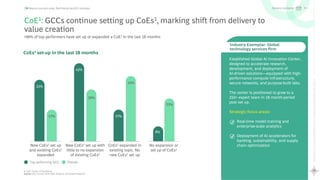

CoE1: GCCs continue setting up CoEs1, marking shift from delivery to

value creation

>90% of top performers have set up or expanded a CoE1 in the last 18 months

Top performing GCC Overall

No expansion or

set up of CoEs1

CoEs1 expanded in

existing topic. No

new CoEs1 set up

New CoEs1 set up with

little to no expansion

of existing CoEs1

New CoEs1 set up

and existing CoEs1

expanded

CoEs1 set-up in the last 18 months

23%

8%

17%

34%

42%

26%

17%

33%

Delivery Excellence B1

Established Global AI Innovation Center,

designed to accelerate research,

development, and deployment of

AI-driven solutions—equipped with high-

performance compute infrastructure,

secure networks, and purpose-built labs.

The center is positioned to grow to a

250+ expert team in 18 month-period

post set up.

Strategic focus areas:

Real-time model training and

enterprise-scale analytics

Deployment of AI accelerators for

banking, sustainability, and supply

chain optimization

Industry Exemplar: Global

technology services firm

1. CoE: Center of Excellence

Source: GCC Survey 2024, BCG Analysis, Secondary Research

29.

29

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

CoE1: AI/ML tops CoE1 focus, retail and technology drive innovation, Industrial

goods prioritizes sustainability

Business

support (e.g.,

HR, finance)

AI/

ML

Other

technology

(e.g., IOT,

AR/VR)

Climate and

sustainability R&D Innovation

Banking and

Fin services

Consumer

goods

Industrial

goods

Pharma

Retail

Technology,

media telecom

Low High

Number of CoEs1:

Delivery Excellence B1

4

Our integration into the new center of excellence

underscores our unwavering commitment to

harnessing top-tier talent and pioneering global

solutions to deliver exceptional client services.

This state-of-the-art collaboration hub is where

brilliant minds will continue to converge to

revolutionize the marketing landscape, driving

innovation and excellence at every turn

— CoE Head, Global marketing and

comms. company

In just a few years, the center has evolved into a

key growth engine for our digital strategies,

delivering AI-powered commercial and supply

chain solutions and pioneering advancements in

modern manufacturing. Looking ahead, we

remain focused on further investment,

leveraging outstanding talent and technological

expertise to shape the future and drive industry-

leading innovation in our core categories

— CXO, Leading consumer goods company

1. CoE: Center of Excellence

Source: GCC Survey 2024, BCG Analysis, Secondary Research

30.

30

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Resilience: GCCs across the maturity index are enabling operational

resilience through robust and continuous BCP activities

Robust BCP is a clear

differentiator—50% of top

performers operate with highly

resilient, regularly tested

continuity plans

46% of above average performers

have only limited BCP planning–

need to develop strong operational

resilience to leapfrog maturity

>80% of under performing GCCs

have limited or no BCP planning

making them vulnerable to

operational discontinuity

11% 43% 46%

10% 52% 36% 2%

17% 75% 8%

Highly resilient operations with robust business continuity planning and activation

Strong operational resilience enabled by robust BCP planning, resulting in minimal vulnerability to disruption

Limited BCP planning with basic enablement of operational resiliency measures

No BCP planning and limited resilience measures, resulting in high operational vulnerability

Top

performer

Above average

performer

Average

performer

Under

performer

Delivery Excellence B2

Source: GCC Survey 2024, BCG Analysis

42%

50% 8%

31.

31

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

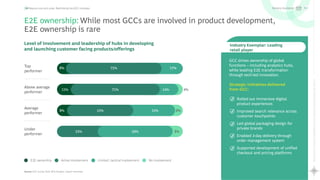

E2E ownership: While most GCCs are involved in product development,

E2E ownership is rare

Level of involvement and leadership of hubs in developing

and launching customer facing products/offerings

Source: GCC Survey 2024, BCG Analysis, Expert Interviews

E2E ownership Active involvement Limited, tactical involvement No involvement

Top

performer

Above average

performer

Average

performer

Under

performer

75% 17%

11% 14%

8% 33% 6%

33% 59% 8%

8%

4%

Delivery Excellence B3

GCC drives ownership of global

functions – including analytics hubs,

while leading E2E transformation

through tech-led innovation.

Strategic initiatives delivered

from GCC:

Rolled out immersive digital

product experiences

Improved search relevance across

customer touchpoints

Led global packaging design for

private brands

Enabled 2-day delivery through

order management system

Supported development of unified

checkout and pricing platforms

Industry Exemplar: Leading

retail player

71%

53%

32.

32

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

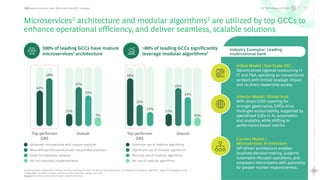

1. Microservices: Independent software services connected by APIs—enabling rapid deployment and integration 2. Modular algorithms: Algorithms designed using

independent, reusable modules, making it easier to develop, debug, and scale

Source: GCC Survey 2024, BCG Analysis, Expert Interviews

100% of leading GCCs have mature

microservices1 architecture

>80% of leading GCCs significantly

leverage modular algorithms2

Early microservices adoption

Well-defined microservices with established practices

Advanced microservices with mature practices

No microservices implementation

Overall Overall

42%

58%

11%

47%

35%

7%

11%

45%

34%

10%

Minimal use of modular algorithms

Significant use of modular algorithms

Extensive use of modular algorithms

No use of modular algorithms

17%

58%

25%

Decentralized regional outsourcing in

IT and F&A, operating as transactional

vendors with limited strategic impact

and no direct leadership access.

Initial Model | Sub-Scale SSC

With direct COO reporting for

stronger governance, GPOs drive

multi-geo accountability, supported by

specialized CoEs in AI, automation,

and analytics, while shifting to

performance-based metrics.

Interim Model | Global Hub

API-driven architecture enables

localized decision-making, supports

automation-focused operations, and

empowers micro-teams with autonomy

for greater market responsiveness.

Current Model |

Microservices Architecture

AI, Technology and Data

Industry Exemplar: Leading

multinational bank

C2

Microservices1 architecture and modular algorithms2 are utilized by top GCCs to

enhance operational efficiency, and deliver seamless, scalable solutions

C1

Top performer

GBS

Top performer

GBS

33.

33

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

Advanced AI use cases are leveraged by top GCCs to deliver faster,

smarter and more scalable solutions

Source: GCC Survey 2024, BCG Analysis

We have widely implemented advanced AI use cases throughout the organization (GenAI, AI-based

customer issue anticipation, natural language processing-enabled real-time solution suggestions,

single dashboard, and hybrid communication (voice and text)

90%+ of top-performers have

adopted advanced AI use cases

signaling that it is a key

differentiator for maturity.

Advanced AI adoption falls sharply

down the maturity curve— 90%+ top

performers agree, vs ~25% of

underperformers, highlighting

growing execution gap.

Top

performer

Above average

performer

Average

performer

Under

performer

8%

84%

8%

7%

25%

64%

4%

3%

44%

38%

15% 17%

58%

25%

Strongly agree Agree Disagree Strongly disagree

01

02

AI, Technology and Data C3

34.

34

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

Beyond cost andscale: Rethinking the GCC mandate

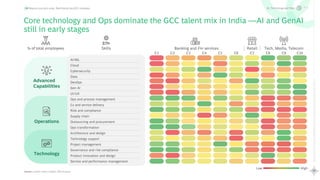

Core technology and Ops dominate the GCC talent mix in India —AI and GenAI

still in early stages

Source: LinkedIn talent insights, BCG Analysis

Low High

% of total employees Skills Banking and Fin services Retail Tech, Media, Telecom

C1 C2 C3 C4 C5 C6 C7 C8 C9 C10

AI/ML

Cloud

Cybersecurity

Data

DevOps

Gen AI

UI/UX

Ops and process management

Cx and service delivery

Risk and compliance

Supply chain

Outsourcing and procurement

Ops transformation

Architecture and design

Technology support

Project management

Governance and risk compliance

Product innovation and design

Service and performance management

Advanced

Capabilities

Operations

Technology

C3

AI, Technology and Data

36

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

Cost of stagnation in the AI era: Top GCCs double down on advanced AI, while

others risk falling behind

… witnessing high adoption of advanced AI use cases across

key strategic areas

Source: GCC Survey 2024, BCG Analysis

Strongly agree Agree Disagree Strongly disagree

Top performing

GCC

Others

Leading GCC have significant advanced

AI adoption vs 50% in others …

We have started implementing AI use cases and

pilots for GenAI use cases (GenAI, NLP etc.)

8%

46%

37%

14%

3%

84%

8%

Process automation and optimization

Enhancing traditional RPA, enabling intelligent

document processing and report generation

Predictive analytics and decision support

Refining demand forecasting, inventory management,

and optimizing processes for increased accuracy

Hyper-personalization

Tailoring market content, offers and product

recommendation, powering personalization at scale

Customer insights and CX impact metrics

Synthesizing real-time customer feedback,

accelerating CX improvements, leading to NPS, and

reduced handling time

Rapid prototyping and experimentation

Assist in developing software prototypes or

product designs to accelerate innovation cycles

New product development

Accelerating R&D across industries–component

optimization (automotive/ aerospace), software

development (technology)

Innovation

Market advantage

Enterprise efficiency

(incl. cost advantage)

37.

37

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

Automation use cases

The dominant traditional applications, focusing on

automating routine and repetitive tasks. These use

cases are popular but deliver only incremental value

on beyond existing RPA and ML technologies

Data driven use cases

Use cases focused on analyzing and providing

insights on large complex data sets. Frequently

used in financial planning and decision-making,

and well-established across GCCs

Knowledge synthesis use cases

Leveraging (Gen)AI to rapidly analyze and summarize

vast, unstructured data sets. This holds significant

potential to transform both operational tasks as well as

strategic decision making based on qualitative data

Content creation and knowledge management

Using the technology to generate rich,

multimodal content and managing complex

knowledge repositories

"Basic" AI use cases

● Document analysis through

OCR and AI models

● Invoice generation and

processing

● Data cleansing

● Data analysis and actionable

insight generation

"Advanced" AI use cases

● GenAI-based auto completion,

debugging for coding

● AI-based customer

issue anticipation

● Natural language processing

enabled real-time solution

suggestions

● Hybrid communication

(voice and text)

● Auto shortlisting resumes

AI adoption is a spectrum, with a divide between traditional and

emerging applications

Source: Global Capability Centers’ (Gen)AI agenda, April 2025 – BCG, Secondary Research

4

With our next-gen P2P automation platform

powered by low-code technology, we are

delivering new levels in automation rates, cycle

times, and execution quality—setting new

standards for the customer experience. We've

seen a 20% increase in automation for third-

party invoices and a 25% reduction in

turnaround time

— GCC function head, multinational

diversified group

Our vision for the next decade is to strengthen

the GCC not only as a delivery hub, but as a

strategic driver of growth and innovation.

Through continued investment in advanced AI,

cloud, data science, and talent, we aim to deliver

measurable value that supports both top-line

growth and operational efficiency

— MD, Global technology company

38.

38

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

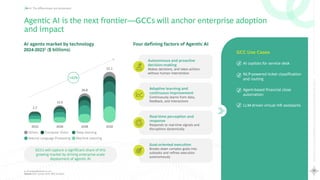

Agentic AI is the next frontier—GCCs will anchor enterprise adoption

and impact

GCCs will capture a significant share of this

growing market by driving enterprise-scale

deployment of agentic AI

2024 2026 2028 2030

5.7

12.0

26.8

52.1

AI agents market by technology

2024-20231 ($ billions)

Others Computer Vision Deep learning

Natural Language Processing Machine Learning

+45%

AI copilots for service desk

NLP-powered ticket classification

and routing

Agent-based financial close

automation

LLM-driven virtual HR assistants

GCC Use Cases

Autonomous and proactive

decision-making

Makes decisions, and takes actions

without human intervention

Adaptive learning and

continuous improvement

Continuously learns from data,

feedback, and interactions

Goal-oriented execution

Breaks down complex goals into

subtasks and refines execution

autonomously

Real-time perception and

response

Responds to real-time signals and

disruptions dynamically

1. GrandviewResearch.com

Source: GCC Survey 2024, BCG Analysis

Four defining factors of Agentic AI

39.

39

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

1.The other countries in the survey include UK, Brazil, Indonesia, France, Germany, Spain, Thailand, China, Puerto Rico, Vietnam etc.

Note: Total responses for each country – India (77), Malaysia (15), Mexico (18), Philippines (12), Poland (11), Singapore (26), U.S. (52), Others (195)

Source: GCC Survey 2024, BCG Analysis

We have widely implemented advanced AI use cases throughout the organization (GenAI, AI-based

customer issue anticipation, natural language processing-enabled real-time solution suggestions,

single dashboard, hybrid communication (voice and text)

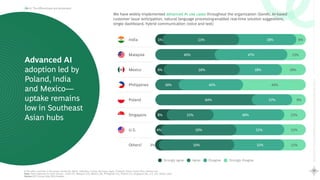

Advanced AI

adoption led by

Poland, India

and Mexico—

uptake remains

low in Southeast

Asian hubs

Strongly agree Agree Disagree Strongly disagree

Others1

13%

47%

40%

Malaysia

6% 16%

28%

50%

Mexico

16% 42%

42%

Philippines

9%

27%

64%

Poland

8% 15%

46%

31%

Singapore

India 5% 6%

38%

51%

4% 15%

31%

50%

U.S.

15%

32%

50%

3%

40.

40

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

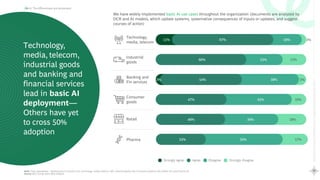

Note: Total respondents – Banking and Fin services (37), technology, media, telecom (36), Industrial goods (30), Consumer products (30), Retail (11) and Pharma (6)

Source: GCC Survey 2024, BCG Analysis

Technology,

media, telecom,

industrial goods

and banking and

financial services

lead in basic AI

deployment—

Others have yet

to cross 50%

adoption

Industrial

goods

17%

23%

60%

Banking and

Fin services

5%

38%

54%

We have widely implemented basic AI use cases throughout the organization (documents are analyzed by

OCR and AI models, which update systems, systematize consequences of inputs or updates, and suggest

courses of action)

Consumer

goods

10%

43%

47%

Technology,

media, telecom

3%

19%

67%

11%

Retail 18%

46% 36%

Pharma 17%

50%

33%

Strongly agree Agree Disagree Strongly disagree

3%

41.

41

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

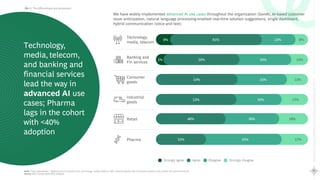

AI: The differentiatorand accelerator

We have widely implemented advanced AI use cases throughout the organization (GenAI, AI-based customer

issue anticipation, natural language processing-enabled real-time solution suggestions, single dashboard,

hybrid communication (voice and text)

8%

22%

61%

9%

Technology,

media, telecom

17%

30%

53%

Industrial

goods

13%

33%

54%

Consumer

goods

11%

34%

50%

5%

Banking and

Fin services

18%

46% 36%

Retail

17%

50%

33%

Pharma

Technology,

media, telecom,

and banking and

financial services

lead the way in

advanced AI use

cases; Pharma

lags in the cohort

with <40%

adoption

Strongly agree Agree Disagree Strongly disagree

Note: Total respondents – Banking and Fin services (37), technology, media, telecom (36), Industrial goods (30), Consumer products (30), Retail (11) and Pharma (6)

Source: GCC Survey 2024, BCG Analysis

42.

42

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

AI: The differentiatorand accelerator

Technology and data

Encompasses cloud architecture, GenAI

platforms, development lifecycle, data

ownership, and security policies

GCCs are starting strong on GenAI—but scaling and maturity

still lag behind

Source: Global Capability Centers’ (Gen)AI agenda white paper

5 key dimensions of the (Gen)AI Maturity Framework

Key insights from (Gen)AI Maturity

Framework Analysis

70%+ of GCCs have initiated GenAI efforts,

but most are still in pilot stages with

underdeveloped use case pipelines

~5% of identified GenAI use cases have

scaled; conservative investments (<$5Mn)

dominate the landscape

GCCs show low overall GenAI maturity (average

46/100), significantly trailing behind leading

BPO and technology peers (average 62/100)

Banking and financial services, and technology

are leading the change, showcasing higher

maturity and stronger returns.

40%+ of organizations have achieved

5–10% baseline savings; highest ROI seen

in firms investing >$15Mn

Bold transformation can drive 30% productivity

gains and shift 30–40% of the workforce from

repetitive to higher-value activities

Value

Realization

Gen AI

Adoption

Maturity

Operating model

Covers organization models,

GenAI leadership, and

governance structures

People

Focuses on workforce planning,

training, talent strategy, skill penetration,

and change management

Partner ecosystem

Involves external partner readiness,

integration, reassessment, innovation,

and IP/security frameworks

Strategy and

Governance

Includes

overarching

strategy,

leadership

buy-in, roadmap,

prioritization,

success metrics,

and ethical AI

compliance

44

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

The acceleration playbook:Closing the maturity gap

Call to action: Steps to becoming a top performing GCC

To evolve into a high-performing, future-ready GCC, organizations must take a structured, forward-looking approach. This journey involves three critical steps:

Clearly articulate the North Star, aligned with the

enterprise’s 3–5 year ambition and positioning the

GCC not just as a delivery engine, but as a

strategic enabler of enterprise growth.

Organizations must define the GCC’s evolving role

across three core value levers to drive both near-

term impact and long-term scale:

● Innovation

● Market advantage, and

● Enterprise efficiency (including cost advantage)

Once the vision is established, translate the vision

into action by selecting a set of enabling capabilities

across the three core pillars–based on what top

performers are doing well:

● People and organizational effectiveness–

leadership and autonomy, EVP, performance

metrics

● Delivery excellence–CoE, resilience, end to end

ownership

● AI, technology and data–modular algorithms,

microservices/ API, AI

Prioritize initiatives that balance foundational needs

with strategic ambition—enabling focused investment

and faster progress toward the GCC’s North Star

Benchmark current performance against

industry-leading GCCs using a structured,

multi-dimensional framework.

● Assess maturity across the prioritized

enablers

● Identify capability gaps and opportunity

hotspots

● Define a roadmap to close the maturity gap

by sequencing initiatives based on impact

and readiness

Conduct a maturity diagnostic to

chart the path forward

Identify and prioritize

strategic levers and enablers

Define the GCC’s long-term

vision and strategic role

45.

45

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

The acceleration playbook:Closing the maturity gap

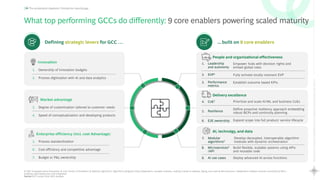

What top performing GCCs do differently: 9 core enablers powering scaled maturity

Defining strategic levers for GCC … ... built on 9 core enablers

Develop decoupled, interoperable algorithm

modules with dynamic orchestration

Build flexible, scalable systems using APIs

and reusable code

Deploy advanced AI across functions

People and organizational effectiveness

1. Leadership

and autonomy

2. EVP1

3. Performance

metrics

Empower hubs with decision rights and

embed global roles

Fully activate locally resonant EVP

Establish outcome based KPIs

AI, technolgy, and data

7. Modular

algorithms3

8. Microservices4

/API

9. AI use cases

1. EVP: Employee Value Proposition 2. CoE: Center of Excellence 3. Modular algorithms: Algorithms designed using independent, reusable modules, making it easier to develop, debug, and scale 4. Microservices: Independent software services connected by APIs—

enabling rapid deployment and integration

Source: GCC survey 2024, BCG Analysis

Enterprise efficiency (incl. cost Advantage)

5. Process standardization

6. Cost efficiency and competitive advantage

7. Budget or P&L ownership

Market advantage

3. Degree of customization tailored to customer needs

4. Speed of conceptualization and developing products

Innovation

1. Ownership of innovation budgets

2. Process digitization with AI and data analytics

Delivery excellence

4. CoE2

5. Resilience

6. E2E ownership

Prioritize and scale AI/ML and business CoEs

Define proactive resiliency approach embedding

robust BCPs and continuity planning

Expand scope into full product/ service lifecycle

46.

46

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

The acceleration playbook:Closing the maturity gap

Enhancing people and organizational effectiveness by empowering hubs,

reimagining and activating EVP1 and implementing outcome based KPIs

Empower hubs with decision

rights and embed global roles

Fully activate locally

resonant EVP1

Establish outcome

based KPIs

Define design rights

Define decision rights and document them in

governance charters and RASCI2 models to clarify

ownership between local and global teams

Accelerate global role integration in GCC

Establish global roles in GCCs by scaling functional

ownership, building talent density and equipping

leaders through structured exposure and targeted

development programs

Embed GCC in enterprise governance

Actively involve GCC leaders in steering committees

and strategic reviews

Track impact

Establish leadership mobility programs and

scorecards to track global engagement and impact

Identify current gaps

Derive insights from baselining activities and

identify core challenges impacting talent

acquisition and retention

Define future state vision

Identify talent needs driven by evolving service

goals and emerging role requirements

Adopt market best practices

Draw insights from best-in-class practices

implemented by leading GCC in the local market

Activate across touchpoints

Embed EVP across recruitment, onboarding, career

development, and recognition to drive consistent

experience and adoption

Redesign KPI

Move beyond SLAs to track business outcomes like

value delivered

Align KPIs by function

Customize 3-5 business linked metrics by domain to

reflect true contribution

Incentivize outcomes

Link variable pay and recognition programs to target

outcomes

Track and iterate

Review performance with leaders and adjust based

on insights

1. EVP: Employee Value Proposition 2. RASCI: Responsible, Accountable, Supportive, Consulted, Informed

Source: BCG Analysis

47.

47

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

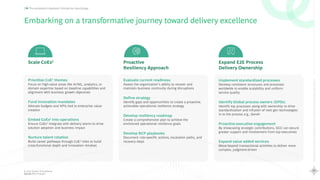

The acceleration playbook:Closing the maturity gap

Embarking on a transformative journey toward delivery excellence

Expand E2E Process

Delivery Ownership

Scale CoEs1

Prioritize CoE1 themes

Focus on high-value areas like AI/ML, analytics, or

domain expertise based on baseline capabilities and

alignment with business growth objectives

Fund innovation mandates

Allocate budgets and KPIs tied to enterprise value

creation

Embed CoEs1 into operations

Ensure CoEs1 integrate with delivery teams to drive

solution adoption and business impact

Nurture talent rotation

Build career pathways through CoE1 roles to build

cross-functional depth and innovation mindset

Proactive

Resiliency Approach

Evaluate current readiness

Assess the organization’s ability to recover and

maintain business continuity during disruptions

Define strategy

Identify gaps and opportunities to create a proactive,

actionable operational resilience strategy

Develop resiliency roadmap

Create a comprehensive plan to achieve the

envisioned operational resilience goals

Develop BCP playbooks

Document role-specific actions, escalation paths, and

recovery steps

Implement standardized processes

Develop consistent structures and processes

worldwide to enable scalability and uniform

service quality

Identify Global process owners (GPOs)

Identify top processes along with ownership to drive

standardization and infusion of next gen technologies

in to the process e.g., GenAI

Proactive executive engagement

By showcasing strategic contributions, GCC can secure

greater support and involvement from top executives

Expand value added services

Move beyond transactional activities to deliver more

complex, judgment-driven

1. CoE: Center of Excellence

Source: BCG Analysis

48.

48

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

The acceleration playbook:Closing the maturity gap

Transforming the technology landscape by developing scalable solutions,

streamlining technology operations and AI integration

Platform-driven

microservices2

Assess maturity

Review overall strategic direction and baseline

current operating model inc. scalability and

adaptability of current architecture

Develop global technology platform

with local agility

Define future ready platform enabling multi-market

adoption and local customization

Build unified data layer

Develop a centralized data layer to enhance

consistency, scalability, and decision-making

Implement modular

algorithms1

Implement standardized interface

Define consistent input/output structures to ensure

interoperability across modules

Enable reusability and scalability

Design each module to be independently deployable,

maintainable, and adaptable across use cases

Enable agile orchestration

Integrate modules through flexible workflows that

support rapid iteration and recomposition

Deploy AI

use cases

Identify high impact areas

Determine processes with the highest potential for

AI transformation

Develop and pilot solutions

Design AI solutions and implement pilot projects to

test feasibility, refine solution, and measure impact

Scale and Integrate

Expand successful pilots and embed them into

workflows across value chain

1. Modular algorithms: Algorithms designed using independent, reusable modules, making it easier to develop, debug, and scale 2. Microservices: Independent software services connected by APIs—enabling rapid deployment and integration

Source: BCG Analysis

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

50

Glossary

Advanced AI UseCases High-impact AI implementations including GenAI, NLP, real-time decision support, intelligent assistants, and advanced analytics models

AI Use Cases Business applications of AI (traditional or GenAI) to automate, predict, or generate outcomes

Basic AI Use Cases AI applications focused on routine automation (e.g., OCR-based document processing, basic data extraction, rule-based triggers)

CoE Center of Excellence–Specialized hubs for building deep capabilities in areas like AI, analytics, and innovation

Digital Maturity Readiness of a site to support AI, automation, and digital-enabled operations

E2E Ownership End-to-End accountability for product/process lifecycle—from design to delivery

EVP Employee Value Proposition–A hub’s promise to attract and retain talent through differentiated employee experience

GCC Global Capability Center or Global Business Services

GenAI Generative AI–AI that creates content, insights, or code (e.g., NLP, summarization, assistants)

Hub and Spoke Delivery model with central hubs driving scale, supported by regional spokes for resilience and localization

Microservices Independent software services connected by APIs—enabling rapid deployment and integration

Modular Architecture Flexible system design using interchangeable components for agility and fast scaling

P&L Profit and Loss - A financial statement that summarizes the revenues, costs, and expenses incurred during a specific period

Resilience/BCP Business Continuity Planning–Ensuring uninterrupted operations via contingency planning and failover

VP/SVP Vice President/Senior Vice President

Term Definition

51.

Rewriting

the

Global

Capability

Center

playbook

Scaling

Maturity

with

AI

51

Rajiv Gupta isa Managing Director and Senior Partner, in the New Delhi office

of BCG and leads the TMT practice area.

Sreyssha George is a Managing Director and Partner, in the Bengaluru office

of BCG and leads the GBS topic.

Sayan Majumdar is a Principal in BCG’s New Delhi office and is a member

of BCG’s Platinion team.

Romil Kulkarni is a Project Leader in BCG’s Bengaluru office and is a member

of BCG’s TMT practice.

Geetika Kaur is a Consultant in BCG’s New Delhi office and is a member of

BCG’s Platinion team.

We would like to acknowledge the support provided by Anuj Mandal

(Project Leader), Anannya Singhal (Consultant), Riddhi Sharma (Senior

Associate), Megha Jain (Senior Associate), Pranjali Rastogi (Senior Associate)

and Prerna Srivastav (Senior Associate) in preparing this report.

About the Authors

Acknowledgements

This study was undertaken by

Boston Consulting Group (BCG).

We thank all the participants of

the GCC survey and 1-on-1

discussions for their valuable

contributions towards the

enrichment of the report.

A special thanks to Nidhi Yadav

and Nopur for managing the

marketing process and to

Saroj Singh, Ratna Soni,

Soumya Garg, Pavithran NS, and

Seshachalam Marella for their

contribution towards design and

production of this report.

![[DSC DACH 23] Scaling & Industrialization of AI - Lukas Kölbl](https://cdn.slidesharecdn.com/ss_thumbnails/lukaskoelblready-230424075135-42c35132-thumbnail.jpg?width=640&height=640&fit=bounds)